Why and How Banks Need to Build Share in Buy Now, Pay Later

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

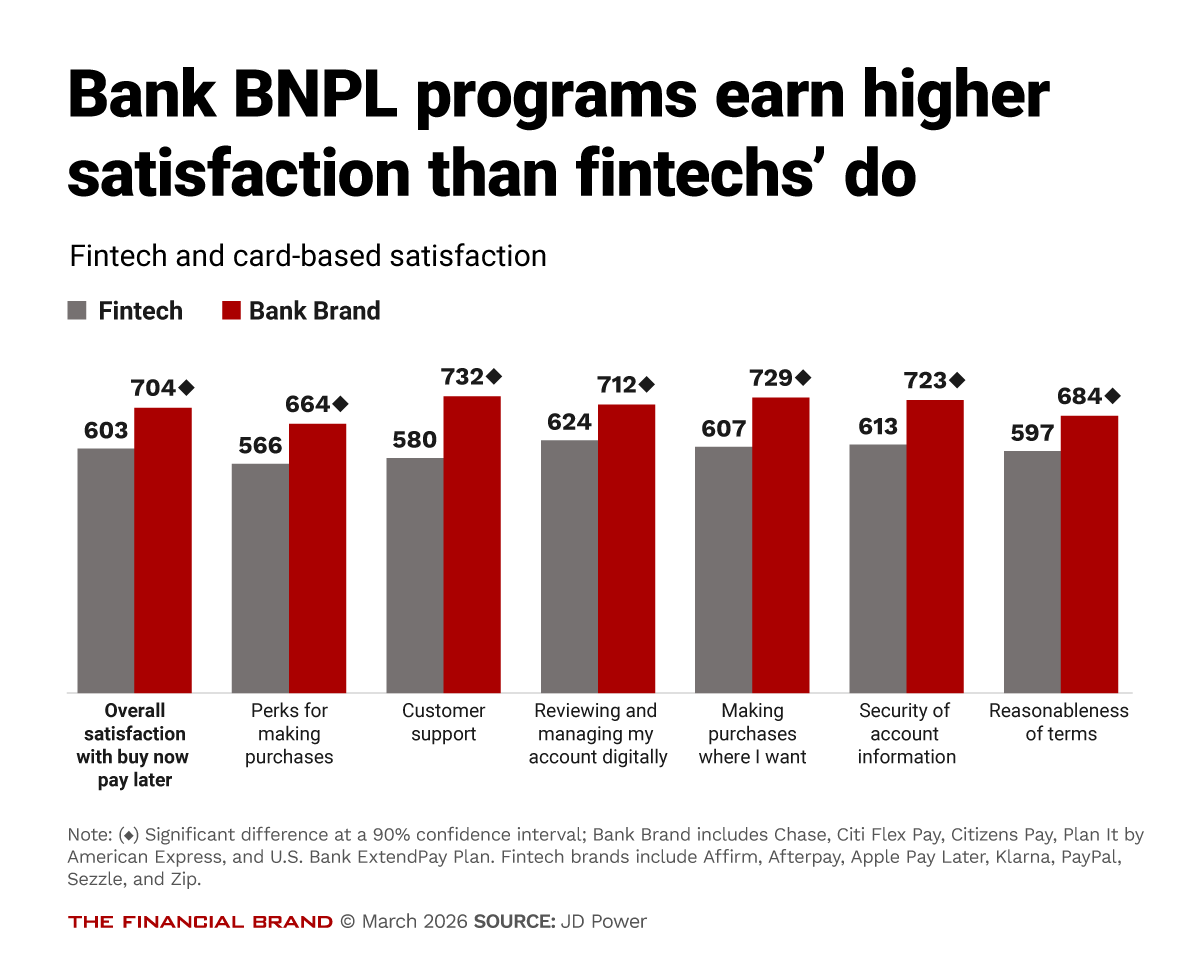

An emerging dichotomy has developed in buy now, pay later payments in the U.S., according to new research by JD Power.

• On one hand, BNPL users’ satisfaction with banks’ programs has pulled significantly ahead of those from fintechs.

Banks received an overall satisfaction rating of 704 points out of 1,000, while fintechs received an overall rating of 603. The bank BNPL providers’ rating was up 59 points from the firm’s previous study, while the fintech providers’ rating was down 17 points. In addition, multiple fintech players saw their scores drop year over year.

• On the other hand, fintechs not only maintained their overwhelming lead in usage over bank brands’ programs, but widened it slightly. Among respondents to the firm’s survey, 97% use fintech BNPL, up one percentage point from the earlier study. Banks’ usage, at 3% of the nearly 4,000 consumer sample, was down a percentage point.

A growing number of credit unions and smaller banks are venturing into BNPL as a payment option tied to their debit card programs.

How do banks and other traditional players slice into the fintechs’ dominant market share, while building upon their superior customer satisfaction ratings and their longstanding customer bases?

Need to Know:

- BNPL usage is growing rapidly. The JD Power 2026 U.S. Buy Now Pay Later Satisfaction Study found that 37% of consumers made a BNPL purchase within 90 days of being surveyed, a five percentage point increase over the 2025 edition.”This is the fastest-growing payment method that we track,” says Sean Gelles, senior director of banking and payments at JD Power. He adds that 50% of younger consumers use BNPL to some degree.

- Chase pulled ahead of Plan It by American Express in the satisfaction rankings for the top spot, with Citi Flex Pay in third. From there, in descending order, were Sezzle, Zip, Afterpay, PayPal, Affirm and Klarna.

- Major surprise: Nearly half — 48% — of bank card customers who choose to switch to a BNPL plan have already made the decision by the time of checkout, versus 52% that wait until reviewing or paying their credit card bill. Among consumers under 40, making the BNPL decision at checkout is even stronger — 59% lean that way.

- “Pay in four” plans dominate the mix among both bank and fintech BNPL users.

“If you don’t have a buy now, pay later product, you need to launch one,” says Gelles. “You need to meet your customers where they are.”

Banks and Fintechs Are Approaching BNPL from Opposite Directions

Most bank BNPL lending is post-purchase, that is, a charge initially made on a credit or debit card that is switched into a payment plan via the provider’s app or website.

On the other hand, fintechs dominate pre-purchase BNPL, where the consumer opts into a plan at checkout. (The study did not include bank-operated white-label installment plans offered through merchants and professionals like doctors.)

However, some fintechs have been putting more muscle behind their own debit cards that allow post-purchase plans.

The debit card push: Klarna, for example, has been marketing this alternative aggressively in digital commercials recently. One spot shows a toy motorcycle as an example of what you’d buy on debit. Out the window beyond the toy is a matching full-size motorcycle, as an example of something better to finance with a plan.

“Fintechs see the debit card path as a way of attriting customers away from incumbent financial institutions. That’s how they’re going to get deposits at the end of the day,” says Gelles. “Fintechs see this as a strategic wedge.”

During recent investor presentations, Affirm has pointed to major growth in volume attributed to debit card use — and is attempting to tie its BNPL plans into banks’ debit card programs via bank vendors like FIS and Fiserv.

Read more: As BNPL Giants Push Debit Cards, Credit Unions Counter with Pay Later Offerings

BNPL is Fintechs’ Competitive Lever, and Entry Point

Bryce Deeney is CEO and co-founder of Equipifi, which helps banks and credit unions set up and operate debit-card-based BNPL programs.

Key insight: “Companies like Klarna and Affirm couldn’t have started with post-purchase programs because they had no users,” says Deeney. “How do you gain users? You do it through checkout. But now that they’ve amassed tens of millions of users, they’re trying to figure out how to deepen wallet share and engagement. That’s by shipping their users debit cards, aiming to become a bank, opening up deposit relationships.”

Key point: BNPL giant Affirm applied for a Nevada industrial bank charter and FDIC coverage in late January, to form Affirm Bank, which would enable the fintech to raise insured deposits on its own.

- PayPal — separately subject of acquisition speculation — offers BNPL services and has applied for an industrial bank charter in Utah.

- Block, owner of Square and the BNPL operation Afterpay, already owns an industrial bank. More charter applications from BNPL providers may be coming.

The precedent: Deeney points to SoFi Technologies, which started as a fintech and acquired a bank charter, as an example of how mission expansion happens. SoFi began with student loans when it was founded in 2011. Now, it provides a broad range of banking services. He adds that the fintechs’ urgency to broaden and diversify have multiplied since the days of very cheap credit.

Read more: How Consumers Under 40 Are Driving Radical Transformations in Payments

Is BNPL for Bank Card Customers Only a Defensive Play?

Gelles says many incumbent banks “understand that they need to build a moat around their customers” as BNPL fintechs branch out and make a grab for their business. “It’s more of a blocking and tackling maneuver,” so far, he says.

The superior customer service rankings for the incumbents indicate that now that the banks have products in the market “they’ve definitely been working on making the customer experience the best they can possibly make it,” according to Gelles.

Chase is the pacesetter. He says Chase pulled in front of American Express, which has offered Plan It since 2017, by upping its game on nearly every front. Chase’s satisfaction score rose 31 points to 706. Key elements include better clarity regarding perks and which charges can and can’t be rolled into a plan. Chase offers BNPL post-purchase options for both its credit cards and its debit cards.

Key insight:In a forthcoming report, Fullstory, a behavioral data platform, indicates that 79% of consumers in its own BNPL survey say they abandon BNPL checkouts at times because of lack of clarity in terms.

Two leading reasons:

- “I couldn’t tell what the total cost would be until too late in the process.”

- “The payment schedule wasn’t shown clearly before I had to commit.”

Read more: Your Customers Will Blame You When Their Shopping Bots Go Rogue

Going on Offense: Take a Page Out of the Fintechs’ Book

JD Power’s Gelles says the nearly 50%-50% split revealed by the study between pre- and post-checkout decisions to use BNPL represents a significant opportunity for banks.

“Why should they have to wait? Why not make it easy for them?” says Gelles.

Case study: In November, U.S. Bank unveiled a new product designed to enable consumers to make such a choice during the checkout process, both online and at point of sale. The product is called U.S. Bank Split World Mastercard.

The card uses Mastercard pay rails. Charges to the card of over $100 are automatically split into a three-month payment plan. Longer terms are also available, for a fee. The bank indicated in its announcement that it expects strong uptake from Gen Z. (The bank has offered a more typical card with the option to shift to BNPL plans since 2021. It’s called U.S. Bank ExtendPay Plan.)

Equipifi’s Deeney notes however that the Split card requires credit-card-style application and approval, something that many BNPL users may not want to undergo.

Bottom line: Deeney believes that for incumbent financial institutions, BNPL represents not so much as opportunity to add more customers as a means of deepening the relationships that the bank or credit union already has. He believes this plays to consumers’ wishes to consolidate often fragmented financial relationships into fewer hands.

Read more: How to Build Customer Relationships When Checking Accounts No Longer Confer Primacy

Understand Who Your BNPL Customer Will Be, and Why

On the surface, it may seem like BNPL services compete head-to-head with traditional bank and credit union credit card programs. Some incumbents might tend not to promote, or even adopt, BNPL out of fear that usage would cannibalize use of lucrative credit cards.

Wrong: Equipifi’s Deeney doesn’t agree with this thinking. He maintains that, “for a consumer who uses a credit card, they like to use a credit card. For a consumer who does not use a credit card, they either use debit or debit plus buy now, pay later.”

Theoretically, he says, card profitability might be considered superior versus BNPL profitability. But Deeney doesn’t think the distinction is that neat.

“You could spend marketing money until you’re blue in the face trying to sell credit cards to people who don’t use them,” says Deeney. “But they simply won’t use them if it’s not their preferred payment method.”

Key insight: Deeney also says cards can’t be compared to BNPL without considering the burden of items like credit card losses, which can be formidable. He notes that BNPL transactions are underwritten as the customer goes, while the basic underwriting of a consumer for a card may be years old and not reflect their current credit nor even their current employment status.

Debit-based BNPL can also bolster the institution’s funding, which drives profitable lending, and it also generates interchange income on the initial swipe.

Generation BNPL. A final argument in favor of adopting pre-purchase BNPL, and BNPL in general, is to appeal to younger generations, according to Deeney. He believes young consumers will consolidate their banking business with whichever provider is offering their preferred choice of payment, which is often BNPL.

Take American Express Plan It, he says: “Your typical Klarna or Affirm user does not have an American Express Platinum Card in their wallet. In fact, the vast majority don’t have credit cards at all.”