Payments in 2025: 5 Strategic Priorities for Bank Execs

In a new report, Deloitte interweaves several trends in and around the payments space to argue that banks need to move aggressively on multiple fronts – including product development, technology and partnerships, CX and fraud prevention – or risk losing their grip on retail banking customers for whom payments is the core of their financial lives.

By David Evans, Chief Content Officer at The Financial Brand

Simple Subscribe

Subscribe Now!

The report: Shaping the future of payments – Trends and insights for 2025

Source: Deloitte

Why we picked this report: The evolution of payments shows no signs of slowing in 2025. Meanwhile, consumers are increasingly conflating payment platforms with traditional banking services, raising long-term strategic issues for retail banks.

Executive Summary

The payments landscape is undergoing significant transformation as we approach 2025, driven by evolving consumer preferences, regulatory changes, and technological advancements. A recent report from Deloitte analysis highlights five key trends reshaping the industry: the decline of checks while cash finds its usage floor; increased regulation of nonbank payment providers; further expansion of Buy Now Pay Later (BNPL) services into essential spending categories; growing adoption of integrated software vendors (ISVs) by small and medium businesses, and the deployment of AI for enhanced fraud prevention.

For retail banking executives, Deloitte argues, these trends present both opportunities and challenges, requiring strategic decisions about product offerings, technology investments, and regulatory compliance to maintain competitive advantage in an increasingly digital payment ecosystem.

Key Takeaways

- Digital payment adoption is accelerating across all sectors, with checks heading toward obsolescence while cash stabilizes at a fundamental usage level. Retail banks must adapt their payment strategies accordingly.

- Regulatory scrutiny of nonbank payment providers is intensifying, creating opportunities for traditional banks to leverage their existing compliance infrastructure and expertise.

- Small- and medium-sized businesses are increasingly gravitating toward integrated software vendors for comprehensive payment solutions, requiring banks to rethink their merchant service offerings.

- Buy Now Pay Later services are expanding beyond retail into essential spending categories like utilities and groceries, presenting new opportunities for banks to serve customers facing inflation pressures.

- AI-driven fraud prevention is becoming a critical differentiator, with successful implementations showing dramatic improvements in detection speed and accuracy

What we liked about this report: A cruising altitude view that clarifies how several trends, often seen as separate, are all pushing the banking industry into an uncertain future.

What we didn’t: Its strategic and operational recommendations are somewhat vague.

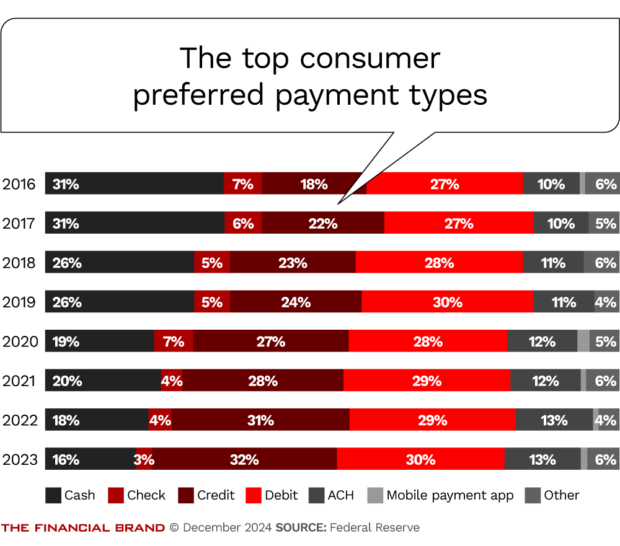

Digital Transformation of Payments Continues to Accelerate

The payments industry is experiencing unprecedented change as digital methods continue to dominate consumer preferences. Check usage is declining rapidly, with major retailers like Target joining the “check zero” movement, forcing banks to reevaluate their check processing infrastructure investments.

While cash maintains a baseline level of usage, digital payment methods, particularly credit cards and peer-to-peer (P2P) transactions, are seeing substantial growth. For retail banks, this shift necessitates a dual strategy: accelerating digital payment infrastructure development while managing the controlled obsolescence of legacy check processing systems. Banks should particularly focus on enhancing their P2P capabilities, as these transactions have seen a 12% increase in usage since 2021, while cash and check P2P transactions decreased by 10% and 2% respectively.

Just How Big Digital Wallets Are:

Digital wallets now represent 37% of e-commerce transaction value in North America, totaling over $748 billion in 2023.

Regulatory Environment and Market Structure Realign

At the same time, the regulatory landscape is becoming increasingly complex, with banking regulators expanding their oversight to include nonbank financial companies. The CFPB’s proposed open banking rule and enhanced supervision of payment applications represent a significant shift in the regulatory environment. For retail banks, this presents both opportunities and challenges. Banks can leverage their robust compliance frameworks to gain competitive advantages over fintech companies that may struggle with increased regulatory burden.

However, this also requires careful evaluation of partnerships with third-party payment providers and thorough assessment of the downstream effects of regulatory requirements on existing relationships. Banks should consider developing standardized partnership evaluation frameworks that incorporate these new regulatory considerations.

Dig deeper:

- CFPB Targets Large Digital Payment Apps, But Will It Stick?

- Credit Card Delinquency and Balance Growth Will Moderate in 2025

- Fitch Ratings: Bank Ratings Show Stability as Industry Navigates Regulatory Changes

Innovation and Consumer Experience Move to the Fore

Small and medium businesses, which drive 65% to 70% of net merchant acquiring revenues, are increasingly gravitating toward integrated software vendors for comprehensive payment solutions. This trend requires banks to either develop competing integrated solutions or forge strategic partnerships with leading ISVs.

The expansion of Buy Now Pay Later services into essential spending categories like utilities, housing, and groceries represents another crucial opportunity. With major players like Affirm offering limits up to $20,000, banks must decide whether to develop their own BNPL products or risk losing market share in this growing segment. The fact that 33% of merchants prefer bank-branded BNPL products (compared to 32% preferring fintech-branded options) suggests a strong opportunity for traditional banks in this space.

Use Cases for BNPL:

BNPL usage for grocery purchases increased 40% between early 2023 and 2024.

AI and Fraud Prevention Will Become Critical

The implementation of AI-driven fraud prevention systems represents a critical investment area for retail banks. Early adopters like Mastercard have seen dramatic improvements, including a 300% increase in speed to flag compromised merchants and significant reductions in false positives.

Banks should prioritize developing comprehensive AI strategies that encompass both fraud prevention and customer experience enhancement. This includes leveraging AI for personalized spending insights and proactive fraud alerts, similar to Capital One’s “Eno” virtual assistant, which provides real-time monitoring of unusual spending patterns.

Strategic Priorities for Banking Executives

1. Product strategy: Develop a clear roadmap for phasing out check processing while expanding digital payment capabilities, including consideration of BNPL products and enhanced P2P services.

2. Technology investment: Prioritize AI implementation for fraud prevention and customer experience enhancement, focusing on solutions that can scale and adapt to emerging threats.

3. Partnership evaluation: Create frameworks for assessing potential fintech partnerships that account for new regulatory requirements and ensure alignment with long-term strategic goals.

4. Customer experience: Design integrated payment solutions that cater to both consumer and merchant needs, particularly focusing on the SMB segment through either proprietary solutions or strategic ISV partnerships.

5. Risk management: Develop comprehensive approaches to managing new risks associated with digital payments, including cybersecurity, fraud, and regulatory compliance.

Success in the evolving payments landscape will require banks to maintain a delicate balance between innovation and risk management while leveraging their traditional strengths in security and compliance. The key to competitive advantage will lie in how effectively banks can integrate new payment technologies and services while maintaining the trust and security their customers expect.

Editor’s note: This article was prepared with AI language software and edited for clarity and accuracy by The Financial Brand editorial team.