How Banks Can Block Financial Scams Targeting Older Customers

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Fraud against American senior citizens continues to explode. With proliferating headlines about “pig butchering” and other scams, major banks are stepping up anti-fraud efforts. What steps should your bank or credit union take to address this burgeoning customer risk and protect your customers?

Need to Know:

- In 2024 people 60 or older filed 147,127 elder fraud complaints, with losses totaling around $4.9 billion, according to a 2025 report by the FBI.

- Both complaints and losses are skyrocketing: Complaints rose 46% over 2023 and losses increased by 43%.

- Fraud runs the gamut from phishing, spoofing and fake tech support calls to romance scams preying on the lonely.

- New research from Keynova pinpoints key tools that banks can help family and other trusted parties prevent and detect fraud patterns.

- Innovative programs include Huntington Bank’s Caregiver Banking, and similar offerings from Wells Fargo and KeyBank.

How are banks responding? A study of 18 major banks by Keynova Group found a range of strategies to address the threat of fraud and other account risk.

“Banks are evolving their offerings to address increasingly sophisticated digital fraud targeting their aging consumers and to support caregivers who they may rely on for managing their finances,” says Susan Foulds, managing director at Keynova. The efforts include both educational content for seniors and family members as well as digital tools.

What are the baseline tools? Nearly all of the 18 institutions studied by Keynova provide key account alerts that can be sent to multiple recipients. About half of the group also provides educational content, guides or security kits to help protect seniors against financial cons. JPMorgan Chase, for example, has published a guide covering many concerns for seniors, ranging beyond fraud.

What are the next steps? Foulds says some banks are now offering controlled or limited access to account information for trusted family members, friends or professional advisors. Among them are Huntington, KeyBank and Wells Fargo. Foulds points out that this capability has been available to small businesses for some time and is now being applied to consumer accounts by the three companies.

It’s not just fraud. Seniors experiencing the onset of dementia also make purchasing errors or other financial mistakes.

“We found in our research that the aging adult might sit on QVC a little too long and buy things on a recurring basis that they didn’t realize they bought, or even need,” says Mark Rhoades, deposit product and pricing director at Huntington Bank.

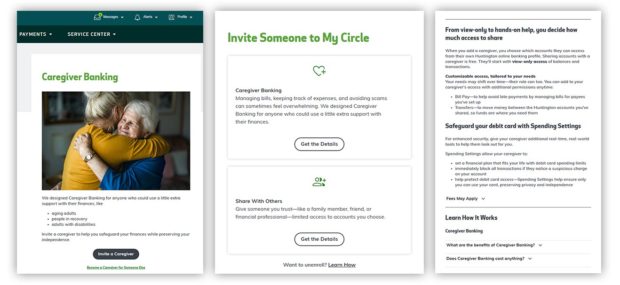

Case Study: How Huntington’s Caregiver Banking Helps Seniors

Rhoades says his bank’s research found that the needs of two generations are involved here.

- The seniors themselves, whose income and assets lie at risk.

- The “sandwich generation” caught between managing the affairs of senior parents and the needs of their own children.

The first level of its Caregiver Banking service is read-only access to the senior’s account. Rhoades says the trusted family member or other party does not have to be on the account in any way and doesn’t have to be a Huntington customer in their own right.

“You can go in and help your mother or father with their cashflow, and you’ll be alerted so you can understand the transactions that occur,” says Rhoades. This level of access doesn’t permit the trusted party to move any funds nor to set up any new bill payments.

The second Caregiver level involves the trusted party more directly in the senior’s affairs. Using a debit card with spending controls, the trusted party can set daily spending limits, which can preclude some large transfers that frauds often involve. Controls can also be placed on ATM withdrawals, as well as spending by categories or by merchant.

“So you could specifically block QVC, for example, or casinos in general,” says Rhoades.

Huntington Bank’s Caregiver Banking program offers multiple ways for trusted parties like children to help the elderly with their banking.

Coming up: These are just the first tools that Huntington intends to include in Caregiver. Rhoades says the bank is looking at similar controls for credit cards.

In addition, he says, the bank is exploring how to implement a secondary authentication or approval process for other types of consumer payments, such as automated clearing house transfers, wires and Zelle payments.

Rhoades explains that some fraud arises from caregiver employees or from family members themselves. Simply setting up joint accounts may amount to turning over the keys to a fraudster close to home.

Read more: Fraudsters on the Line: The Rise of Call Spoofing

How to Start Your Own Senior Banking Anti-Fraud Effort

Fraudsters don’t discriminate between customers of large institutions or small ones, so setting up a program is critical for banks and credit unions of all sizes.

Use tech you likely already own. Foulds says most banks have the digital capabilities to implement many of the alerts and spending controls that would help with senior fraud because they already have similar capabilities for business customers. Some institutions would have to beef up their debit card spending controls.

Keynova found that some institutions’ email and text alerts for debit cards aren’t as sophisticated as those available to credit card holders. These should be improved.

A key feature: alerts to “card not present” transactions.

Keep everyone in the loop. Foulds recommends building in communications so trusted parties, notably seniors’ children, understand clearly that some degree of participation in their parents’ finances has been set up. In this way they won’t be surprised by alerts and other messages — or think that the messages themselves are some kind of spam.

Create a regular customer content stream on the problem. An essential first step for all institutions is getting the word out. “It’s now table stakes to have articles about scams targeting older populations,” says Foulds.

Read more: How Banks Can Combat Customer Fraud Flying Under the Radar