Why NYC is Still the Key Proving Ground for Branch Innovation

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- While post-Covid statistics showed shrinkage in branch counts in New York City and nearby markets, there are indications of a leveling off and institutions big and small have been exploring selected opportunities for new branch strategies.

- Manhattan continues to be a unique market, crammed with retail and commercial opportunities, especially as return to work policies repopulate it.

- The Long Island market — Nassau and Suffolk counties — while linked inextricably to the city, has opportunities as well. Large banks, midsized banks and community banks find attractive options.

In downtown Manhattan, along the island’s spine, sits Union Square, one of the city’s green spaces. From the west side of the park you can still see a building, complete with Greek columns, that long ago housed “Bank of the Metropolis,” shuttered for decades.

On the south edge are locations of three modern banks. One is a branch of Citibank, complete with a long rack of the blue Citibikes that the institution has sponsored for years. Another is one of the six Capital One Cafés based in Manhattan —but more an outreach effort to promote the mostly digital bank. Finally, half a block away, there’s a Bank of America branch, with a large sign urging passersby to come in to “Get Your Financial Game Plan.”

Something you’ll also see — in fact, they block some views of the bank locations — are street vendors: food wagons, peddlers of old books, and goods of dubious provenance. It’s a fact of life in Manhattan, so much so that when Gina Bleedorn, president and CEO of Adrenaline, was pitching a client about a city branch makeover, the firm included some street vendors in the artist’s conception of the exterior, to add realism.

But unusual visual accompaniment is not what makes Manhattan unique banking territory.

Its skyscrapers, especially as return to office mandates have taken hold, are increasingly full of people again, all of whom need banking services during the workday, tripling the demand for banking that would otherwise exist, according to one expert’s estimate. This has led to a measure used by some institutions: “daytime households per branch.”

Manhattan’s vertical nature — also including countless apartment buildings for natives — busts the math of typical branch planning.

Consider deposits, because branches today are about deposit gathering. Andrew Hovet, managing director at Curinos, points to a key branch metric, average retail deposits. The nationwide average is around $95 million per branch. In the greater New York City area, the figure is about $150 million.

In Manhattan, says Hovet, the average is approximately $280 million per branch — about three times the national number.

Of course, Manhattan commercial leases — virtually all branches there are leased, not owned — are typically astronomical, so payback takes a while, but retail banking is a long-term game.

Manhattan is also a showcase for design, from the high-end retail industry forward, notes Danielle Calcara, senior vice president, marketing, at NewGround International. “Developments like that are going to be looked at and then adopted throughout other industries,” she explains.

In banking, “you’re usually going to see it in New York first,” says Scott Florini, vice president, strategy, at NewGround. “A lot of the contemporary design — use of glass, use of digital technology in the financial retail space, and the considerable use of environmental graphics — is no longer unique, but it started there. Concepts first emerge in the New York marketplace.”

Bank of America opened a flagship branch in midtown Manhattan earlier this year and Chase has had its own blocks away, near Grand Central Terminal, for several years. Both feature various leading design elements, with an emphasis on consultation, rather than traditional teller-heavy service. Chase also launched one of its first two J.P. Morgan Financial Center private bank branches in Manhattan, at Columbus Circle, in late 2024. This growing network, with an upscale look and feel, is being built on the acquired First Republic branches.

Read more: Big Banks Are Heading South… and Loving It

New York Market By the Numbers

The New York City area market consists of the five counties or boroughs of the city itself and parts of other states, including New Jersey and Connecticut. Institutions in other states, such as N.J., have entered New York via Manhattan and from there, like a steppingstone, over the East River to Long Island. But veteran branch planners tend to think of the market in terms of the five boroughs and two counties on Long Island, Nassau and Suffolk.

The city is home to around 8 million people and there are about 3 million residents in Nassau and Suffolk — nearly twice that of the city’s northern suburbs — per a recent report by the New York Federal Reserve District Bank. The report also notes that median household income is higher at $121,000 on Long Island than in the city or the northern suburbs.

A word about the geography. Manhattan, as mentioned, is an island, with the Hudson River on one side and the East River on the other. The Bronx, across from Manhattan on the other side of the Harlem River to the north, is the only part of New York City that’s part of the U.S. mainland. Staten Island is, well, an island, off the southern tip of Manhattan.

That leaves two more boroughs, which are actually part of Long Island geographically. The island is shaped somewhat like a fish. Brooklyn is the jaw, Queens is the head. When New Yorkers say they are going “to the Island,” they mean Nassau, around the fish’s pectoral fins, and Suffolk, the body, which eventually separates into the North Fork and the South Fork (home of the Hamptons where the rich and famous live in the summer).

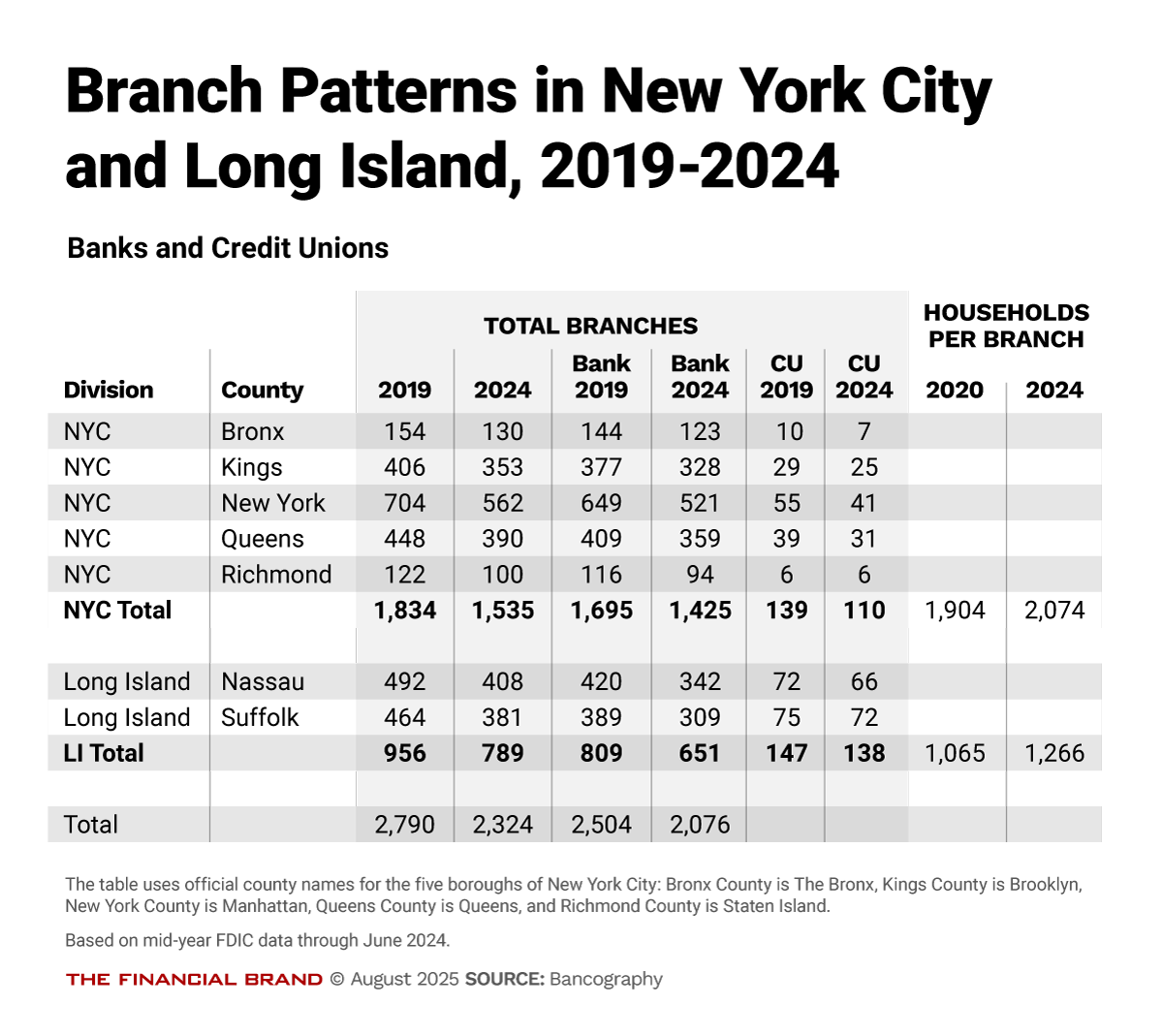

Bancography produced the tables that follow, illustrating the trends in the market from pre-COVID mid-2019 to mid-2024. (FDIC’s mid-2025 numbers will not be available until later in the year.)

The table illustrates the trend county by county in the city and on Long Island, including both banks and credit unions.

The total number of branches in the city fell by 16% — a bit higher, 20%, in Manhattan (officially New York County, as noted in the table). Credit unions closed branches at a higher rate (down 20.8%) than banks (down 15.9%).

On Long Island, total branches fell by 17.5%, with banks falling by 19.5% and credit unions by 6.1%.

The number of households per branch, computed at the level of the two geographic regions, has risen in both cases, as shown in the final column of the table. In this measure, the higher the number, the better, because it means fewer branches are serving more households — it is less competitively crowded, explains Steven Reider, founder and president of Bancography. The number grew higher for both geographies, but Long Island is more concentrated than the city. This further illustrates the advantage of branches in the urban environment.

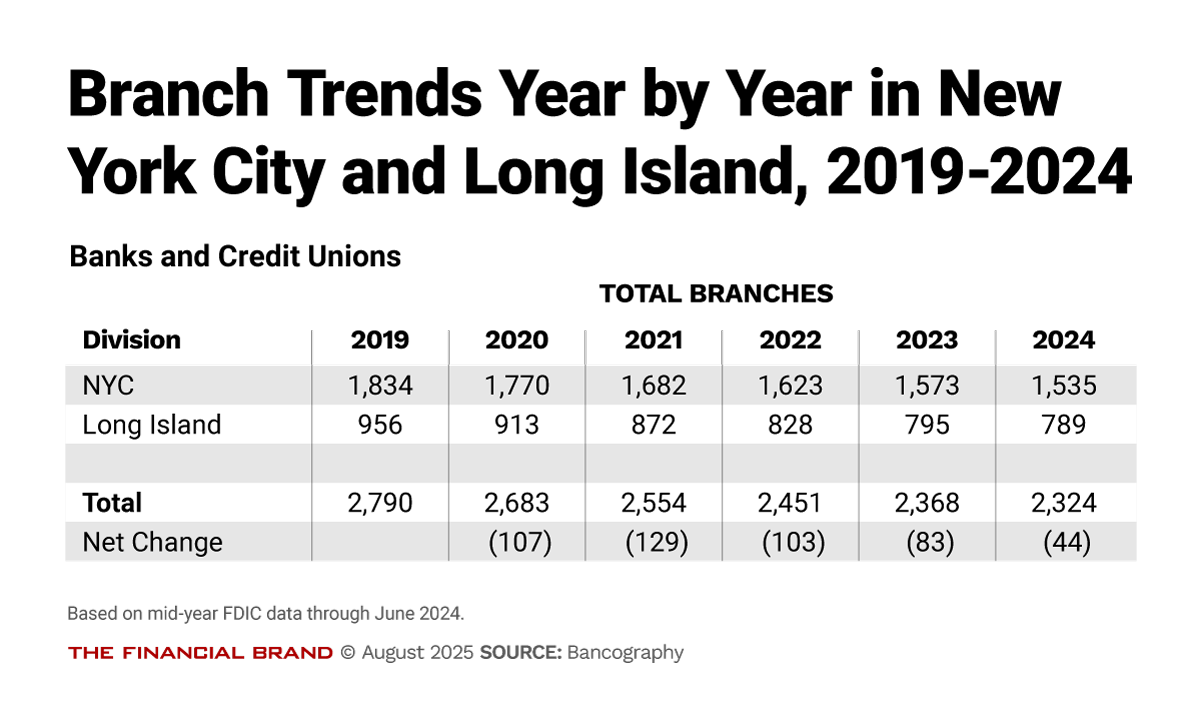

In the next table, Bancography tracked the trends in total bank and credit union branches for each year between mid-2019 and mid-2024. The rate of closure in the city went from a peak of down 4.9% between 2020 and 2021 to 2.4% between 2023 and 2024.

On Long Island, the rate of closure peaked between 2021 and 2022, down 5%, falling to down 0.75% between 2023 to 2024.

Reider notes two trends in these numbers and in the table.

First, in the entire industry, 2020 and 2021 marked the greatest years of branch contraction in the modern era, he says.

“Many banks used the COVID crisis as cover to close a lot of branches,” says Reider. Some of the shrinkage has been the result of mergers thinning the branch population, says Reider, as well as some institutions betting that with digital channel use increasing, consumers will tolerate “a little bit more spacing between their branch locations.”

Second, while net closures are still occurring, Reider sees significance in the latest trend.

“In 2020 and 2021, we shed more than 6,000 branches across the industry, in those two years combined,” says Reider. “Last year, it was only about 1,000.”

The pace of closures in these regions of N.Y., he adds, “is mirroring what we’re seeing in the U.S. It’s still negative, but by much smaller increments than in prior years. That tells me that we’re reaching an equilibrium branch level in the industry.”

Bancography research indicates that in mid-2019 to mid-2024 period the larger the parent institution the higher the percentage of branches trimmed in the city. Banks greater than $100 billion in assets cut 18% of branches, those between $10 billion and $100 billion cut 15%, $1 billion to $10 billion cut 8%, and smaller institutions cut 1%. The pattern was generally similar among Long Island branches, though the smallest institutions actually showed a very small gain over the period.

Among the biggest banks, nationally, there has been “judicious branch expansion,” says Reider. “This expansion is very focused towards specific markets that the institutions are seeking to win, versus just throwing a bunch of branches everywhere.” (Among institutions aggressively branching are Chase, Bank of America and PNC.)

Curinos’ Andrew Hovet points out that some of that growth is being funded through savings “harvested” in past years by trimming or consolidating branches elsewhere in institutions’ systems. “Over the last five years, they’ve taken a lot of cost out,” says Hovet.

An additional factor in new branches is that credit unions, especially as more have adopted community charters and expanded fields of membership, have been selectively looking to add offices. (Reider notes that sometimes they pick former bank branches.)

Both trends have been seen to a degree in the New York and Long Island markets.

Reider adds that nationwide the controlling factor for net changes in branching has been closures, because the number of openings has hovered between 1,000 and 1,110 a year. “The close-to-open ratio keeps getting a little bit smaller,” says Reider.

Whether slowing shrinkage will continue remains to be seen. The Trump administration is seen as being more open to bank mergers and acquisitions than the Biden administration, for example. M&A could lead to branch trims depending on who gets together. On the other hand, as we’ll discuss, other players are building.

The ante for staying in the branching game is going up, especially in city locations, according to Adrenaline’s Bleedorn. During COVID a good deal of upkeep and maintenance was put off. Given the costs of city real estate, keeping branches from looking tired has always been a challenge.

“But now it’s more than general upkeep,” says Bleedorn. “Now you need to be pushing the needle on experience. If you’re not, the bank next door is renovating and changing models to be a little more customer- centric.” A common move is slashing the size of the teller area and putting the space to other uses, or simply shrinking the floor plan. Bleedorn says the new Wells Fargo look explored in an earlier story on The Financial Brand that stresses consultation and a homey feel is the kind of thing laggards must contend with.

Read more: Omnichannel’s Unfinished Business: Reviving the Bank Branch to Reignite Loyalty

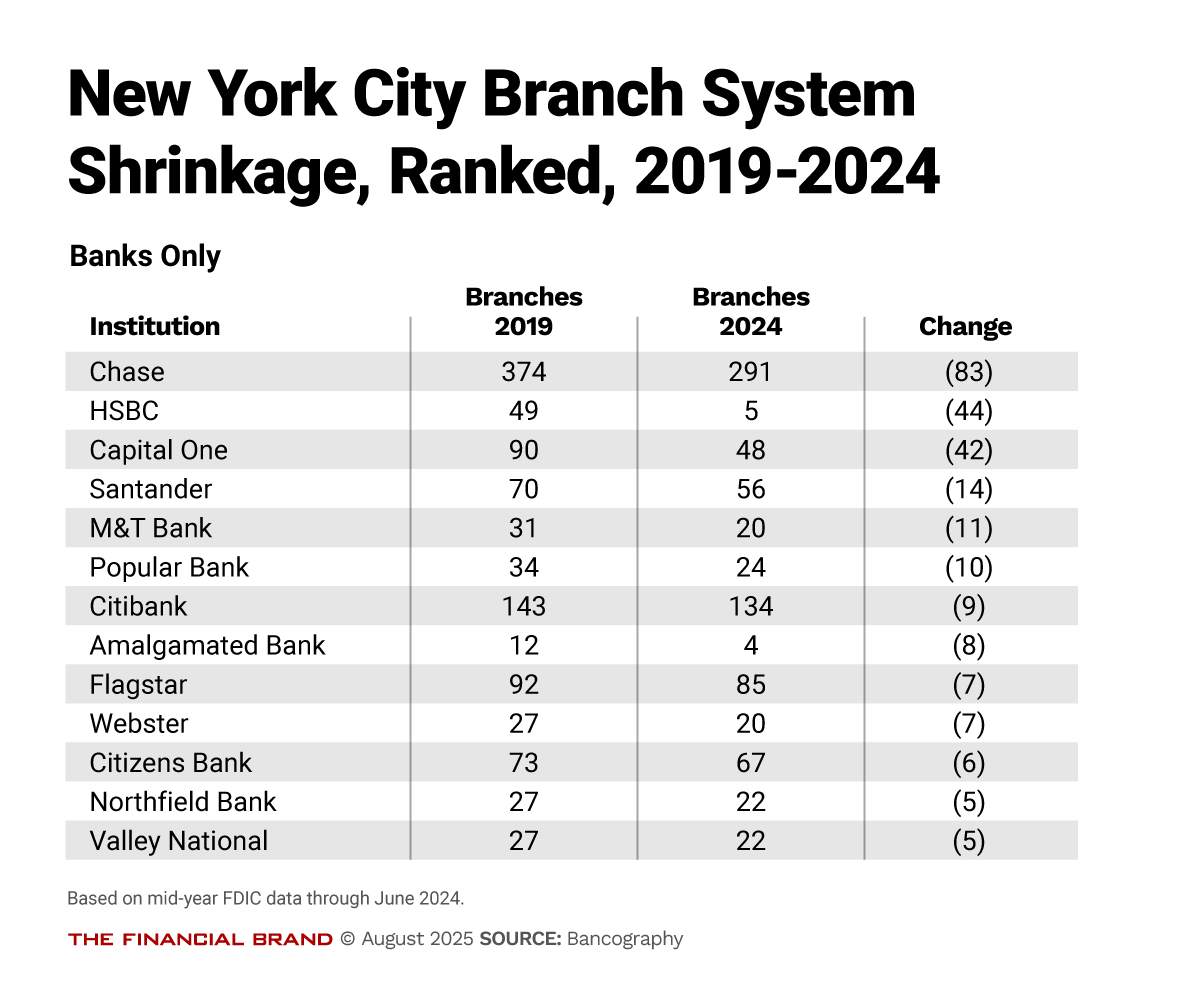

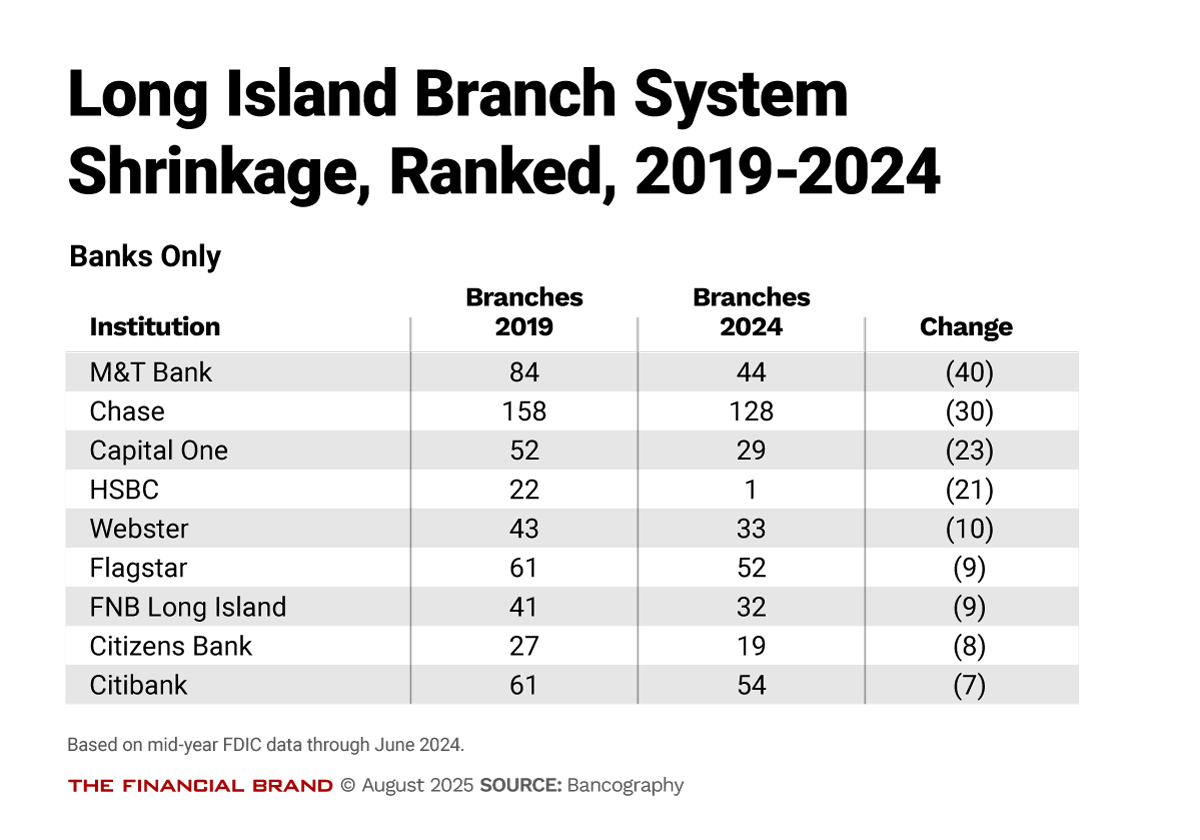

Who’s Been Closing Branches in NYC and Long Island

Chase is considered the city’s 900-pound branching gorilla, partly through longstanding pro-branch strategies and partly due to its merger history. The bank is a New York-headquartered institution, which actually puts it in the minority. Bancography research in mid-2024 figures indicates that 401 city bank branches and 192 Long Island bank branches were owned by in-state banks, while 1,024 city bank branches and 459 Long Island bank branches were owned by out-of-state institutions. (Nearly all credit unions operating in the two areas are New York headquartered.)

Jones Lang LaSalle, the real estate services company, manages several thousand Chase properties. Nickolas Hayden, executive managing director at the firm, says that Chase is constantly tuning its network.

“They’ll close branches, but they’ll also open them,” says Hayden. In the city, he says, the bank has put many of its locations through upgrades or facelifts, “with a robust schedule moving forward.”

“Chase is the incumbent, the market share leader,” says Curinos’ Hovet. The bank’s sheer ubiquity in Manhattan “gives them advantages because everybody knows who Chase is, so they’re probably in the consideration set for everybody.”

“Chase is always repositioning,” Hovet says. “They are always thinking, ‘Here’s an old facility. I can either refresh that facility or I can move down the street.’ So you do see some ‘new’ Chase branches, but they’re usually a two-for-one or a relocation. It’s hardly ever a net new in New York because they already have such massive market share.”

Hovet explains that there’s a critical mass institutions have to achieve, in terms of the number of locations that will provide the public with awareness that they are in a market and seeking business.

“If you don’t have anything at the top of the funnel, it doesn’t matter how efficient you are at the bottom of the funnel,” says Hovet. “Nothing’s going to flow through.”

Not every institution playing in the city is looking for mass business, he notes. Some are there for specialized business banking plays, for example.

The tables below show institutions that have cut branches in the 2019-2024 period in both the city and Long Island. (Some institutions that made smaller cuts have been omitted for space.)

Building Up Branches in Both Regions

On the other hand, Wells Fargo announced plans earlier this year to add at least 20 additional locations in New York City metro areas including Queens and Brooklyn and in Nassau and Suffolk. The target date for that thrust is the end of 2026.

This is a quest to build greater density in these markets. (This is on top of a branch opened in upper Manhattan, as well as in the Long Island City section of Queens and in Southampton in Suffolk County earlier this year, all earlier this year.) (Dive Deeper: “Wells Fargo Is Leaning Hard Into Branches Again – And With a Fresh Take”)

In an interview with The Financial Brand earlier this year, Brad Nolan, head of branch systems and transformation, said that “we’re casting a much wider net, beyond 2026. So the number will be well north of 20 once we’re said and done.”

Bank of America has been active on Long Island, opening branches recently in Suffolk County’s Hampton Bays, on the south shore, and Rocky Point, on the north shore.

NewGround’s Scott Florini says Suffolk County has seen significant population growth in many of its census tracts, which has been attractive to some institutions.

Read more:

Not Just for the Larger Players

Growth in the city and Long Island hasn’t been solely for big banks.

Take ConnectOne Bank, a commercially oriented bank headquartered in New Jersey. In recent years it branched into Manhattan and then leapt out to Melville, near the Nassau-Suffolk county line. A big move came this June when the now $13.9 billion-assets bank acquired First National Bank of Long Island, with branches in both Nassau and Suffolk. Between this deal, which added 40 branches to the bank, and other moves, the bank now has more branches in New York than New Jersey. It is now one of the top five banks on Long Island, with 60 branches.

Frank Sorrentino, chairman and CEO, expects that the branch network will go through some optimization, but he points to the sheer size of Long Island from tip to tail.

“It’s over a hundred miles long, from New York City out to East Hampton,” says Sorrentino. “So, there’s a lot of real estate to cover there. The need for more office locations is required in order to bank the population out there.”

Sorrentino has long had a branch-light philosophy, but is also a realist about the need for proximity to deliver customer service. Branches are being built in various markets and more are in planning, in all the bank’s areas. One already going up will be near Long Island MacArthur Airport, a key commercial hub for Suffolk County.

“Do I expect we’re going to have some major explosion in the number of branches? Probably not,” says Sorrentino. “Do I expect that we’re going to cut back the number dramatically? Probably not. But over time there will be optimization.”

He notes that First National had a deeper retail base than the acquirer, which will require somewhat more brick and mortar than ConnectOne would historically have used.

Looking back west, to Manhattan, would Sorrentino consider expanding beyond his single location there? He doesn’t see the urgency, but adds that “if we hired a couple of great bankers who were more conveniently placed in lower Manhattan, maybe.”

Smaller banks than ConnectOne are also interested in expanding in the city and Long Island. For example, Hanover Bank, a $2.3 billion-assets bank in Nassau’s Garden City, has branches in both the city and opened its tenth branch in Suffolk’s Port Jefferson in June. That makes the second branch for the bank in Suffolk.

A special niche has also encouraged several smaller banks to expand their networks in the city, Long Island or both. This is to serve the area’s growing Asian communities.

One such is $9 billion-assets Flushing Bank, located in Queens. About a third of the bank’s branches are currently in Asian markets and more locations are being planned to build this specialty. Among these are locations in Manhattan’s Chinatown and Queens’ Jackson Heights, home to Asian communities. The bank now has branches in Hicksville and New Hyde Park, in Nassau County, serving growing Asian populations there. (The bank opened a branch in Melville, in Suffolk, in late 2024.)

To guide this growth, the bank set up an Asian Advisory Board. It has also sponsored related seasonal celebrations of Lunar New Year and Diwali.

Read more: Inside Chase’s Aggressive Consumer Strategy: More Deposits, More Cards, More Branches, More Lending