Digital Wallets Increasingly Dominate Payments, But Cash Maintains A Stubborn Toehold

And the day is coming when Americans will continue their love affair with credit and debit without physical cards — on smartphones, in ecommerce and at point of sale.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Globally, digital payments — especially digital wallets — are poised for continued growth through the end of this decade. While the U.S. is showing similar growth, it lags the global trend and is expected to continue to do so over the same period. Worldwide, by 2030, digital payments are projected to grow beyond $33.5 trillion.

These trends, and more recounted below, have significant implications for financial product design and marketing.

Assessing U.S. Trends Versus Global Trends

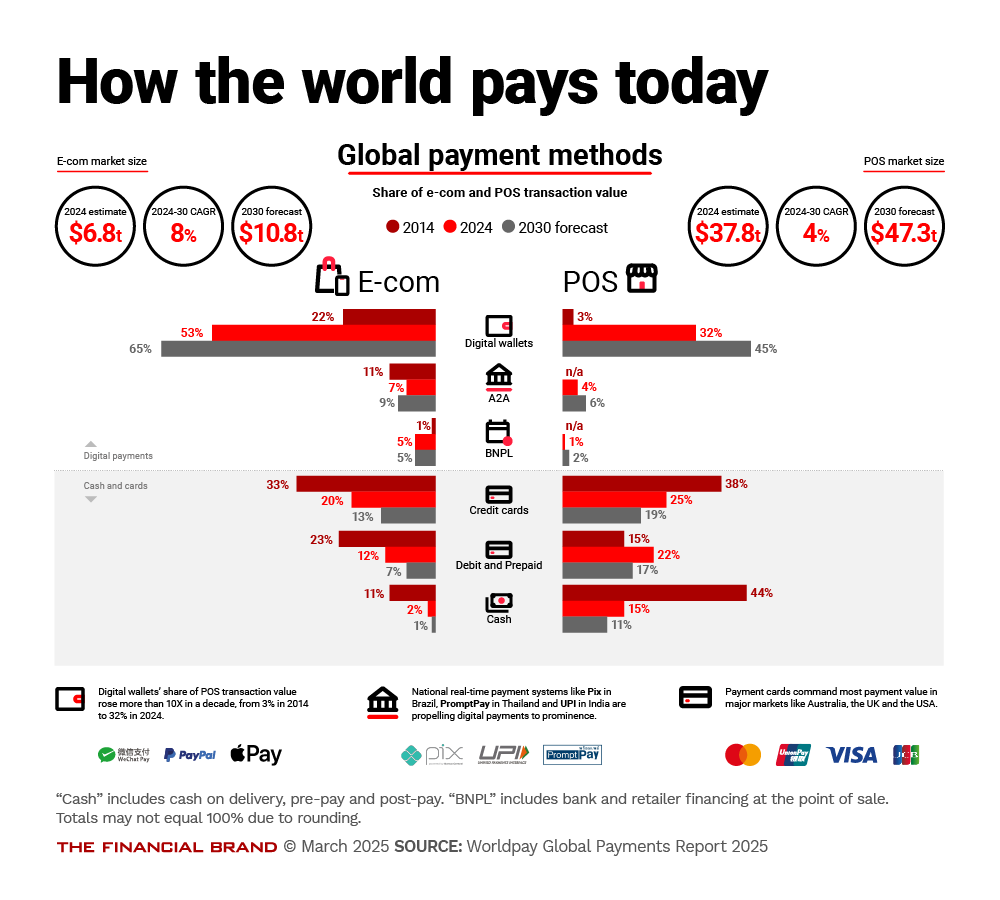

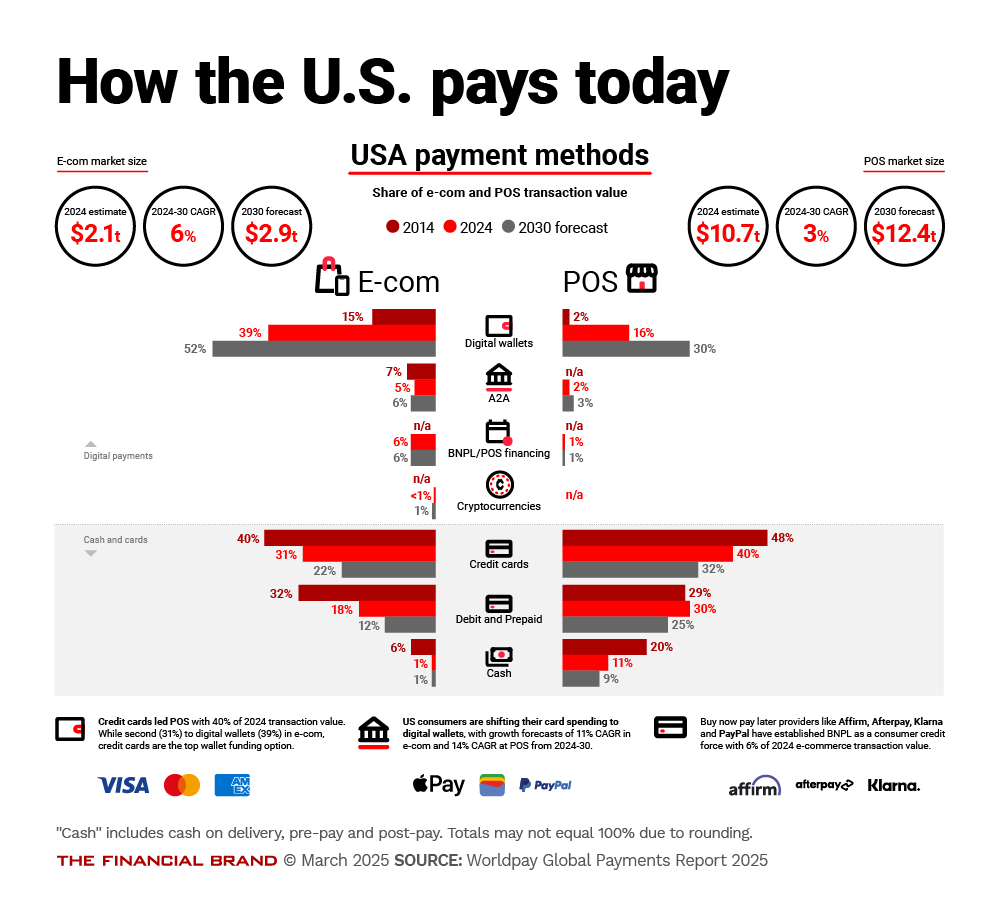

By 2030, the share of ecommerce via digital wallets is projected to hit 65% globally and 52% in the U.S. Worldwide, 45% of point-of-sale transactions will be via digital wallet, while in the U.S. this will reach 30%. Increasingly, “cards” will be accounts loaded into digital wallets, with a physical piece of plastic (or metal) no longer routinely provided to users. In the U.S., 40% of digital wallet transactions are funded via credit cards, 25% by debit cards, and 22% via bank accounts.

These overall observations come from the tenth edition of Worldpay’s Global Payments Report. The study covers payment trends in 40 countries and the collective picture worldwide. In the context of the report, “digital payments” includes digital wallets, account-to-account payments, buy now, pay later payments, and payments via cryptocurrency. Digital wallets include both funding from cards and from non-card sources.

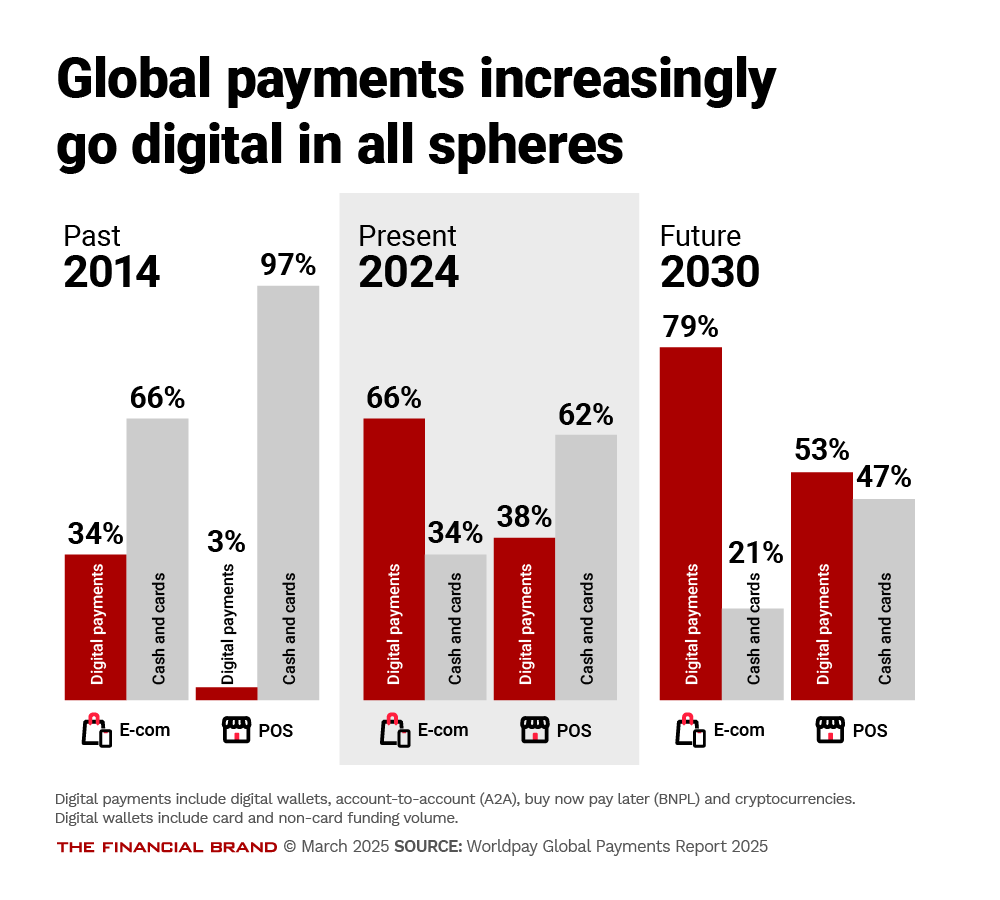

Significant change has been seen over the 10 years of the report, as depicted in the global and U.S. versions of the charts immediately below. This reflects the advent of smartphones — the iPhone was introduced in 2007 and the Android technology was introduced in 2008 — and the growth of buy now, pay later, account-to-account payments, as well as rising spending. Worldwide, the study used surveys of 66,000 consumers and secondary research, and Worldpay validated its observations with regional payments experts.

The share of digital payments versus use of cash and cards in ecommerce flipped over the decade, as shown below. Worldwide, the 34% digital/66% cash and cards became 66% digital/34% cash and cards.

And by 2030, Worldpay projects, digital ecommerce payments, at 79% share, will dwarf cash and cards at 21%. “Cash and cards,” in the ecommerce context, includes cash on delivery, pre-pay transactions (such as vouchers purchased with cash) and post-pay transactions, where an ecommerce purchase can be paid for in cash at pickup.

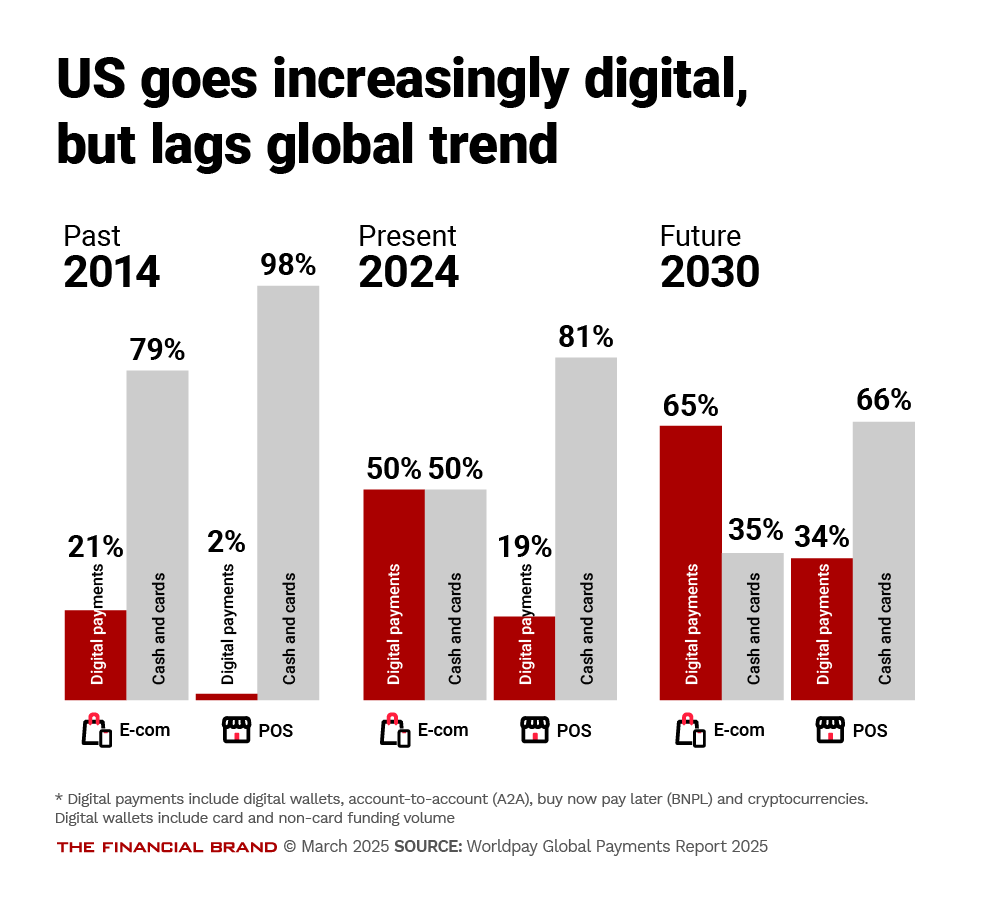

By contrast, while the U.S. has shown a similar pattern, the change has not been quite as dramatic. In 2024 in ecommerce, digital and cash and cards were tied at 50% share each (see below). The shift by 2030 will be strong, at 65% digital, but still behind the 79% expected globally.

In addition, by 2030, for point-of-sale transactions, cash and cards are still expected to be stronger than digital payments, in the U.S., versus digital pulling ahead of cash and cards on the global stage.

The evolving mix of payment choices is driven by dual acceptance, according to Jason Pavona, general manager, North America, at Worldpay, in an interview. Merchants must be willing to accept a given payment type and consumers must be willing to use it also.

Americans have an almost cultural dependence on debit and credit cards, according to Pavona. That strong preference has slowed adoption of other methods, such as account-to-account payments. In some cases, Americans must be coaxed to try new channels through incentives of some kind. Take BNPL. The early draw was no interest.

“People sometimes forget, because it was a long time ago, but Apple Pay and PayPal spent a lot of money incentivizing customers to use their products at point of sale and online,” says Pavona. “That helped the adoption curve.”

He points out, however, that adoption of Apple’s digital wallet, for example, wasn’t uniform. “When it first came out, there were a lot of people using Apple Pay in San Francisco, Boston and New York — but nobody was using it anywhere else.”

The Financial Brand discussed the continuing evolution Worldpay sees in the U.S. in light of the global trends, and the outlook in some specific areas. But first, let’s drill down into a finer comparison of the global and U.S. findings. (The 162-page report‘s findings on other regions and countries are as detailed as the recap here of the U.S. trends.)

Comparing Global and U.S. Payment Trends Channel by Channel

As the following pair of charts demonstrates, over the last decade digital wallets have taken off both worldwide and in the U.S. While the U.S. lags behind the global trend, “lags” is only a relative term. The change has been huge. In ecommerce, usage more than doubled from 15% of payments in 2014 to 39% in 2024. By 2030, digital wallets will account for more than half of ecommerce payments in the U.S.

Notable in the U.S. too is the growth of BNPL, 6%, though the study projects that that share will remain the same through 2030. But that represents a steady share of a pool of payments that keeps increasing.

Account-to-account transactions are at roughly the same level in the U.S., while usage is a bit broader globally. Worldpay’s report sees significance in developments like Walmart’s plans to implement real-time account-to-account payments (more typically called pay-by-bank payments here) in 2025. The retail giant’s blueprint taps both FedNow and the Real Time Payment Network of The Clearing House.

Even while digital payments continue to build share (aided in part by a desire for contactless payments during the pandemic), Worldpay notes that there’s been a plateauing for cash use at point of sale. As shown in the nearest chart above, paying with cash in stores and elsewhere will still represent 9% of U.S. transactions in 2030, per the company’s projections.

Globally, the study notes, cash has been finding its floor — diminished, yes, but not gone. In some markets, such as Nigeria, the Philippines, Indonesia, Mexico and Japan, where cash use is still strong, Worldpay projects that it will fall drastically by 2030.

Note this: “Cash is no longer the majority payment method in any of the 40 Global Payment Report markets.”

Read more:

Providers and Merchants Both Have Roles in Payments Evolution

Moving the needle on shares for various digital methods will depend on how the players manage the relationship with consumers, according to Pavona.

There’s almost no reason, in an age of digital wallets, that people need plastic anymore, says Pavona. He points to the fact that Apple will still send you a physical, metal Apple Card as a “historical mindset.”

Overcoming that mindset and its having been woven into culture, will depend on issuers’ marketing, Pavona believes. Decades of focusing people’s attention on the look of cards — gold, platinum and even black, and affinity cards showing off everything from sports teams to causes to dogs — must give way to more abstract, yet tangible, messaging.

This means marketing even harder on features and benefits.

“If I have an AmEx platinum card, I get X, Y and Z as a result of having that card,” Pavona explains. Communicated well, this should resonate more than the panache of pulling out a fancy bit of plastic. As that happens, the convenience and speed of the digital wallet and the benefits for using that card relationship dominate.

“There are global digital wallets that allow you to pay anywhere and then there are standalone applications that have wallet-type features that allow you to store cards.”

— Jason Pavona, Worldpay

“The goal will be to drive home the fact that you get these benefits and that’s why you want to have that ‘card’ at the top of your digital wallet,” says Pavona.

Pavona says that digital wallet competition will likely increase because major retailers see opportunity in devising their own digital wallets or mobile apps with embedded payments.

A battle is shaping up, in his view. “There are global digital wallets that allow you to pay anywhere and then there are standalone applications that have wallet-type features that allow you to store cards.”

Pavona says the challenge is to provide seamless convenience for purchasers and a reduced cost structure for merchants — while also steering the consumer to a particular issuer’s payment mechanism. Apple’s decision to open up its near-field communication chip in the U.S. and elsewhere is a wild card in this area, right now.

Some of these factors play into the future of account-to-account service in the U.S., which Pavona sees as being merchant-driven. One hurdle is providing sufficient incentives for consumers to forgo cards, which often have rewards attached. But another, significant, challenge is safety.

“One of the great things about credit and debit cards today is that there’s protection,” says Pavona. “When I hand somebody my credit card, I know that if something’s not fulfilled, I can charge it back or fight it. If the card is lost or stolen, I’m going to be protected.”

Pavona says U.S. consumers have grown used to that safety net and challengers have to match it or otherwise overcome the status quo. Consumers’ behavior relies substantially on their trust in the providers, he adds.

Read more: 7 Fintech and Payments Trends That Will Reshape Retail Banking in 2025

Cryptocurrency: Not Ready for Payment Prime Time

Digital assets of all kinds have been experiencing a resurgence in interest and certainly friendliness out of Washington in the wake of the presidential election. Still, in terms of utility, the word is almost an oxymoron in the U.S. — it’s crypto, but it’s not yet really currency. It’s much more of an investment/speculation in the U.S.

The projection in the Worldpay report is accordingly nil, for the U.S., as shown in the chart above. (The firm projects that globally crypto spending will rise from $16 billion in 2024 — a tiny subset of an estimated $44.6 trillion in ecommerce and point-of-sale spending in 2024 — to $38 billion in 2030.)

“The ability for people to actually transact with crypto is there from a long-term standpoint, but there needs to be improvements within the ecosystem to drive general usage,” says Pavona.

Pavona adds that right now the greatest challenge for crypto is stability. By comparison to fiat currencies, it doesn’t have the steadiness to be a true exchange of value.

He explains that in the U.S., the U.K., the Eurozone and Japan, while the values of currencies fluctuate, it’s at a relatively low rate.

“So in such markets something would have to be much less volatile in order to drive adoption,” says Pavona. The point where merchants and consumers both see a mutual advantage to crypto payments hasn’t arrived yet.

Digital cash in the form of government-issued central bank digital currency is something that Pavona thinks, at an indeterminate time, can get legs. The Biden administration effectively halted any further development of CBDC in the U.S. after pilot research under the auspices of the Federal Reserve was completed. But under the Trump administration things could change.

In spite of the stubborn survival of cash, noted earlier, Pavona believes this will erode.

“Given the rapid nature of how people are starting to consume using digital wallets, it will almost force the issue of easily turning cash into a digital mechanism,” Pavona says. “Having physical money around will eventually go away.”