Why AI Agents May Be the Tech to Finally Deliver on Personalization

According to Salesforce, the financial industry is entering the 'agentic AI era' in which artificial intelligence advances beyond backend operations and risk management to enhance customer engagement and service delivery.

By Jim Marous, Co-Publisher of The Financial Brand, CEO of the Digital Banking Report, and host of the Banking Transformed podcast

Simple Subscribe

Subscribe Now!

While the banking industry continues to discuss improving personalized recommendations and contextual engagement, customer satisfaction with personalization remains surprisingly low, according to the Connected Financial Services Report published by Salesforce. Only 21% of banking customers report being fully satisfied with their institution’s personalization efforts. This satisfaction gap represents both a challenge and an opportunity for financial institutions wanting to build engagement and expand relationships.

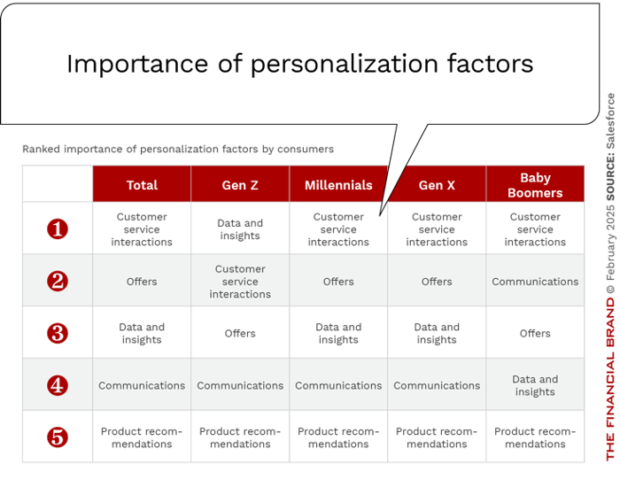

The research shows that personalization expectations have evolved beyond merely including a customer’s name or current product ownership in communications. Today’s consumers, especially the critical Gen Z segment, expect their financial institutions to deliver data-driven insights, customized customer service,= and personalized offers. Rising expectations across all demographic segments require banks and credit unions to reconsider their strategies for investing in technology, leveraging data, and communicating recommendations.

Service Quality Not Keeping Pace with Increasing Expectations

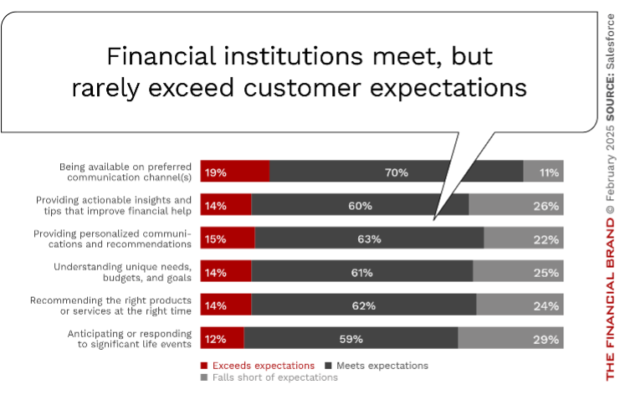

The research reveals that 84% of consumers expect their financial service institutions to act as trusted advisors rather than transactional order-takers. While most institutions meet this expectation, far fewer go above and beyond what customers expect regarding essential elements of trusted relationships.

It was found that only 26% of banking customers are fully satisfied with their institution’s customer service speed and just 27% with its effectiveness. This satisfaction gap is particularly concerning given that 47% of consumers report having to repeatedly explain their situations to different representatives.

The impact of this shortfall in service is a lower level of potential cross-sell opportunities and a continuing increase in the use of alternative financial institutions.

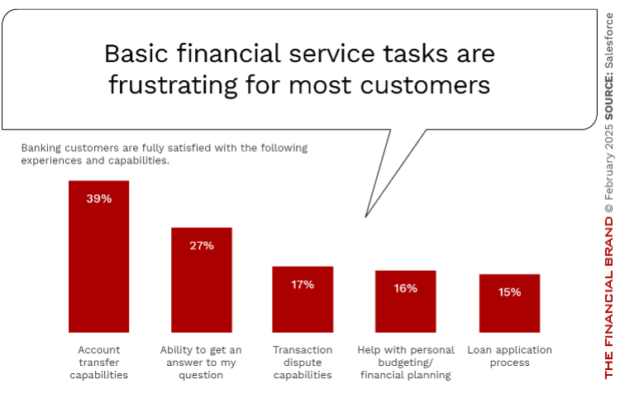

Service shortcomings are often exemplified in some of the most basic, mundane tasks. For instance, banking customers are unlikely to be fully content with what it takes to answer a question or get help with a budget. Even opening a new account can seem tedious for customers.

Financial service representatives are disadvantaged when trying to meet customer expectations without full access to customer data or AI-assisted recommendations. This presents an opportunity for organizations in the battle for new or expanded relationships.

Digital Engagement and Channel Preferences

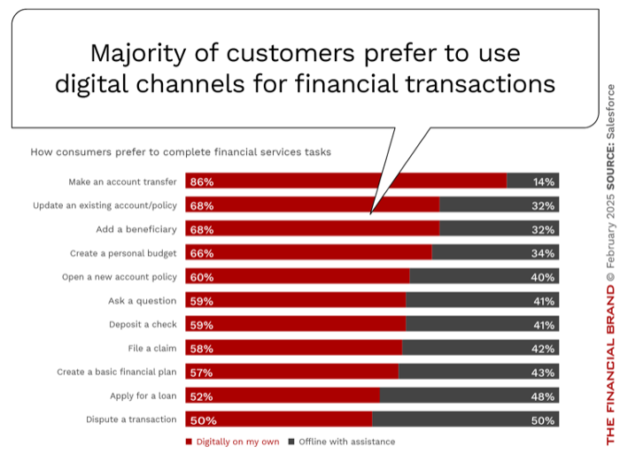

The report highlights that most consumers have transitioned to digital-first engagement in financial services. Customers now prefer to conduct most of their financial business through digital channels. This extends beyond rudimentary transactions to include product opening, customer service, and budget management.

While mobile apps remain the preferred digital channel across most demographic segments, the report emphasizes the importance of maintaining an omnichannel strategy that combines digital and human interactions. Online chat support and messenger apps rank high in customer preferences, particularly in emerging markets.

The AI Revolution in Financial Services

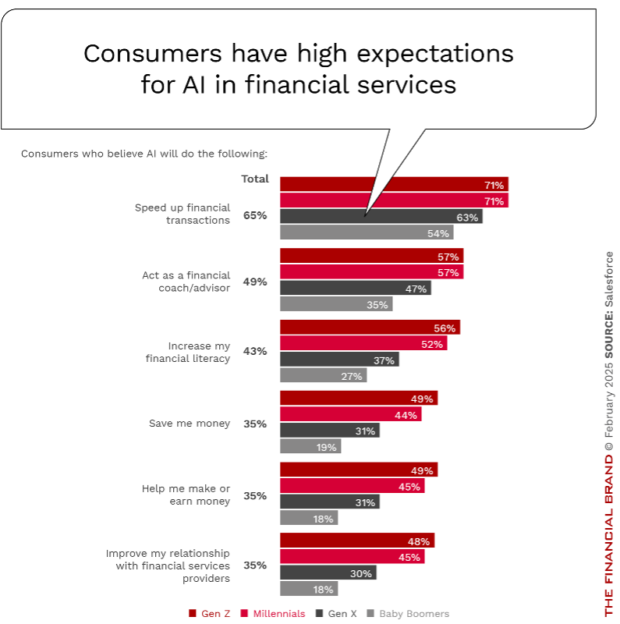

The most significant finding from the report concerns customer expectations around AI adoption. Nearly one-third (31%) of consumers believe AI is already a standard part of their financial services relationships, and over three-quarters (76%) expect AI to be more impactful by 2030. The impact of AI is becoming increasingly tangible as well, with 65% of consumers now believing AI will speed up financial transactions, a dramatic increase from 46% in 2023.

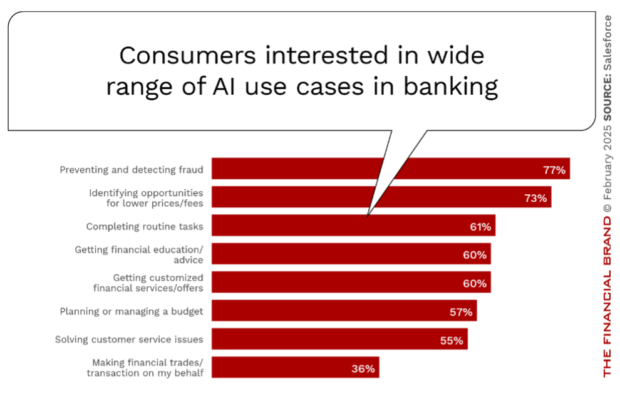

The highest acceptance levels of AI are found in areas where AI’s value proposition has already been established, such as fraud prevention (77% interested), routine task completion (73% interested), and identification of cost-saving opportunities (61% interested). Consumers hesitate more about AI’s role in more complex financial decisions, with only 36% comfortable with AI making financial trades or transactions on their behalf.

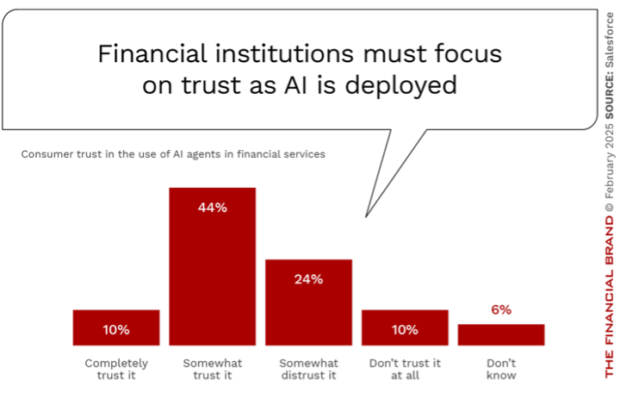

The Trust and Data Challenge

The report finds that balancing the data requirements of AI-driven personalization with growing consumer privacy concerns remains an industry challenge. Only 48% of consumers say they understand how their financial institutions protect their data, with only 44% understanding how it is used. This trust gap has significant implications, with 84% of consumers would switch financial institutions if they felt their information was mishandled, an increase from 78% in 2023.

Moreover, while younger generations show greater willingness to share data in exchange for personalized services, there’s a clear generational divide. For example, 56% of Gen Z consumers are willing to share wage or tax statement data for better service, compared to just 45% of baby boomers. This divergence requires institutions to develop nuanced, segment-specific approaches to data collection and usage.

The Infrastructure Imperative

The report highlights a significant gap between consumer expectations and institutional capabilities in data management. While 93% of financial services decision-makers agree their organizations should be getting more value from their data, 45% lack confidence in their data’s accuracy, and only 41% consider their data maturity to be best in class. With data volumes growing exponentially at an estimated annual rate of 22%, this capability gap poses a serious challenge to AI deployment and service improvement initiatives.

For senior retail banking executives, the report’s findings suggest several strategic priorities:

- Institutions must accelerate their AI adoption while maintaining transparency and trust. This includes clear communication about AI use cases, robust governance frameworks, and demonstrable value creation for customers.

- Data infrastructure requires immediate attention. The report suggests that 88% of technical decision-makers believe AI’s outputs are only as good as its data inputs, making data quality, accessibility, and governance crucial success factors.

- Personalization capabilities need significant enhancement. While customers increasingly expect tailored experiences, few institutions currently deliver them effectively. This gap represents both a risk and an opportunity for differentiation.

- Service delivery models require reimagining. With consumers expecting both digital efficiency and human empathy, institutions must develop hybrid service models that leverage AI for routine tasks while preserving human interaction for complex needs.

Finally, the report emphasizes the importance of generational considerations in strategy development. Different demographic segments show markedly different preferences for engagement channels, data sharing, and AI adoption, requiring more nuanced, segment-specific approaches to service delivery.

Conclusion

While AI presents unprecedented opportunities to enhance personalization, customer service, engagement, and operational efficiency, success demands a focus on trust, data quality, and customer empathy. Institutions that balance digital and human interactions will be best positioned to thrive in the emerging agentic AI era.

However, playing ‘catch-up’ during accelerating change is not a strategy for success. Customer expectations are evolving faster daily, and new market entrants are leveraging technology to reshape the competitive battlefield.