How Many of These Mobile App Best Practices Is Your Bank Following?

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

How do the features of your institution’s mobile app stack up to major banks’ offerings?

As more daily banking gets done digitally, the app increasingly becomes the face of the institution. In the most recent edition of its biannual Mobile Banker study of 17 major banks’ apps, Keynova Group looked at two key feature categories: account opening via mobile devices and debit card controls and alerts.

Key insight: Debit card features are beginning to match those that major banks provide to credit card users. This grows more important as an increasing portion of consumers favor debit cards.

“People are using debit cards as a way of budgeting or restraining their spending,” says Susan Foulds, managing director. And customers increasingly notice when digital services for debit cards lag those for credit cards.

Competitive insight: Debit cards are also achieving greater visibility as more fintech players and buy now, pay later providers offer debit cards as an integral part of their own products.

Need to Know:

- Continuing a trend, U.S. Bank ranked first in the overall study and for mobile web service, while Bank of America and U.S. Bank tied for mobile app service.

- Debit card alerts are helpful not only to account holders, but also to parents and caregivers who have access to this information. More institutions are making delegated digital access available.

- Immediate enrollment in digital banking via apps has become table stakes. Consumers have no patience for waiting periods.

The study found that more institutions’ apps are catching up to their mobile website experiences. (“Mobile web” is essentially a bank’s website services, adapting through responsive design to device screens and functionality, and accessed through a mobile browser rather than an installed app.)

Keynova’s study evaluates the apps of 17 major and regional institutions, including Bank of America, BMO, Capital One, Chase, Citibank, Citizens Bank, Fifth Third Bank, Huntington Bank, KeyBank, M&T Bank, PNC, Regions Bank, TD Bank, Truist, USAA, U.S. Bank and Wells Fargo.

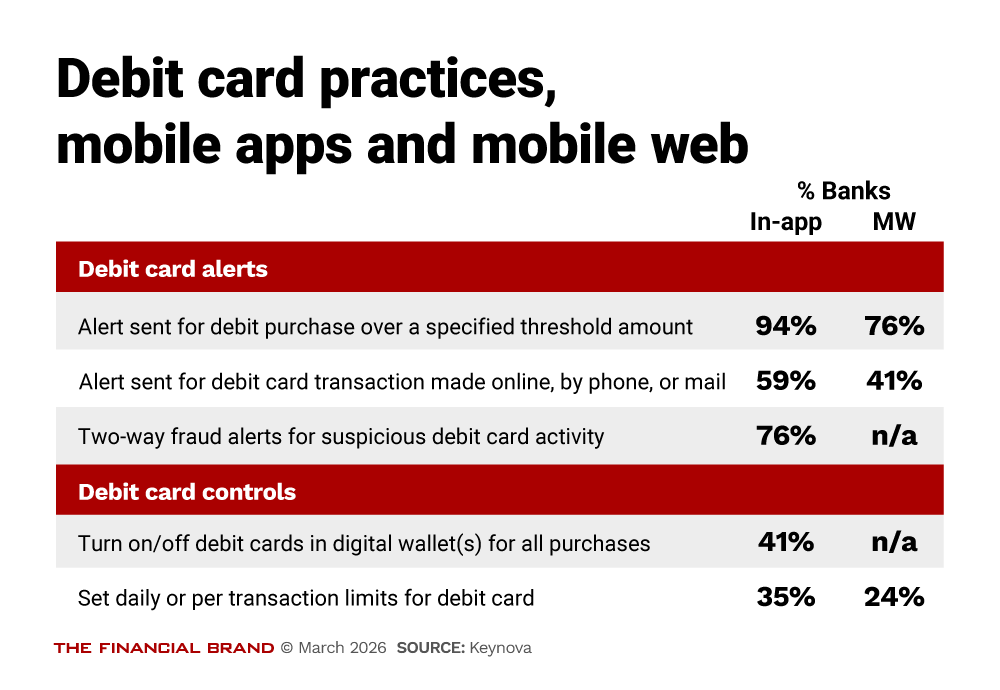

Mobile Banking Apps’ Debit Card Features Ramp Up

Among the banks studied, app functions relating to debit cards have become table stakes, while others are less frequently offered.

For example, as shown in the table below, some alerts, such as for debit purchases over a pre-set amount and for suspicious transactions, are now common. More than half of the banks enable alerts for debit transactions made online, by phone or by mail.

Yet some controls, such as restrictions at certain locations or for certain types of transactions, still set some providers apart.

Key insight: Only one out of four institutions offers the ability to lock debit cards for specific types of purchases, and even fewer institutions enable this in mobile web. That’s a blind spot when many consumers are trying to restrain their spending in the face of inflation.

A look ahead: Some alerts in time may be superseded by increased engagement by virtual assistants that some of the institutions provide on top of their apps. Foulds notes that Bank of America’s Erica and U.S. Bank’s Smart Assistant are ahead of others in these capabilities, but she feels that banks’ virtual assistants in general could still be doing more. (Keynova performs its research by maintaining active accounts with all providers.)

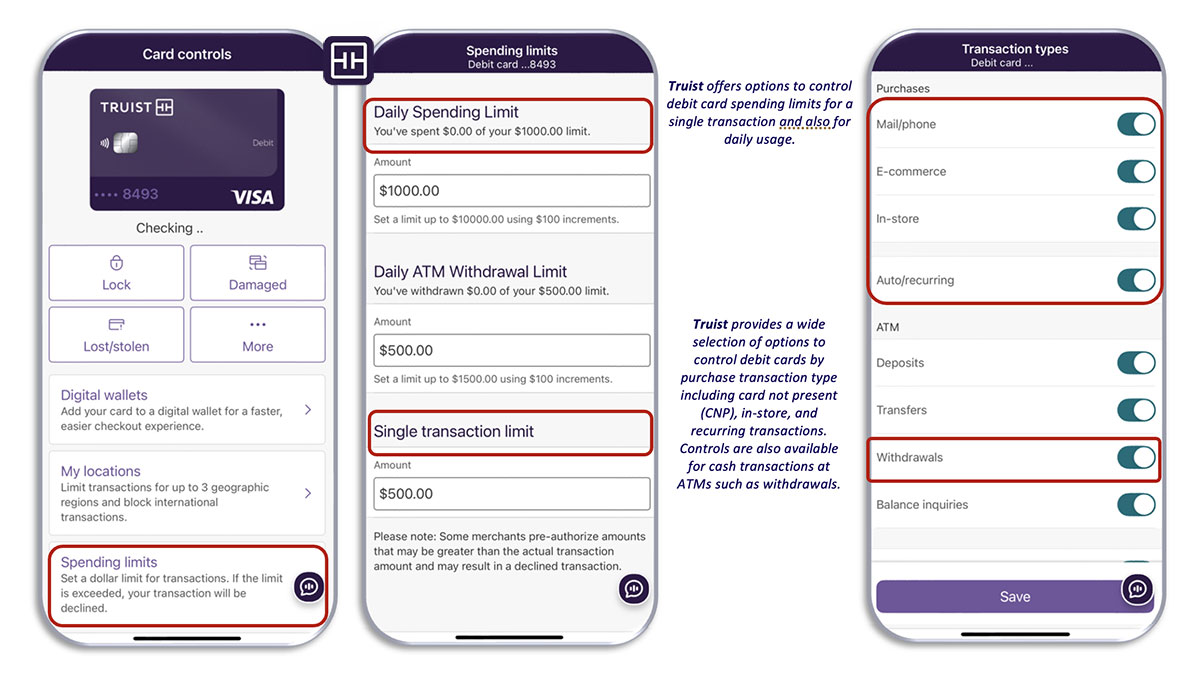

Case study. Keynova cites Truist’s alerts interface as a cut above.

Courtesy Keynova Group

Persistent weak spots: The study indicates that availability of external emails and text alerts for debit card transactions still lags those that credit card holders get in their apps.

Foulds adds that many providers provide separate apps for their credit cards, requiring customers who have bank accounts with the same institution to jump between apps.

“That seems pretty antiquated,” she says. Foulds thinks these multi-relationship customers ought to be able to deal with their provider all in one place, without multiple log-ins.

Read more: More Banking Apps Offer Predictive Insights, But Many Alerts Arrive Too Late

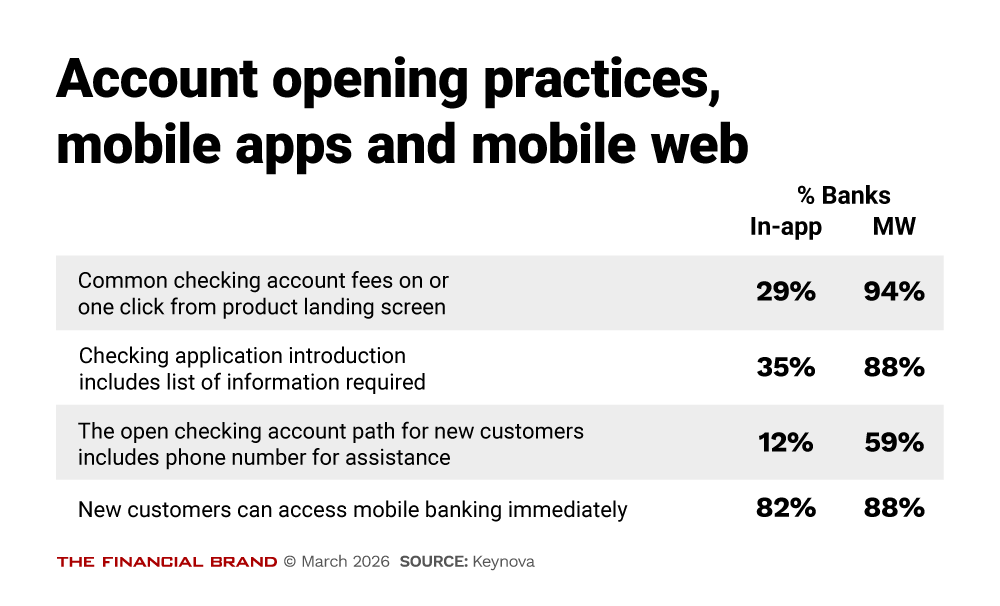

Opening New Accounts in Mobile Apps Becomes More Seamless

It’s basic, but often an oversight, according to Foulds: Not telling customers looking to open accounts via a bank’s mobile app what they’ll need to get things started. The study found that now six out of ten institutions give consumers these two essential pieces of information:

- A complete list of information and items needed to apply mobilely.

- A full description of account funding options, such as ACH transfers or debit cards drawn on other banks.

Key point: Foulds points out that taking these elementary steps can reduce abandonment and streamline enrollment.

A related weakness: the absence of something as simple as a phone number for assistance. Many institutions fail to provide one, which frustrates Foulds.

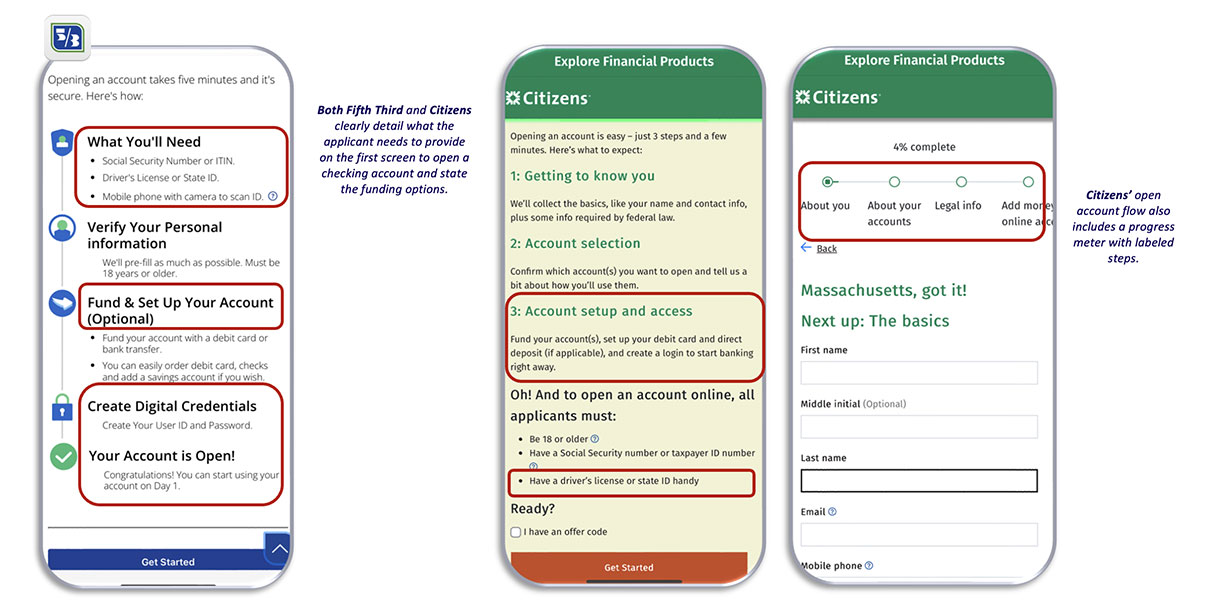

Courtesy Keynova Group

“You’re getting a new customer, a new account — what if they have a question?” she says. Providing a phone number is a simple way to staunch leakage of potential new business — and a dumb way to lose a lead that came to you.

Read more: Offering a Best-In-Class Mobile Banking App Is Easier Than You Think

How Smaller Players Can Adapt Their Mobile Apps

The study found that regional players are improving their apps.

Foulds acknowledges that smaller banks and credit unions don’t have the development bench that the larger institutions do, and are more likely to be relying on vendors to provide their apps.

However, she says, “the good news is that with APIs and, potentially, some open banking, these smaller players can integrate other applications beyond what’s offered through their service provider.”

This can enable more adaptation to specific customer bases and local market needs. A bank serving an agricultural community can consider features of interest to that type of economy, for example.

“So community banks, and even good-sized regional banks, can customize their app offerings,” says Foulds, “and that’s something they really need to do.”

Read next: How Digital Shopping Tools Turn Credit Card Apps into Transaction Amplifiers