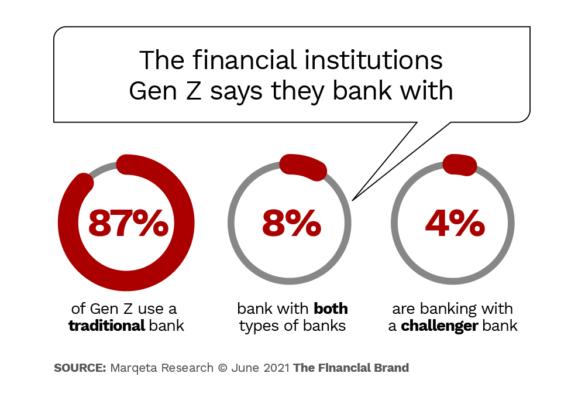

Almost nine out of ten Gen Z consumers (87%) still prefer traditional banking providers to the competitive neobanks and fintechs who are dominating the news, according to a new study by Marqeta, a fintech payments platform.

“While it is a common belief that Gen Z is digital-only and will bank with whatever app they find most useful, our data shows they currently have a strong preference in opening and having bank accounts with well-established banks,” Marqeta’s report reads.

Ian Johnson, SVP of Marqeta’s Europe group, said in a statement he thinks Gen Z may even be yards ahead of previous generations in financial maturity.

Gen Z — which endearingly earned the nickname “Zoomers,” in a head nod to the “Boomer” generation — is not nearly as worried about the same things that Millennials were, says Johnson. He thinks they have a more “practical approach to personal finance.”

Johnson goes on to explain that the financial institutions who can cater to Gen Z’s concerns very well may be the ones who can earn the loyalty of the trend-setting generation. They can do this by introducing them to ‘Buy Now Pay Later’ products or teaching them how to budget for a future home, for example.

( Read More: 13 Major Insights Into Gen Z Driving Banking Behaviors )

Although challenger banks are slowly pulling in more consumers — expected to top 20.2 million users by the end of 2021 — only one in ten (12%) of Gen Z consumers say they are banking with neobanks, like Monzo and Revolut, in any capacity. Of these, only 4% actually use challenger banks exclusively and the other 8% say they bank with both traditional players and neobanks. (The survey was conducted in the U.K., where neobanks are more established than in the U.S.)

To add to the shock factor, Marqeta also found in its research 80% of Gen Z still use cash on a weekly basis, which the company suggests is a sign the new kids on the block aren’t ready to forgo their physical wallets.

Gen Z is known for being resilient, financially sharp and hyper socially-conscious. However, the latest generation entering the financial industry is coming in at the same time challenger banks are gaining ground. So, it’s easy to understand why legacy institutions are concerned with losing out on the newest market segment.

A Shocker:

Gen Z still uses cash and almost 90% of them are banking with the traditional financial institutions. It’s not too soon (or too late) to market to the youngest people doing banking.

Gen Z is expected to be an influential generation of consumers. To date, Gen Z accounts for a fifth of the U.S. population, which rounds out to about 67 million people. Seeing as they were born between 1995 to 2015 (give or take a few years), the oldest ones are graduating out of their teens and entering young adulthood.

What’s even more interesting is the Zoomer generation already wields a purchasing power exceeding $143 billion, according to Business Insider. And Boston Consulting Group projects that Gen Z spending power will increase by as much as 70% over the next five years.

It’s worth looking into what it takes to really keep them interested.

Gen Z Is Concerned About Long-Term Goals

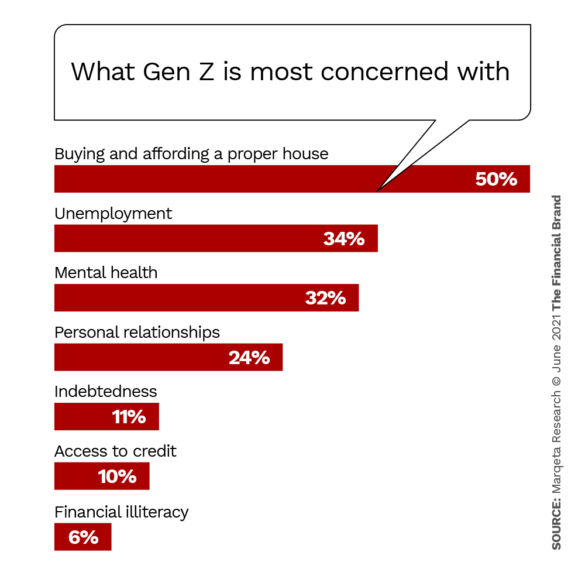

Anyone studying the Gen Z mindset can attest the generation watched the financial mistakes of their predecessors and as a result are a frugal group. Whereas Millennials used to fear for their credit scores and mounting college debt, one out of every two Zoomers say — in the next ten years — buying a property will be their biggest life challenge, according to Marqeta’s research.

Over 20% of them consider a future house to be their top financial priority, while 18% are prioritizing starting or building up their emergency funds and another 17% are focused on cutting down their student debt.

The Center for Generational Kinetics echoed the data found by Marqeta, noting 91% of Gen Z plan to buy their own home and nearly seven out of ten think retirement saving is a top priority.

“Gen Z’ers saw their parents — most likely to be Baby Boomers or Millennials — struggle through the Great Recession, and many are saddled with student debt,” writes Nanda Kumar in the Bankless Times. While older generations likely weren’t fiscally prepared for retirement, Gen Z plans to be ahead of the game.

They’re Loyal Now, But Keep These Things In Mind

Although the generation now entering adulthood still likes the banking providers their parents are used to, they crave new technology. They want ease of access and intelligent automation.

“Young people have huge expectations. They’ve grown up as digital natives. They expect everything in real time,” said Louise Hill, Co-founder & Chief Operating Officer of neobank gohenry, during a Sifted panel.

This isn’t a new concept — financial institutions already feel the pressure and they’re partnering with fintechs to up their digital banking game. And that’s good timing — Gen Z says they might be interested in banking with leading technology companies like PayPal, Apple, Amazon and Google, according to Marqeta.

But, it may not be too difficult to retain their loyalty. Here are a few key points Gen Z wants banks and credit unions to focus on:

Social Media (But Not How You Think)

Maybe you read ‘social media’ and thought, “We still need to revamp our social media profiles?!” But, there really isn’t much proof showing Gen Z is that concerned with seeing their banking provider on Instagram or TikTok.

Instead, according to Marqeta’s research, more than one in five Zoomers say easier ways to pay for services and products through social media would “be a key feature is selecting a financial services provider.”

Food for Thought:

Innovating the way Gen Z and other consumers pay for products and services on social media and online shopping venues could be an easy win for traditional financial institutions.

Offers, Incentives & Better Prices

More than half of Gen Z (54%) would like to see their bank or credit union break out more offers and incentives to guide the customer experience.

Furthermore, almost one in three say they want better prices and less fees tied to banking, two elements which neobanks and challenger banks are already supplying.

A Guiding Light

CU Management says Zoomers (and likely the generation to follow) care about the purpose, values and mission statement a banking provider presents. If those things don’t connect with them, “they stop paying attention.”

“If young people don’t have a good perception of a company and don’t find any information that challenges their existing perception, their new belief system will prevent them from being engaged in that company’s culture and purpose (even if its purpose is noble),” wrote Arnessa Belin in CU Management.

As neobanks pilot their strategies in the financial industry, they often lead with their brand purpose and Gen Z is noticing. Take, for instance, First Boulevard — which launched in 2020 out of Atlanta, Georgia — and which loudly advertises its motto: “Unapologetic Banking Built for Black America.”

On the other hand, New-York based investment advisor Ellevest says its ultimate goal is getting women to feel comfortable with banking and investing.

How To Keep ‘Em Hooked Long Term

Gen Z kids, even though they feel like they have a better hold on their long-term financial goals, are still very stressed out. The American Bankers Association ran a report titled “Stress in America 2020,” which concluded the oldest of the generation are scoring stress levels significantly higher than their predecessors.

One result of that, according to Marqeta, is that Gen Z wants bank apps that are easy to use. The company lists key features Gen Z expects in a mobile banking experience:

- Contactless functionality

- Good interest rates

- Aesthetically pleasing app layouts

- Ability to pay and make easy money transfers with their phones

- Modern and personalized card design

- Tips on how to invest and save money

- Discounts and rewards

- Strong and reliable security