Open Finance Is Exploding Globally. Why is the U.S. Lagging?

By Chad Davis, Senior Solutions Marketing Manager, Financial Services for F5

Simple Subscribe

Subscribe Now!

Executive Summary

- A recent analysis of 32 countries ranks economies in the adoption of open finance. Champions, including Singapore, Brazil, and the UK, all pair innovative industry initiatives with ambitious regulatory frameworks.

- Critical growth factors include the standardization of interoperable data and API protocols across markets and sectors, and the pursuit of cross-industry monetization.

- The report forecasts a market size of US$7.2 trillion market size for embedded finance by 2030, with a billion global users in open finance ecosystems and a 30% boost to banking revenue.

Open finance has evolved rapidly — from a regulation-driven initiative into a cornerstone of the world’s financial innovation landscape. According to the recently published report, “2025 Global State of Open Finance” by analyst firm Twimbit, the global open finance ecosystem includes more than 132 million active users spanning banking, insurance, pensions, and cross-sector embedded finance. The movement has had an extraordinary 330 billion transactions annually in payments alone.

Yet, the ecosystem faces significant challenges, including exploding API use, AI integration, regulatory harmonization, and cybersecurity risks.

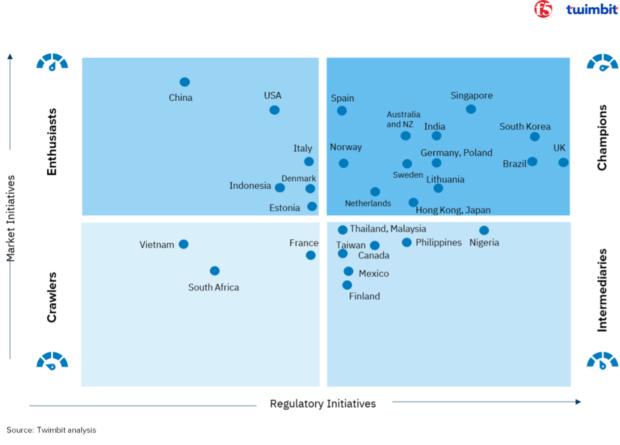

Where Countries Stand: The Global Open Finance Maturity Index

The 32 countries evaluated by Twimbit fall into four distinct categories, based on initiatives led by regulatory bodies and market-driven innovations by financial institutions and fintechs:

- Champions: Exemplary performance in both regulatory and market innovation standards, notably the United Kingdom, India, and Singapore.

- Enthusiasts: Strong market activity despite less mature regulatory frameworks, with prominent examples in the United States and China.

- Intermediaries and crawlers: Moderate to emerging maturity levels, characterized by evolving regulatory guidelines and initial market experimentation.

Why Global Innovation Is Still Heavily Influenced by Regulation

While proactive and deliberate openness is paramount for banks in their open finance strategies, regulatory frameworks still have a significant impact. Several leading nations have established clear regulatory frameworks to empower banks and fintech companies and accelerate innovation.

An example is Brazil, whose central bank continues to advance its groundbreaking open finance agenda. With 96 billion API calls monthly, their initiatives have had a substantial impact. Looking ahead, Brazil plans to introduce Banking-as-a-Service (BaaS) regulatory frameworks and further enhancements to its successful instant payment network, Pix. These steps explicitly aim to foster greater financial inclusion, transparency, and interoperability, placing Brazil at the forefront of open finance innovation worldwide.

The UK leads among “Champion” countries, advancing aggressively through the Joint Regulatory Oversight Committee’s ambitious 2025 roadmap. The UK’s proactive Data (Use and Access) Bill and upcoming long-term regulatory framework aim to supercharge a USD 13 billion smart data economy. UK’s regulatory excellence stems from decades of ecosystem-centric policymaking.

India, equally ambitious, leverages the India Stack and Account Aggregators to operationalize secure, consent-driven sharing of data. This unique model is expanding financial inclusion and driving innovation across India’s financial landscape. India’s rapid scale in open finance highlights the potential of public-private partnerships executed on a central tech backbone like India Stack.

Singapore notably adopts a more market-driven stance. The Monetary Authority of Singapore (MAS) provides strategic guidance, oversight, and vital resources such as APIX, regulatory sandboxes, and API registries, while banks and fintechs lead ecosystem development through collaborative, customer-centered solutions.

In contrast, “Enthusiasts” such as the United States and China exhibit substantial market initiatives despite regulatory frameworks that are still stabilizing. In China, market innovation driven by technology giants such as Tencent and Alibaba showcases rapid progress, though explicit open finance regulations remain limited.

Building a Stronger Banking Future Through Openness

Banks enjoy unparalleled strengths: customer trust built over decades, sophisticated risk management expertise, deep regulatory experience, and mature governance processes. These strengths uniquely position them to lead the strategic shift toward openness in financial services — not by abandoning control, but rather by deploying an evolved, strategic form of it. Rather than viewing openness as surrendering autonomy or creating vulnerability, banks should understand it as a means to extend their trusted reputation and robust risk culture across broader ecosystems.

For instance, JPMorgan’s partnership with Walmart in embedded payments through the Walmart Marketplace has enabled U.S. merchants to seamlessly manage payments and cash flow in JPMorgan’s robust financial infrastructure.

Another example is Santander UK which scaled card repayment innovation with embedded payments offered via a partnership with Token.io. The collaboration allowed customers to initiate repayments directly from over 90 UK banks without leaving the Santander mobile app. The innovation not only created a more seamless experience for the account holder, but also improved security and compliance through full alignment with Strong Customer Authentication (SCA) regulations without added login friction.

Open Finance Security Challenges Expand with Growing Ecosystems

As APIs become pivotal to open finance initiatives, ensuring robust API security is no longer optional — it’s foundational. Recent high-profile incidents, including Trello, Honda, and Optus breaches, underscore critical security failures such as inadequate authentication measures and a lack of robust API governance.

To succeed, institutions must proactively embed continuous API discovery, advanced authentication, automated deployment of API protections, and rigorous decommissioning of unused interfaces. Trust and digital resilience depend on making API security a foundational priority within open finance ecosystems, especially since they involved on so many third-party providers.

API sprawl exponentially increases with AI integrations. Cutting-edge applications in AI-driven hyper-personalization, risk scoring, lending evaluations, and fraud detection all depend on dynamic and secure API networks. This increased complexity and proliferation of APIs, intensifies the need for meticulous API management, secure interoperability, and compliance.

Dig deeper:

- EY Banking Chief: The Banking Industry Must Build New Capabilities to Survive

- What Banks Must Do While 1033 Open Banking Rules Hang in Legal Limbo

- Should You Demand Fintechs Pay for Your Data Like Chase?

The Roadmap to Open Finance Excellence

Institutions successfully embracing open finance have demonstrated several key strategic enablers that pave the way for excellence. A critical starting point is the standardization of interoperable data and API protocols across markets and sectors. This harmonization ensures seamless collaboration and integration while enabling stakeholders to work more efficiently across diverse ecosystems.

Cross-industry monetization emerges as a key avenue for profitability in 2025. When institutions like JPMorgan structure collaborative models beyond traditional banking ecosystems, they unlock new revenue streams. Effective governance of these ecosystems is equally important, requiring clearly defined roles, liabilities, and risk management frameworks to maintain stability and trust.

Finally, establishing continuous analytics and policy feedback loops allows institutions to engage in an ongoing dialogue with regulators. This iterative process helps optimize the ecosystem while ensuring compliance and fostering innovation. Each of these elements collectively contributes to open finance excellence, positioning financial institutions to thrive in a rapidly evolving landscape.

Looking Ahead: A Financial Future Defined by Openness and Security

By 2030, the economic impact of open finance will be immense: the Twimbit report forecasts a US$7.2 trillion market size for embedded finance, a billion global users in open finance ecosystems, and a 30% banking revenue boost due to open finance alone.

As financial institutions race into this future, balancing innovation with robust data protection and API security governance will define sustainable competitive advantage. Global open finance adoption must occur responsibly, with aggressive strategies for data protection and systemic API security integration. Leaders who prioritize trust, resilience, and customer-centric innovation will unlock massive market potential. Is your institution leading the open finance charge — or following in the wake of others?