With demand for BNPL solutions rising, the competitive landscape has intensified as new entrants flood the market to get a slice of the pie.

Some traditional financial institutions are among the players, with incumbents like American Express, Chase and Citi providing BNPL functionality but with a different customer experience than the type that has led to the meteoric rise of pure-play BNPL providers such as Affirm and Klarna. Rather than offer BNPL at the point of sale, the biggest card issuers have been providing the service retroactively, presenting customers with the option of splitting a payment into installments after they have made a purchase with their credit card.

Banks could win greater share in BNPL if they recognize how segments of the market differ and learn how to appeal to the growing segments. In addition, banks can make gains through some unorthodox plays and can succeed even if they don’t jump into some form of buy now, pay later financing through an alternative strategy I’ll outline.

Understanding the Generational Split in BNPL Preferences

With the largest traditional institutions and the pure-plays operating different BNPL models, a generational divide has emerged regarding which option gets used most. Our research on BNPL finds that Gen Z and Millennial consumers are most likely to use PayPal which offers the standard “Pay in 4” model at the point of sale, as well as pure-plays like Afterpay. Older consumers, especially Baby Boomers, are significantly more likely to use their card issuers’ BNPL solutions.

A number of reasons creates this divide. The first is simply that Gen Zers are less likely to have credit cards in the first place and may lack the history to qualify for one yet. Pure-plays, known for lenient approval standards, make their products much more accessible. Unlike traditional credit issuers, pure-plays rarely perform a hard credit inquiry upon origination, and their products are frequently marketed with the promise of having no impact on one’s credit score.

For the Millennials who do have a credit card, the prospect of using a pure-play is also cheaper than using their card issuers’ post-purchase BNPL service. Chase’s “MyChasePlan” and American Express’s “Plan It” still charge monthly service fees, and for younger generations who are more likely to revolve and pay interest on their cards, it makes sense that they would gravitate to interest-free fixed installment plans.

By contrast, older generations are often less price sensitive. They may be content paying fees to use buy now, pay later if it brings the peace of mind of receiving the service from a regulated entity that they trust. Additionally, the older demographic using their credit card’s BNPL service have the flexibility of splitting up their purchases while retaining the consumer and fraud protection, as well as rewards, that come with a credit card.

How Banks’ BNPL Programs Can Cater to Younger Consumers’ Payment Preferences

Banking providers looking to enter the BNPL market with the broadest potential should not rely solely on offering a retroactive plan that requires credit card ownership. Instead, they should offer multiple financing options and these must be made available at the point of sale.

The retroactive model negates one of the biggest draws of BNPL — which is the seamlessness of having it available directly at the time of purchase, online or instore. The revolving aspect and hidden fees rife with credit cards are also significant contributors to younger consumers’ aversion to credit (even though BNPL is still debt). This leads them to seek BNPL solutions from pure-plays instead.

Some regional banks are already offering BNPL at the point of sale separate from a card transaction (e.g. Citizens Pay, FNBO Slice).

Secret to Drawing Young BNPL Users:

Traditional institutions can leap forward in BNPL if they integrate it with younger consumers' preferred method of payment: debit cards.

Gen Z and Millennials are the largest users of debit cards, as well as the largest users of BNPL — meshing the two seems logical from a customer acquisition standpoint as well as earning extra revenue. Banks earn minimal revenue from debit transactions, so tacking an installment financing fee option onto a debit card could help them earn more.

So far, for traditional players, this has been a missed opportunity. For example, American Express has been making strides to broaden the reach of Plan It, such as by implementing it at the point of sale on Delta’s website. Their recently launched debit card would have been a prime opportunity for them to integrate Plan It as an added incentive for signing up for the card.

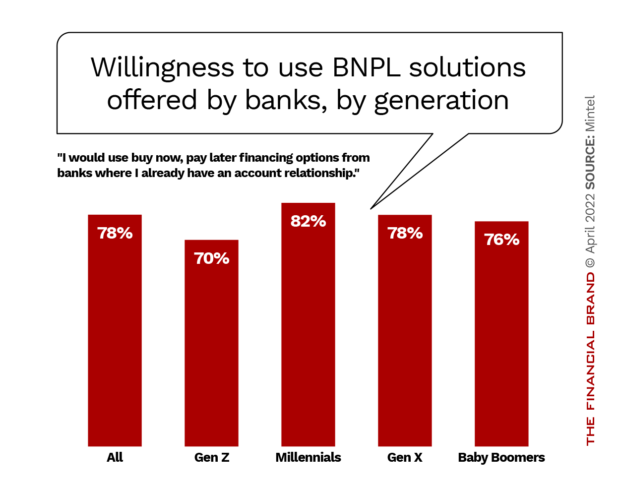

Remember, Klarna and Affirm don’t own the younger market. 70% of Gen Z and 82% of Millennials say they are willing to use BNPL solutions backed by their regular financial institutions, so there is significant openness to the prospect of banks supplementing the payment methods younger consumers gravitate toward. Banks that can capture younger segments with their debit-linked BNPL offering will also have another stream of data to assess creditworthiness, with the potential of retaining these customers by extending to them more lucrative products like credit cards as they demonstrate an ability to repay.

Debit-linked BNPL offerings are already out there — but most notably with Affirm’s Debit+ card, as well as other debit announcements by Klarna and Zip. (The savings accounts behind Affirm’s Debit+ are held by Cross River Bank.) Pure-play BNPL firms are leveraging the strong usage of their services by catering to their target audiences’ (Gen Z and Millennials) payment preferences, providing them with a physical card that bridges the gap between BNPL purchases and everyday spending.

The probability that these providers add on rewards to these cards is highly likely, and will only increase brand stickiness and make the prospect of cross-selling other financial products easier down the line.

Banks’ don’t have unlimited time to counter this move. And they have the tools, balance sheets and consumer trust to match these offerings. They mustn’t let this opportunity pass them by if they want to retain the business of their younger customers.

Read more:

- Banks Getting into BNPL Should Study CFPB Complaints First

- Why Consumers Don’t Think BNPL Is ‘Debt’ (and Why It Matters)

- Lender Alert: Struggling Consumers Using BNPL Almost 4x More Than Others

Banks Must Pursue BNPL Carefully to Avoid Fostering Credit Issues

While preferences for BNPL providers differ by generation, the one constant driving usage of this service is ultimately the convenience of a fixed payment schedule: 38% of BNPL consumers say “It’s easier to make payments” as the reason for choosing buy now, pay later financing. Other motivators driving BNPL usage include avoiding credit card interest. Most “Pay in 4” plans do not carry interest, and fees are only assessed by some providers if a customer fails to pay off an installment. As such, the prospect of an interest-free fixed payment plan is another strong driver.

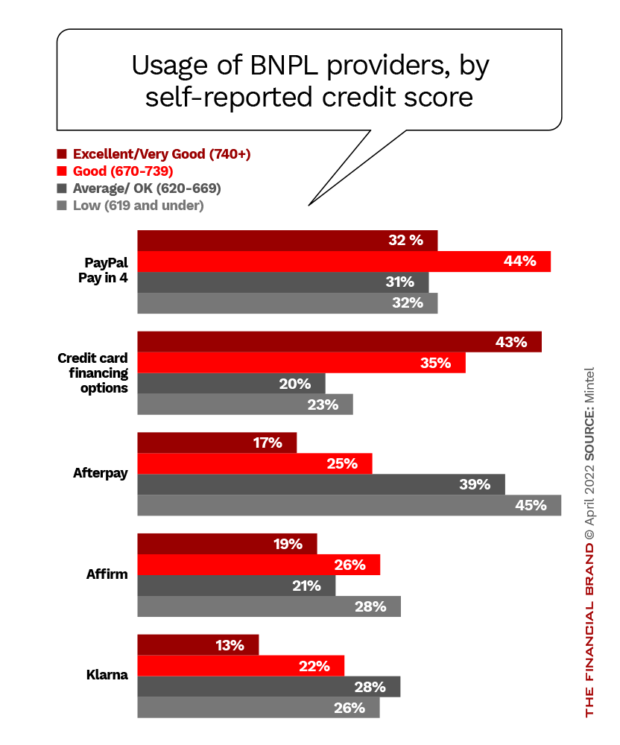

The most glaring reason for using BNPL services, however, is the fact that consumers could not afford a purchase in full, with 38% of BNPL consumers citing that as the reason for use. Even more concerning is the fact that a significant share of BNPL users have subprime credit scores, which could lead them to take on even more debt than they can afford given how lax approval standards are with most BNPL services.

Financial overextension has been top of mind for regulators and policymakers taking aim at BNPL, given how accessible the product is to less financially stable individuals who risk further debt accumulation.

See all of our latest coverage of BNPL.

Invest in the Financial Health of Customers Using BNPL

With financial overextension a serious concern of using BNPL, banks that have no interest in entering the market can still provide value by creating tools that help their customers better manage their BNPL plans.

One way to do this is to help with financial management.

These banks can offer the option to add enable consumers to input their outstanding BNPL plans to their bank’s mobile app (such as SoFi Relay and Marcus Insights). This can give them a consolidated view of all their BNPL activity on top of their other financial obligations. Given the short duration of “Pay in 4” plans, and lack of hard credit pulls, customers can have multiple plans open simultaneously with multiple providers.

Banking Tools to Corral BNPL Debt:

Offering BNPL users a comprehensive view of their outstanding plans could help avoid potential of mismanagement and the subsequent late fees that could result.

Offering a feature like this ties into other pro-consumer moves among banks, most notably removal of overdraft fees at some banks (Ally, Citi), offering tools to better manage overdrafts (PNC, Huntington), and providing early payday access (Capital One, Discover).

Banking institutions can go a step further and educate customers about the lesser-known facts about BNPL.

This includes how BNPL lacks the consumer and fraud protection offered by credit cards. In addition, something else consumers should know is how, despite the absence of late fees, some providers will still report multiple missed payments to collections and drastically impact one’s credit scores. Educating consumers in this way can help them make more informed and financially responsible decisions as they use BNPL products, leaving them less vulnerable to the pitfalls.

Financial institutions that can leverage their positions as subject matter experts in financial wellness could thus gain two invaluable things in any banking relationship: trust and loyalty.

Free Email Newsletter: Subscribe to The Financial Brand for Banking News & Trends