How Financial Wellness Programs Drive Primacy for Banks and Credit Unions

By Nicole Volpe, Contributor at The Financial Brand

Simple Subscribe

Subscribe Now!

Many banks and credit unions have put considerable thought, and in some cases significant resources, into the role financial wellness can play in how they go to market. But for most institutions, such efforts have resulted mainly in changes to messaging and development of educational content rather than strategic shifts.

There’s nothing wrong with that; much of today’s financial wellness content is useful and informative, albeit sometimes overwhelming. Articles, videos, and explainers can be effective in building trust and engagement.

But what if a bank or credit union decided to treat accountholders’ financial wellness as an outcome to be achieved in the same way it might pursue primacy, cross-sales, or engagement? If consumers desire financial stability or a sense of financial progress — and most do, research shows — wouldn’t it be good business to make it your institution’s goal to lead them toward it?

To be sure, many fintechs have already gone down this path, with mixed degrees of success. Budgeting apps, automated savings tools, debt-management platforms, and digital advisors all have business models centered on helping customers improve their overall financial position. But what they lack is the customer and member data that banks and credit unions have — deep reservoirs rooted in trust-based relationships and reflective of the central role they’ve played in accountholders’ lives.

This article considers whether banks and credit unions can seize the wellness opportunity. What would it look like if traditional financial institutions, leveraging their data, aimed to operationalize financial wellness and situate it as a strategic objective of the customer or member relationship?

Want more insights like these? Check out MX’s content hub: Data in Action

The Changing Wellness Landscape

Definitions of financial wellness have long emphasized consumers’ desire for growth and resilience but new research is diving deeper, examining the forces that underlie their quest for wellness and what might enable them to achieve it.

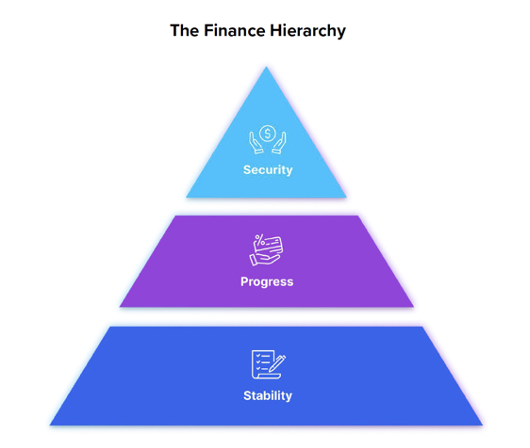

A new report by MX, a technology firm that specializes in helping financial institutions harness the value of their customer data, confirms what many of us instinctively know: consumers don’t perceive financial wellness as a zero-sum achievement. The report, based on a 2026 survey of 1,000 consumers, describes financial wellness as a hierarchy of needs that starts with stability, advances to progress and culminates in security.

Like Maslow’s hierarchy of needs, the base is about survival — the ability to cover bills and manage day-to-day obligations. Above that are goals that represent progress, like improving credit, reducing debt, and building savings. At the top is security, including retirement investing, paying down major loans, and building long-term wealth. “Our research focused on how consumers prioritize their own needs and manage financial stress, but especially on how they define progress,” said Heather Warner, Vice President, Head of Client Success & Strategy at MX. “The idea is that wellness is not one and done, but a journey.”

According to the report, many consumers are concentrated at the bottom of the pyramid: 62% consider themselves to be living paycheck to paycheck, 40% say they struggle to make ends meet, and 19% say their top financial goal is simply to cover their bills each month.

Moreover, consumers have decidedly mixed feelings about where they stand in the hierarchy: 72% say they are optimistic or very optimistic about achieving their top financial goal in 2026, yet 51% say money is their primary source of stress and 48% say looking at their financial accounts makes them anxious. Only 27% feel confident they can cover any expense, and 31% worry about covering an unexpected expense.

Managing and Measuring (Outcomes)

The report’s findings suggest ways in which banks and credit unions might do a better job of leveraging data to enable consumers’ pursuit of financial wellness, including especially by giving them a sense of control and clarity.

A key takeaway is that many consumers are highly engaged with their finances, but don’t necessarily understand their implications or have a clear perspective on how the different components of their financial lives relate to each other: 44% say they track every dollar and know exactly where it goes each month, 37% say they check individual accounts, and others rely on spreadsheets, manual processes, or budgeting tools. Meanwhile, the average consumer holds between three and four (3.6) financial accounts across different institutions but, while 76% identify a primary financial institution, only 25% keep all their accounts there. Finally, 22% say they don’t track their finances at all.

Such financial fragmentation — both emotional and structural — may help explain why 64% say they would value having a single score that reflects their overall financial health. Consumers say they want that unified score to comprehensively reflect their credit score (73%), debt owed (51%), cash flow (47%), net worth (43%), income-to-spend ratio (43%), and emergency savings (42%).

“Consumers do not necessarily need more data,” said Warner. “They need help bringing their financial lives into focus, connecting dispersed and diverse information, and translating data into actionable insights.” A bank or credit union that wants to support financial wellness might start by asking where in the customer experience they help accountholders interpret data and information, rather than merely presenting it.

Even still, while a unified financial health score has broad appeal, things get complicated when it comes to the role the score would play. More than 30% of respondents straightforwardly believe such a score would give them a clearer picture of their financial health, but 28% say they would want even more information to make their finances easier to understand and 14% say they want visibility into actions they can take to improve their financial health.

Just as important, the report shows the limits of a purely evaluative approach. Some respondents do not want a score because they worry theirs would be low, or because they don’t want yet another number to manage, or don’t think it would help them improve. “A financial wellness score might be influenced by a credit score but it’s purpose is much different,” Warner said. “It’s important for institutions to provide guidance without judgment.”

Consumers want tools that surface what matters, draw on core financial indicators, and help them make the journey from stability to security. For banks and credit unions, that points to a more specific role in enabling wellness: not merely offering products or publishing educational content, but helping accountholders make practical sense of their financial position in ways they can act on. It would enable them to gamify their progress, in ways that are highly personalized.

Managing and Measuring (Outcomes)

Getting Started

For banks and credit unions looking to center financial wellness within their go-to-market strategy, it helps to establish a set of first principles that align with their mission and market. Strategists can start by taking the following steps:

- Define financial wellness for your market and accountholder base. Not every institution should use the same definition. A locally-oriented community bank, a small financial institution with strong digital reach, and a credit union with a mission orientation might each frame the outcome somewhat differently.

- Identify what progress looks like. Translate wellness into a manageable set of metrics the institution can observe and influence — and map them across the stability / progress / security pyramid in the same way you might map them within a sales or marketing funnel.

- Clarify the relationship between wellness and primacy. Rather than treat these as separate ideas, explore whether helping accountholders make financial progress is one path to deeper trust and higher engagement, and increasing your institution’s likelihood of achieving primary-institution status.

- Tie the effort back to your mission and operating model. For some institutions, centering wellness will connect naturally to mission. For others, it may be more useful to operationalize this objective as a series of “nudges” within a more traditional journey, offering customers and members ways to track progress and being present with answers at key moments in their financial lives.

- Take a page from the robo-adviser playbook. These fintechs use algorithms to provide advisory services online, often with limited human interaction and at lower cost than traditional providers of investment management and advice services. How can your institution better leverage data to guide customers and members to financial wellness?