Digital Wallet Paze Leans into Security and Speed as Shopping Season Looms

After some bumps, Paze, the banking industry's online digital wallet, is wading into its first holiday shopping season, seeking broad acceptance among consumers and merchants. This year, the owner institutions (as well as bank and credit union clients of Elan) will offer Paze to card holders. Access for other banks and credit unions will likely follow in 2025.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Anything new in the consumer payments sector should be in place by late summer to have a shot at getting used during the holiday shopping season. Paze, the banking industry’s online-only digital wallet held a combination press conference and launch party of sorts at the end of September to mark the fact that this new ecommerce checkout solution “is now available” for more than 125 million credit and debit card accounts across the U.S.

The organization was planting a flag on the right side of that industry deadline. Now consumers just have to take up the flag.

That phrase —”is now available” — is important. By itself, the number of cards represents a huge slice of American consumers, enough to grab the eye of any ecommerce merchant — 125 million potential purchasers, give or take. Paze, offered by the Early Warning Services consortium, is promoting its service as a convenient and private alternative to that bane of ecommerce sites: a checkout that requires manual input of card numbers and security codes in lieu of establishing an account with the merchant.

And shoppers can be fickle and lazy. Consumers encounter enough friction in many checkout routines that they abandon their shopping carts — anathema to merchants, said Catherine Murchie, head of operations at Paze, during the event. Simply having to pause, go to another room to retrieve a plastic card from a physical wallet, and return to a laptop, tablet or phone to complete a purchase, can be enough to slay a sale.

Paze eliminates the need for providing card information to merchants at all, by tokenizing payment information such that merchants never have it, and eliminating payment data entry. That gives the cardholder ease, speed and data security simultaneously. Merchants who provide access to the Paze wallet for site visitors hook them into their credit and debit cards from participating financial institutions where they have relationships.

For Paze, it’s one thing getting merchants to incorporate it into their sites. The other is putting the wallet into hands of participating banks’ credit and debit card holders. Many have been automatically enrolled in Paze and already have a Paze wallet that includes all cards with any Paze-member institution.

However, they have to activate the wallet in the course of their first transaction on a participating ecommerce site. Until they do — and assuming they don’t exercise their right to opt-out of the wallet — their Paze wallet is more or less dormant. Not unlike a card kept in a drawer.

That 125-million figure makes a potentially powerful user base — if cardholders claim their wallets and if they use them and if there are enough participating merchants to use them at.

So when Paze officials and bankers interviewed from participating EWS owners are asked for hard projections on usage, many answer that it is too early to be specific. (The owner banks are Bank of America, Capital One, JPMorgan Chase, PNC Financial Services, Truist, U.S. Bancorp and Wells Fargo.)

Paze is making its first broad frontal attack on ecommerce payments at a time when cross pollination between online/point of sale payments is the order of the day in wallets in the U.S.

In early September, PayPal unveiled its “PayPal Everywhere” push, stressing that its longtime digital payments tools could be used at point of sale. In June, Apple announced the expansion of the ability to use Apple Pay for website-based checkouts in all browsers beyond its own Safari. During the summer, Apple also announced that access to the near-field communications chip in iPhones would become available to developers, to enable qualifying companies to offer their own in-app payments capabilities.

So for Paze, this holiday season, “is not about specific numbers for us. It’s about awareness,” says Murchie. “It’s about the build. It’s about the longer term. It’s less about how many transactions you’re getting and more around, do people understand what Paze is?”

Read more: Could Walmart Move Accelerate Instant Payments, Cutting Out Mastercard and Visa?

Cranking Up Paze for 2024’s Shopping Season and Beyond

Murchie is a recent arrival at Paze, coming aboard in June 2024. She compares the service’s situation to the development of Zelle, which was also originated by EWS and its owner banks in 2017.

“P2P was a crowded market when Zelle came in,” says Murchie. She explains that there were many other providers of person-to-person payment services and it took Zelle some time to become the largest person-to-person payments app in the U.S.

A 24-year veteran of Mastercard, Murchie, in an interview with The Financial Brand, says she can look back on other payments projects that took much time to build out. One was Mastercard PayPass, which became contactless payments and is now so ubiquitous that it’s really a feature now, not a distinct product. For some time, issuers, merchants and consumers constituted a challenging three-sided adoption proposition for PayPass.

Paze has taken some time to reach the broad ecommerce market in a highly visible way. News of its development broke in January 2023 in a Wall Street Journal scoop and initially the plan was to get the new checkout scheme rolling in time for the 2023 holiday shopping season. That didn’t happen.

In latter 2023, revised plans called for a phased rollout in 2024. This effort included spotlighting key merchant accounts such as Omaha Steaks. (Paze’s original managing director, James Anderson, left the company in July 2024 after nearly two years. At the launch event Early Warning announced that Serge Elkiner would be coming aboard as general manager, from a senior post at Visa.)

With the developments of wallets encroaching from their online or physical venue to the opposite sides, why not take Paze there, too, providing an industry-owned digital wallet that cardholders could wave at the point of sale?

This question was put to Saad Khatri, Chase managing director for commerce payments and wallets, during a panel discussion at the Paze media event.

“It’s a good question, actually, that’s come up before. The answer is, ‘Not at the moment’,” said Khatri. “I think there’s still massive opportunity with ecommerce and that continues to grow, especially as it relates to digital wallets. It’s the curve that’s going up. We’ll keep evaluating the idea [of mobile], but I think our roadmap is quite full just with ecommerce.”

When word of Paze first leaked in early 2023, some commentators argued the banking industry was late to the game with a wallet that only worked on websites.

Khatri was asked if Paze is an offensive or defensive move. He declined to comment directly, but said it behooved banks to meet consumers where they had needs. During his time at Paze, James Anderson had remarked that existing mobile digital wallets were already pretty good but that the online experience could be improved tremendously by what Paze was developing.

In a recent interview on The Financial Brand, Nilesh Vaidya, global head of banking for Capgemini, said that he saw good potential for Paze after it had “a little bit more runway.”

Read more:

- Mobile Debit Card Payments Are Ramping. But the Economics for Issuers Are in Flux

- Affirm Sees Profitability in 2025 as its BNPL Products Gain Traction

- Surging Credit Card Surcharges May Push More Consumers to Cash, Debit

Putting Paze on the Shopper’s Mental Money Map

Building visibility for the fledgling ecommerce wallet is a joint task of Early Warning and the owner banks.

Paze itself launched a series of commercials for television, streaming media, social media and other channels in September to promote the new payment gateway, to get the word out that it was becoming available. The theme is how Paze puts the joy back in online shopping by eliminating the need for entering data, downloading special apps, or establishing usernames and passwords to pay each merchant.

The spots lean heavily into humor, demonstrating how three people use Paze. The father of a newborn trying to keep his baby asleep, a multitasker who does her work and her shopping online while using a step machine, and another dad who loves to shop online and tends to buy in multiples of two. He even has twin teenage daughters. (View the Paze commercials.)

Meanwhile, owner banks have their own marketing to do.

“Many of our partner banks are just starting to communicate to their cardholders to tell them Paze, how they can use it and where they can use it,” says Murchie. Much of this has occurred thus far by emails targeted to credit and debit card holders. Tracking by Comperemedia found that JPMorgan Chase started emailing back in March, to tell customers that Paze was going to be available. Bank of America and U.S. Bank emails came on the company’s radar in mid-summer. Among the three banks alone, at least 43 million emails went out by the end of September.

Email research courtesy of Comperemedia.

Khatri said early feedback from Chase cardholders, in verbatim comments gathered by marketing researchers, have been good. “We were just so pumped — it was gratifying to be able to see some of the early feedback,” said Khatri.

Read more: Consumers Have Embraced Digital Wallets. But They Also Want Them to Be Better

A Quick Tour of How Paze Works

U. S. Bank’s Ankit Bhatt, EVP and consumer chief digital officer, says it’s important to understand the function Paze plays. Some are tempted to call it a “platform,” picking up a common term from digital commerce. However, he said, Paze is strictly oriented towards payments and is best described as a “gateway,” a dedicated way to pay. Platforms can perform multiple functions beyond handling payments.

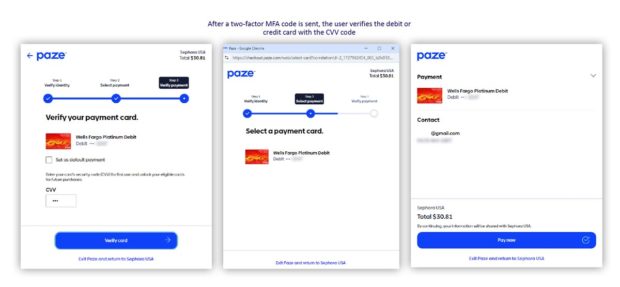

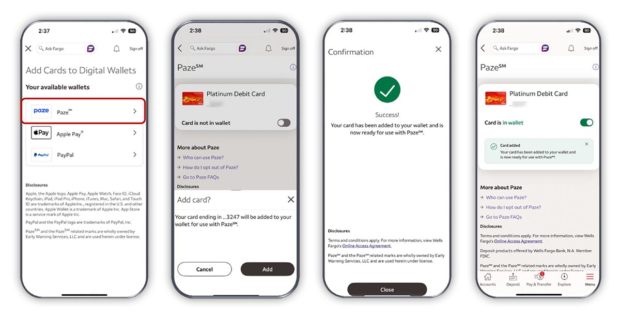

The following sample flow for a purchase on Sephora was produced by Keynova Group, which maintains real accounts with major banks in order to study mobile and online offerings closely as a customer.

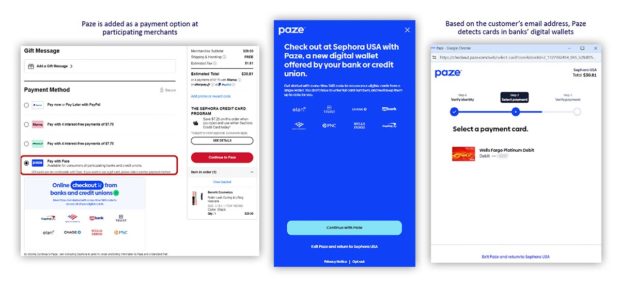

In the screens below, a Wells Fargo customer can choose among multiple checkout modes, including, “Pay with Paze.” When the consumer opts for Paze, they input their email address and this brings up all cards provided by participating banks that have already been populated in the consumer’s Paze wallet. The cardholder can select which card will be the default card, the one that comes up first. (This can be set differently for each Paze merchant that a consumer visits. For example, someone could set one bank’s card as the default for a purchase from 1-800-Flowers and a different eligible card for a Sephora purchase.)

Courtesy of Keynova Group

Banks can also enable the addition of more cars into their Paze digital wallet. In the case below, the Wells Fargo consumer could choose between three digital wallet apps. In the case illustrated they can add the card to their Paze.

Courtesy of Keynova Group.

Read more:

- 6 Innovative App Features Pushing the Mobile App Experience Beyond Transactions

- Offer ‘Test Drives’ of Mobile Banking Apps for a Marketing Advantage

What Role Will Incentives for Cardholders Play for Paze?

Early in the development of Paze commentators speculated that as the new wallet in the crowd the company was going to have to provide incentives to persuade institutions’ cardholders to try the wallet and to go on using it — something like “Paze Points.” (A made up term.) Other payment services have been cooking up incentive programs, taking a leaf out of the credit card business.

That’s not the way things are developing so far for Paze.

Catherine Murchie doesn’t see Paze-only incentives as a smart move for Early Warning. Among other reasons is that on some levels it can be seen as competing with the merchants that are looking to Paze to build their business. She points to Sephora, the beauty products company, one of the major merchants accepting Paze on its site thus far. Sephora has “Sephora points” and Murchie says Paze doesn’t want to do anything that could distract a customer from a merchant’s own incentive program. Promotional partnerships, on the other hand, could be helpful to Paze and its merchants.

At U.S. Bank, experiments in joint incentive programs between the bank and its merchants who accept Paze have commenced, according to Ankit Bhatt. He says this partnering to stimulate usage is helped when a bank has both a card issuing side as well as a merchant card processing operation. He says that the bank has been testing offers that tie back to values that merchants accepting Paze can offer customers.

Read more: Why Cardholders Are Ditching Miles and Points in Favor of Cashback

A Question Mark: When Do Other Institutions Get to Join Paze?

Zelle began as a service only for the owner banks, initially, but now many banks and credit unions that aren’t Early Warning owners offer Zelle to their customers. They pay fees for that usage.

At present, merchants pay nothing extra on a purchase to do it through Paze, just the interchange fee already applicable to the underlying card. The owner banks processing through Paze pay a fee that goes to Early Warning.

Murchie points out that roughly 1,000 smaller banks and credit unions can avail themselves of Paze though U.S. Bancorp’s Elan subsidiary. As for other players, she thinks they’ll be able to join Paze sometime in 2025, though it’s not firmed up yet.

However, while Zelle needed ubiquity to create a network, broadening access to Paze among banking institutions would seem to be splitting up the same pie into more pieces. Why share?

Murchie disagrees, explaining that this is a case where cooperation will do all more good than competition. Ubiquity will help Paze achieve more visibility and acceptability. That, she says, helps all institutions.