Does Your Bank Belong in Stablecoins, Tokenized Deposits … or Both?

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Industry insiders often talk about tokenized deposits and stablecoins in the same breath. But that doesn’t mean they’re the same thing.

What’s the difference? Ron Shevlin, chief research officer at Cornerstone Advisors, explains that tokenized deposits are an efficiency play. Stablecoins, on the other hand, represent a competitive strategy.

“It’s really two separate decision paths,” says Shevlin.

Need to Know:

- Among banks, 9% plan to invest in or implement tokenized deposits in 2026, while 57% have discussed this at the board or executive level, according to Cornerstone’s “What’s Going On In Banking 2026” report.

- Shevlin sees a slow but steady roll in tokenization. For example, among banks, with 9% currently moving forward, he sees that reaching no more than 15% in 2027, absent intervening events that hasten adoption.

- Among credit unions, 5% plan to invest in or implement tokenized deposits in 2026, with 42% having discussed it at senior levels.

- Regarding stablecoins, 5% of banks are investing in this, or will implement it, in 2026, and 71% have discussed at senior levels. Only 24% of the banks aren’t looking at stablecoins in some way.

- Among credit unions, 8% will invest in or implement stablecoins in 2026, and 63% have had senior level discussions. 29% are not looking into the matter.

The Right Perspective is Key

Shevlin gives some guidance:

Tokenization: “No consumer, no business is going to say, ‘Oh, you’ve tokenized my deposit. That makes me want to do more business with you,'” says Shevlin. “That’s never going to be a selling point. But tokenized deposits drive internal efficiency in terms of reducing reconciliation when money moves between accounts.”

Customers will see the results of that internal efficiency, in time.

Tokenizing deposits transforms deposits into on-blockchain representations of those deposits, allowing the money to move with no time lag. Shevlin advises banks and credit unions to move in the direction of tokenization.

“If I were the CEO of a bank, I don’t know that I’d really want to be the last bank moving its deposits to a tokenized world,” says Shevlin. “It’s a matter of when, not if.” Right now, he sees a three-to-five-year time frame for widespread adoption.

Stablecoins: For banks that can come up with use cases that serve specific markets’ needs, stablecoins are a different matter.

“The stablecoin decision is all about the competitive market,” says Shevlin.

Use cases are developing in commercial payments, cross-border payments, and treasury management that, for the right customer base, will be a big deal and worth changing banks for. Shevlin says the ability to set up smart contracts, in which self-executing payments are made when goods or services change hands, will have much appeal for some firms, once mechanisms for verifying delivery are in place.

The competitive decision institutions must ask, per Shevlin: “Is the juice worth the squeeze?” Getting involved in both types of assets will require most institutions to invest in outside technology and, potentially, partnerships.

Read more: Your Bank Will Lose Customer Accounts Without a Digital Asset Strategy

Where Strategy Intersects Regulatory Clarity

Cornerstone’s survey probed institutions’ current approach towards tokenized deposits. The leading answer in the study for both banks (37%) and credit unions (29%) was that they are awaiting regulatory clarity. Among banks 29% said they were in early exploration of use cases and partners, with 18% of the credit unions likewise exploring possibilities.

A third of the banks (33%) and nearly half of the credit unions (47%) said they weren’t familiar enough with tokenized deposits to answer.

Is regulatory uncertainty really holding up tokenization? Perhaps, but “I think that’s a horrible reason, and just an excuse for just not getting their act together on it,” says Shevlin. In any event, he doesn’t see a “hockey stick” growth curve, in part due to financial executives’ habitually conservative nature.

Stablecoins come into focus. On the other hand, last year’s passage of the GENIUS Act will make a difference to the adoption curve for stablecoins. (GENIUS stands for the Guiding and Establishing National Innovation for U.S. Stablecoins Act.)

“A tokenized deposit is still a dollar, it’s just tokenized,” says Shevlin. “A stablecoin is not a dollar, it is a cryptocurrency that, thanks to the Act, will now have some regulatory rules around who can issue them, what can be done with them, and how they are backed. Stablecoins have become relatively safe crypto assets, unlike Bitcoin and all the other crazy cryptocurrencies that are not backed by anything.”

Reality check: One argument that won’t wash with Shevlin is that banking should jump into stablecoins simply because $26 trillion in stablecoins were processed in 2025. That’s a bogus point, he says.

“Strip out crypto trading and you’re looking at $2 trillion in real payments and treasury activity,” according to Shevlin.

Read more: Why the Future of Banking Lies at the Intersection of AI and the Blockchain

Should Interest Payments on Stablecoins Give Bankers Pause?

Bank and credit union executives’ attention to stablecoin deposits has been dominated by the issue of whether they can pay interest. There is widespread concern that if they pay interest — technically, that is not permitted under GENIUS — they could suck deposits out of the banking system and transfer much of the money to Treasury securities used to back stablecoins.

“But that’s not the factor that drives whether or not you get into stablecoins,” says Shevlin. “What does drive it is whether you see opportunities to use stablecoin as a payment mechanism for competitive advantage.”

But what about disintermediation? Shevlin believes the interest-payment issue has been overblown. He draws a parallel with high-yield savings accounts to make his point:

“You can go to Bankrate.com and find providers who are paying huge interest rates on deposits. Do you know what their individual market share is? Not much bigger than zero. They get some money, but we have not seen a mass movement of funds. Look how long the mega banks have held a huge share of deposits paying barely anything. So, who cares if Coinbase comes out with 6% or 7%?”

Shevlin thinks some perspective is needed. For example, there is some feeling that millennials and Gen Z, for example, will migrate.

“But millennials have had 20 years of being adults now,” he says, “and they are not putting all their money into nonbank providers. I’m not buying that argument.”

Banks also have a card to play: account pricing. Shevlin points out that consumers try to avoid fees and do so by maintaining balances. Institutions can make it plain — move money out and you’ll start paying monthly fees again.

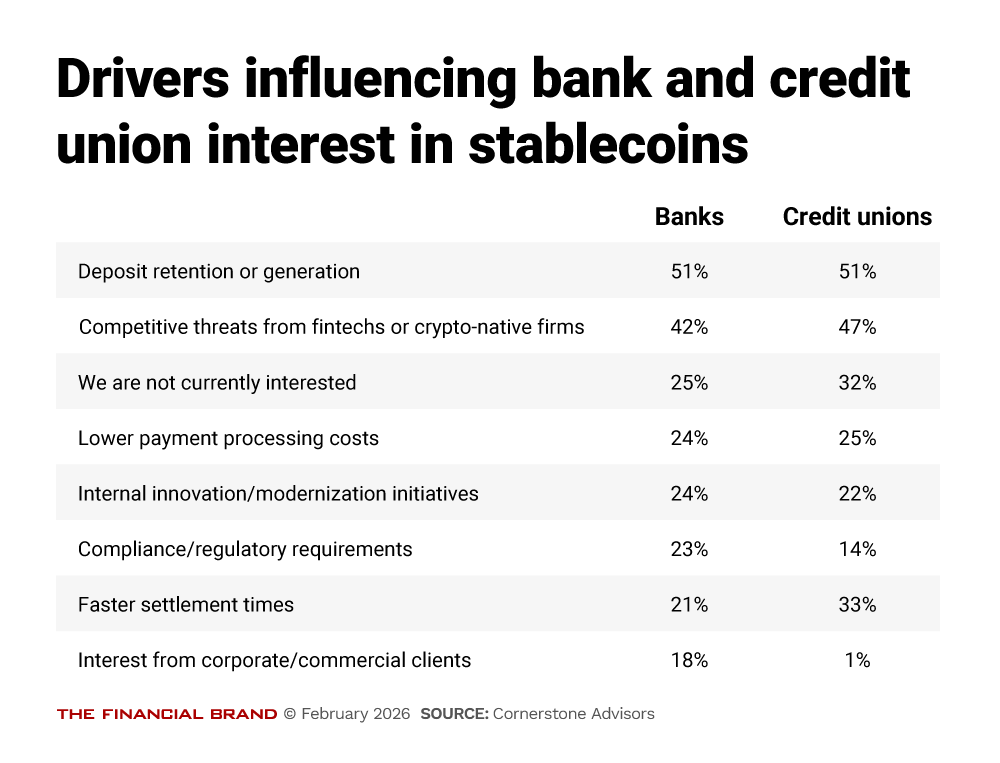

Referring to the table above, Shevlin sees the top two lines, “deposit retention or generation” and “competitive threats from fintechs or crypto-native firms” as two sides of the same coin. What impresses him most is line five, “internal innovation/modernization initiatives.”

That makes him optimistic that more banks and credit unions will focus on that in time.

Read next: How Proposed ‘Skinny’ Fed Accounts for Fintechs Could Alter U.S. Payments