More Banking Apps Offer Predictive Insights, But Many Alerts Arrive Too Late

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Three major banks have started offering predictive consumer checking account insights within their mobile apps. Using factors like past transaction patterns, scheduled and recurring transactions and expected deposits, their apps give consumers a sense of the road ahead.

- Increasingly consumers expect apps to provide such assistance, based on their experiences with nonfinancial apps.

- One pervasive problem: Account alerts that arrive so long after the fact that they’re meaningless.

A decade or so ago, pundits looked forward to the day when mobile banking would be more than a way to check balances, shoot checks and transfer funds. They talked about putting a “banker in your pocket” that would alert, advise and keep you out of trouble with a digital whisper in your ear.

That day is starting to arrive at three major institutions and will likely follow at other banks, as more players offer predictive insights and account information to mobile banking users, according to Susan Foulds, managing director of Keynova Group.

However, while that early hope is finally becoming reality, there’s a problem — poor timing.

Some institutions’ alerts, while offered, can be less-than-helpful because the banks involved deliver them too late for consumers to act upon them, according to Keynova’s latest Mobile Banker Scorecard.

How Three Major Banks Incorporate Forecasting into Their Mobile Banking Apps

Keynova’s report indicates that banks have been introducing that forecast of their spending and balances, based on past behavior and account activity. The banks’ apps base their forecasts on estimated spending, scheduled transactions, and deposit trends.

“Providing predictive insights is an exciting and consequential advancement in mobile banking that can significantly benefit customers with well-timed financial information to help them manage and improve their finances and also mitigate the risk of unnecessary fees and overdrafts,” says Foulds.

Keynova’s study cites three institutions — Bank of America, Wells Fargo and U.S. Bank — as leading this trend. The company’s analysis for this report covers 16 major U.S. banks as well as USAA.

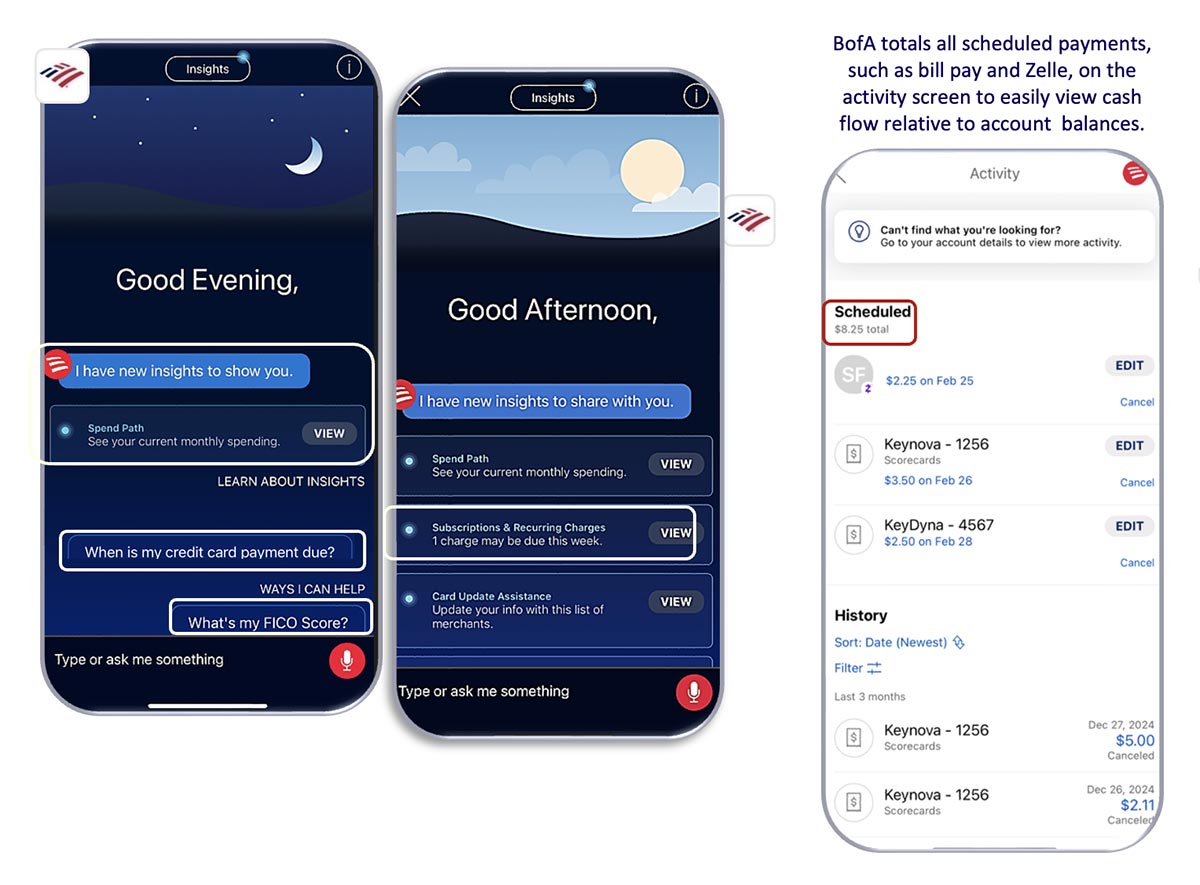

Bank of America’s Erica virtual assistant presents insights upfront after the mobile user logs in. This includes such information as payment due dates and recurring subscription charges. Insights are also presented about spending habits using the categorized spending and cash flow over the previous year.

Graphic courtesy of Keynova Group

Wells Fargo flags its forecast on the app’s pay and transfer screen (point 1 in the first screen below). Tapping on the activity forecast icon (point 2) sends the user to further detail, along with a timeline (point 3). A link (point 4) on the same screen leads to a screen (point 5) presenting any scheduled transactions, along with a chart forecasting balances in the future.

Graphic courtesy of Keynova Group

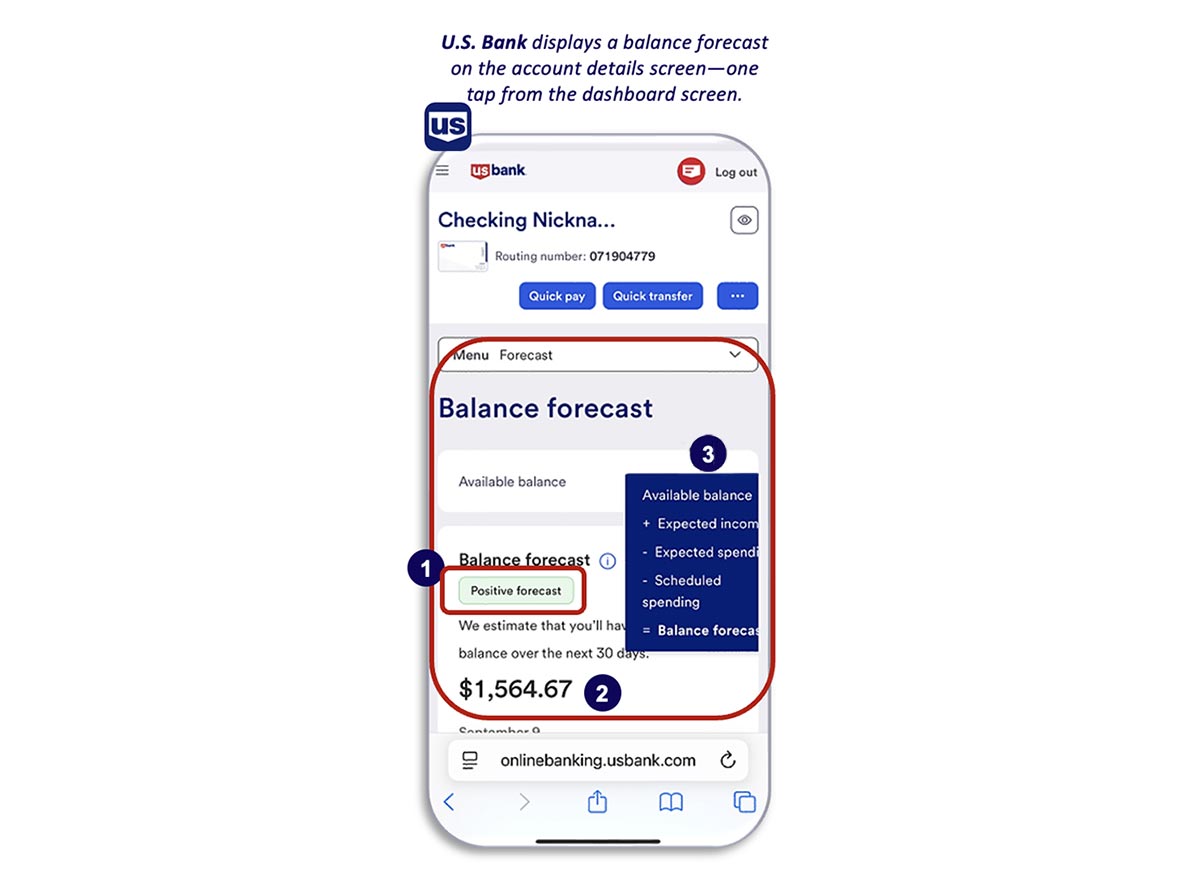

U.S. Bank’s app presents a balance forecast on the app’s account details screen. In a general sense, it gives a forecast of whether the balance over the next 30 days will be positive or negative (point 1) and then the bank’s estimate of what the running balance will be (point 2). A popup box (point 3) gives the user the data elements that went into the bank’s forecast.

Graphic courtesy of Keynova Group

Foulds believes these features can encourage consumers to consolidate more of their relationships in a single institution, because the more that’s under the umbrella, the better the forecasts can be. She says other banks that aren’t as far along as Bank of America, Wells and U.S. Bank could be doing more even with data they already have. Even simply totaling up whatever is scheduled for the next week to 14 days, and presenting the math, is a service to customers.

“But what you see in the screenshots is that these three banks have taken things a step further, where they’ve packaged it and presented it in a digestible way,” says Foulds.

Read more: How Leading Credit Card Apps Are Adding Features to Boost Spending

Spending Subset in Focus: Recurring Subscription Payments

Keynova has also found that issuers have been doing more to break out recurring charges on cards, such as ongoing subscriptions.

Subscriptions can be a significant expense, and not always apparent. Consider this: By asking consumers about their subscriptions two different ways, C&R Research, in a 2022 study, found that people underestimate their subscription bills by a factor of 2.5. The estimated average monthly subscription spend is $86, versus the actual average monthly spend of $219. This covers everything from streaming to apparel, cosmetics and food.

“Subscription services have changed the way consumers get their entertainment, apparel, food, etc. Convenient payment options through recurring monthly charges are one of the driving factors that attract many consumers to use subscription services,” according to C&R. “Oftentimes the monthly payments for these services fly under the radar, especially when consumers subscribe to more than one.”

The study also found that 42% of consumers surveyed have forgotten about subscriptions they are still being billed for, though they are no longer using the goods or services. Seven out of ten set their subscriptions on auto-pay, according to C&R. The younger the consumer, the more likely they are paying for subscriptions they aren’t using.

Subscription tracking services — some are offered by banks — were only being used by one out of ten consumers at the time the study was conducted.

Read more:

- Personalization and Accessibility: Are Banking Apps Doing Enough?

- How Three Banks Are Fighting Back Against App Consolidation

- The Silent Alarm on Mobile Banking Apps Just Went Off

Behind the Curve: Account Alerts Aren’t Always Timely

Even as account alerts have become table stakes, some banks are dropping the ball, according to Keynova’s research.

“Not all the banks covered in the Scorecard send critical low-balance alerts in real time,” says the company’s report, “and only 53% of them send real-time alerts when account balances become negative or overdraft.”

Keynova points out that alerts sent out of real-time don’t mean much — the consumer doesn’t have a chance to bring up their account balance or otherwise prevent the problem covered by the alert.

“Real-time notifications for time-sensitive events — such as external transfers or certain type of debit card activity — remain uncommon, despite consumer expectations for instant notifications,” the report says.

Another weak spot: Recurring payments that are set up for a limited period, such as a monthly mortgage payments. She advises that real-time alerts be set up so that when a payment stream like that comes to an end, and the consumers hasn’t set up a new stream, the bank’s app will automatically send warn the customer that their payment could lapse.

“Real-time alerts are fundamental to being proactive,” says Foulds. She adds that banks have to realize that consumers use many types of apps.

“Customers’ expectations are ahead of what banks are delivering,” says Foulds, “because of what they’re used to seeing in retail, travel and other types of apps. They expect to be notified proactively.”

Read more: Three Must-Have Features for Next Gen Banking Apps