How to Blunt the Threat of Smart Contracts and Stablecoins to B2B Payments

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Much of the attention on digital currency and agentic commerce has been focused through a consumer lens. But the possibilities of a boom on the commercial side are growing.

- One key is the possibility that smart contracts, digitally enforced payments mechanisms, will take off. Another is the potential for stablecoins to execute instantaneous payments in conjunction with smart contracts.

- Will banks be part of this trend? A noted payments consultant worries that a history of slow adoption and resistance to stablecoins on principle may let fintechs pull ahead.

Just as digital currency services are poised to take off in this country, an emerging one-two punch could represent a competitive threat to banks.

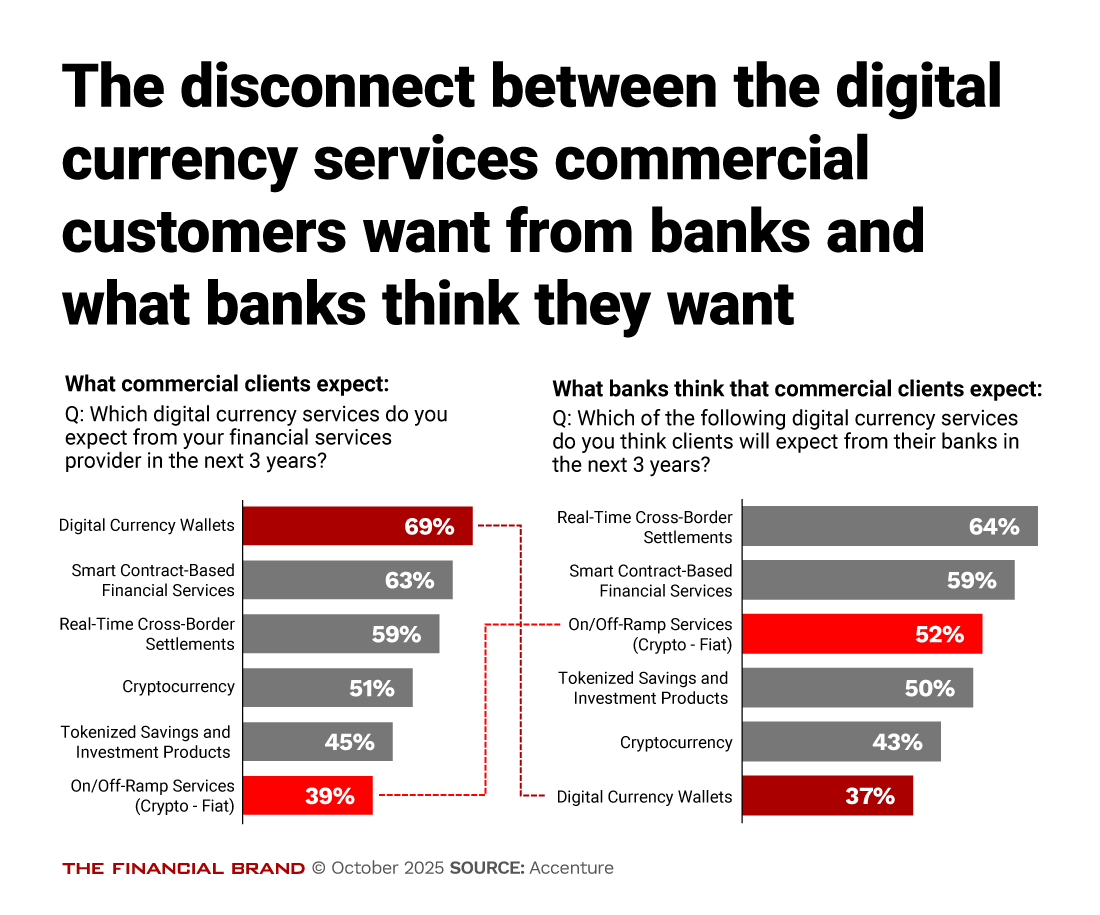

A new study, “The Future of Money,” from Accenture identified a substantial disconnect between what commercial customers expect from their financial providers and what banks think their commercial customers need.

The most dramatic difference: While 69% of the commercial clients mentioned digital currency wallets as an expectation — the most frequent choice — only 37% of the banks mentioned digital currency wallets, putting it at the bottom. The study was international, and among North American respondents, the difference was even greater: 72% of customers expect digital currency wallets, while only 28% of the banks cited them.

Another major difference: Only 39% of the international sample of business customers expect their banks to provide on/off-ramps for cryptocurrency, enabling them to change fiat currency to digital currency and vice-versa. In contrast, banks ranked this service much higher, with 52% mentioning it. (In the North American sample, the percentages were lower, 25% among customers, 48% among banks.)

One item in the ranking did come out evenly between customers and their bank providers: smart contracts. These are contracts that are digitally governed based on defined factors. When a given condition (or conditions) is met, payment is automatically executed.

In the international sample, 63% cited smart contract-based financial services, ranking second overall. Among the banks, 59% mentioned this item, also ranking second. In North America, the percentages were higher, 67% among companies, 70% among banks.

The high ranking that business customers gave to digital currency wallets, especially in the North American region, was a bit of a surprise to Brian Shniderman, senior managing director and head of Accenture’s N.A. Payments & Digital Assets Practice. He credits that to enthusiasm in the wake of the passage of the GENIUS Act this summer. Shniderman equates the customer enthusiasm with the initial excitement level over faster-payment options — which he says overshot some customers’ usage levels thus far.

“Digital currency wallets are more complicated than some people expect,” says Shniderman. “It’s going to take time to work out the details.”

The synced interest in smart contracts between the two groups struck the consultant as an opportunity banks ought to pounce on — and quickly.

“Smart contracts are actually not that difficult to deliver,” says Shniderman. “They may be one of the easiest things to accomplish in AI.”

But can banks get in the game?

Smart Contracts: An Opportunity that Won’t Hang Around

Shniderman says the concepts of smart contracts and of agentic commerce and payments appear to be converging.

On the commercial side, many companies need “smarter payments, not faster payments.” Payment rails can now carry a good deal of transaction data that they couldn’t in the past, enabling companies to embed their functions into workflows to streamline processing and payments.

Banks run the risk of being overtaken by fintechs and other players that move faster than banks historically have, Shniderman warns.

A key challenge, he says, is that banks bring the pieces to the payments game but often don’t put them together. He compares this to Legos construction sets.

“Banks just dump the Legos on the floor,” says Shniderman. “They don’t include any instructions about how to build the castle or the little race car. They don’t actually show you a picture of it, which creates value.”

As a result, they tend to leave it to customers to figure out how to put the bricks together. Consortiums such as The Clearing House are barred by monopoly laws from providing such templates, he says.

He thinks banks need to devise vertical, industry-specific solutions that address the ways that many companies conduct their businesses today.

Stablecoins Meets Agentic Commerce. Will Banks Be in the Room?

Buyer-supplier networks are a growing element of modern business , according to Shniderman. Simply put, these are digital marketplaces that enable buyers and suppliers to do business with each other inside a closed B2B system, often with ancillary services. (See a directory here.)

Under the GENIUS Act, nonfinancial companies can fund and issue stablecoins. Shniderman sees stablecoins as a natural add-on to buyer-supplier networks, and one that doesn’t necessarily require the involvement of a financial institution.

Initially, he believes, usage of stablecoins in these networks will be a closed-loop arrangement, in which the digital currency will only be honored within the system. The perception will be that that is a safe approach, obviating the need for bank involvement. Smart contracts and stablecoins could replace bank-operated payment mechanisms, such as cross-border wires.

Shniderman also believes that fintechs may be the first to jump into this arena, because many elements of the banking industry will resist stablecoins. While a handful of banks have publicly made a big commitment to stablecoins, many would just as soon they go away.

“The traditional ecosystem is creating friction, dragging its feet,” says Shniderman. But that may not be a luxury they’ll have for long if more commerce and business payments move to these specialized domains.

Read more:

- Three Must-Dos for Banks: Faster Payments, Stablecoins and Agentic Commerce

- Will Stablecoins Upend Banking? Watch Consumers for the Answer

- Will the GENIUS Act Revolutionize Banking and Payments? Absolutely. Here’s How

Making New Payment Flows that Customers Will Trust

As agentic commerce and payments for consumers has become a trend, trust has emerged as a key issue. In plain terms, can we give agentic AI our credit cards and not fear it running amuck?

For companies, the stakes, in monetary terms, are even bigger.

Shniderman thinks both consumers and businesses will learn to trust AI-driven commerce and payments if processes are built to include guardrails. He says we already have many purchasing decisions running on automatic pilot with fairly dumb technology — think of autopay for utility bills and subscription payments that people rapidly forget that they agreed to.

Read more: Stablecoin and AI Agents Will Reinvent Banking, According to a Crypto Pioneer

Can All Banks Play in This Game?

As exciting as these possibilities may seem, a natural question is whether this will leave some banks behind. Shniderman gives a nuanced answer.

The very largest players who are active in payments will have the resources to throw at both AI and digital currency. In fact, he says they are on a pace that is enabling them to pull further and further ahead of midsized banks.

At the other end, many community banks and credit unions are willing to cede control of much of the process so that they will be able to participate, and hold onto commercial customers’ business through third-party providers. Shniderman says there is already much precedence for this, especially among credit unions.

Banks in the middle will be challenged, Shniderman say. They typically aren’t able to invest as much into development and putting enough chips on all the appropriate spots. On the other hand, they traditionally don’t like any arrangement that means giving up control to another organization.

Ultimately he thinks these institutions will have to merge — for this and other strategic reasons — or languish in the middle.

Read this next: How U.S. Bank Is Retooling for a New Generation of Business Owners