The Innovation Gap Forcing Banks into Fintech M&A

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Globally, the average fintech is growing at 21% annually, more than triple the rate of 6% for incumbents. And while the fintech sector is only getting started — with overall market penetration of about 3% — they are scaling, profitable competitors that are expanding into markets that banks once assumed were theirs alone.

Why This Moment Matters: Nigel Morris — Capital One co-founder and now managing partner at QED Investors — believes retail banks are now at a critical strategic inflection point: As these fintechs advance, regulators are opening the gates — and most incumbents are standing still.

Morris says: “When I have conversations with incumbent leaders, their focus is often on protecting and defending, not on innovating and growing.”

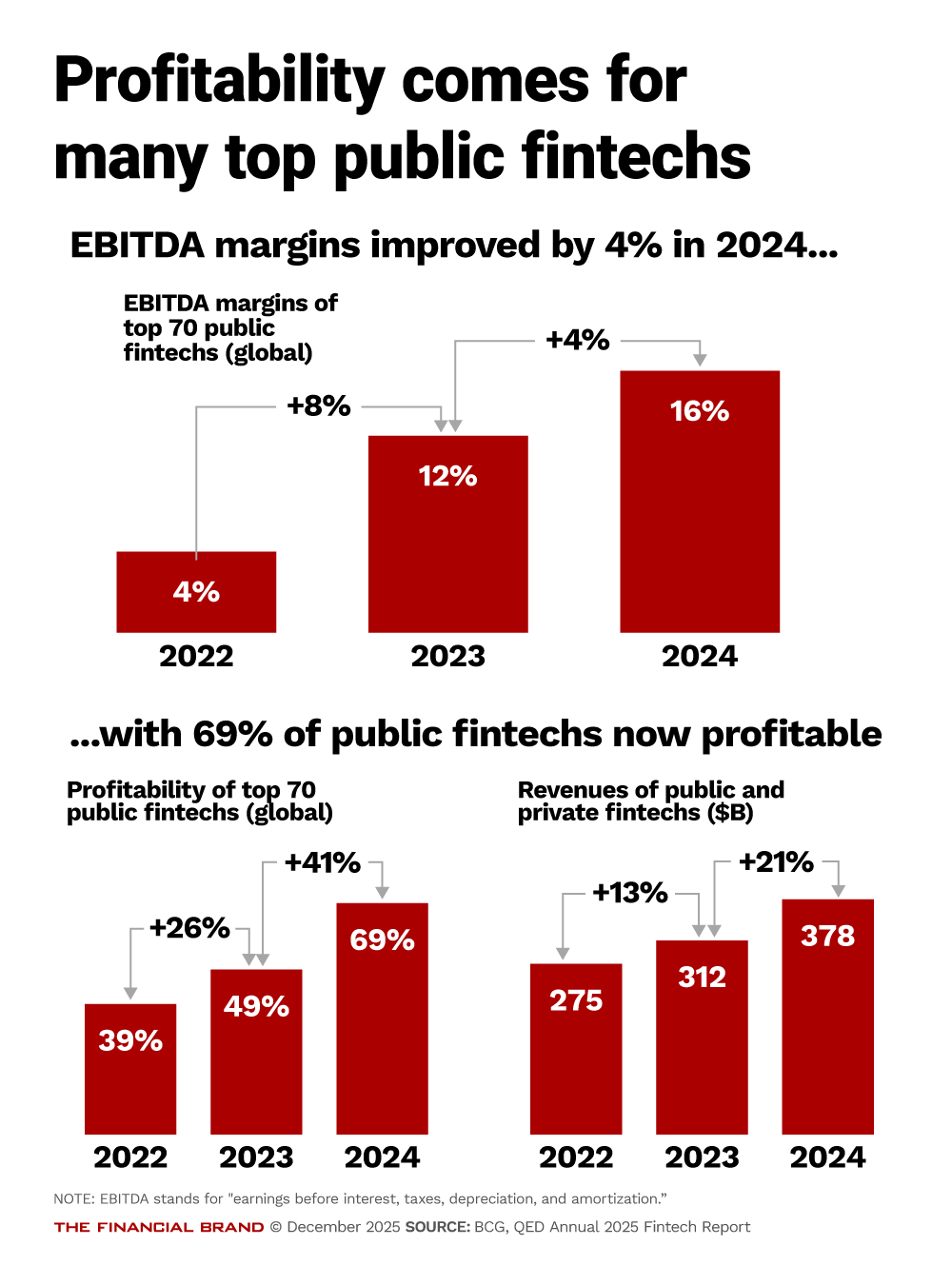

This is a critical mistake because the more seasoned and sizable fintechs have changed. “Two or three years ago, these fintechs were trying to get to escape velocity,” says Morris. “Now they’re public, profitable, incredibly well-run, and outgrowing incumbents.” Examples include Klarna, Robinhood, Credit Karma, Nubank and Chime.

What’s at Stake. Within a decade, Morris sees fintech penetration reaching 10% — and in some of the fastest-growing slices of the market.

“The gap between incumbent growth and fintech growth will accelerate because fintechs are getting bigger and stronger,” says Morris. “These new organisms are winning the Darwinian battle.”

The New M&A Imperative

So what should incumbents do? Morris’s message is simple and stark:

Banks should stop trying to out-innovate fintechs. Instead, they should quickly find, vet, partner with, and acquire fintechs.

His advice:

• Reframe your M&A strategy from “Should we acquire another bank or credit union?” to “How can we make fintech acquisitions become our primary innovation engine?”

• Build a structured fintech scouting and partnership pipeline to avoid overpaying for scaled fintechs later.

• Acquire smaller fintechs early to build integration muscle before pursuing larger strategic plays.

• Shift from defensive execution to growth-oriented innovation or risk permanent erosion of market share.

Trust the Source

Morris knows both sides of the fintech-banking divide. In the 1990s, he co-founded (with current leader Richard Fairbank) Capital One Bank, which he calls an “early fintech.” Morris later founded QED Investors, a Virginia-based venture capital firm, in 2007. QED Investors holds significant positions in about 150 firms, among them Nubank, Current, Albert, Remitly, Avant and Prosper.

Read more: How the Marriage of Open Banking and Payments Will Change Everything

Missed Opportunities: Why Most Banks Are Not Effective Innovators

Surveying the last decade or so, Morris says, “There are so many businesses now that have been created by fintechs that banks could have owned.” Example: BNPL. Banks understood merchant service and financing at the point of sale via credit cards, says Morris. “But no banks have any significant ownership in that space,” says Morris. Other misses include digital brokerage, cross-border payments and earned wage access.

The reality? “Banks shouldn’t necessarily try to out-innovate fintechs, because, you know what? That’s their job,” Morris says. “Fintechs are, by their very nature, disruptive. They’re trying to tip all the toys out of the box and create really interesting and different ways of solving problems with digital and other technologies.”

Bank Innovation is Hamstrung by Culture

The key cause, according to Morris? “Culturally, it’s very, very hard for banks to innovate. The people who tend to end up running banks tend to be people who don’t make mistakes. They are good executors, good leaders, good spokesmen and women.”

Innovators Exist but They’re the Exceptions

The banking industry isn’t devoid of innovators, Morris acknowledges, but they comprise a tiny minority of the business. Among them are Capital One, JPMorgan Chase, Fifth Third, KeyBank, American Express, Citigroup, Truist, U.S. Bank, Santander and BBVA. These institutions aren’t necessarily inventing things in their own shops but using their innovation functions to find the best partners — or acquisitions — among fintechs to realize what they are trying to accomplish.

Role model: Morris singles out Fifth Third’s Tim Spence, chairman, CEO and president: “He’s made fintech acquisitions, been able to get them to work, and I think Fifth Third’s gathering momentum because of that.”

Read more: The Classic Checking Account Doesn’t Meet the Needs of Today’s Consumers. Here’s How to Fix It

Regulators Are Opening the Door – for Fintechs

All these shifts coincide with what will be at least three more years of what Morris labels “laissez-faire” financial regulation out of Washington, including increasing openness to considering charter and deposit insurance applications from fintechs and other nontraditional companies.

Morris also says greater federal willingness to consider mergers and acquisitions across the spectrum of bank sizes suggests a bulking up among traditional contenders as the industry consolidates.

Read more: A Wave of New Charters is Coming. Meet Your New Competitors

How Banks Should Execute Fintech M&A

Go to school on the fintech space. Most bankers don’t understand the fintech world, according to Morris. Below the big names, there are thousands of firms that are “fighting for oxygen, fighting to reproduce, figuring out their business models,” he explains.

Selling to a strategic buyer, such as a bank, is one of several exit strategies for founders and investors. Banks bring to the table existing profits, branding, regulatory access and distribution channels. “Partner with it, invest in it, buy it, leverage it, and figure out strategically how you can get the best of both worlds,” says Morris.

Start small. Begin scouting targets before someone comes along to shop the fintech. “It requires a lot of effort and energy and a real commitment to watching the fintech ecosystem,” says Morris. “Go to school on how to assimilate them, and how to manage this different kind of organism,” says Morris.

Final Thought: Don’t Stand Still

Morris says too many banks confuse inertia with loyalty.

“Think about a world where Klarna and Nubank and Robinhood are coming after regional banks’ deposits with surgical targeting, maybe even agentic AI,” warns Morris. “If I as a consumer have a checking account and a savings account and they are commodities as insured accounts, I will move that money for 20 basis points.”