As the Wealth Gap Widens, Banks Have to Pick Between Two Distinct Customer Sets

By David Evans, Chief Content Officer at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

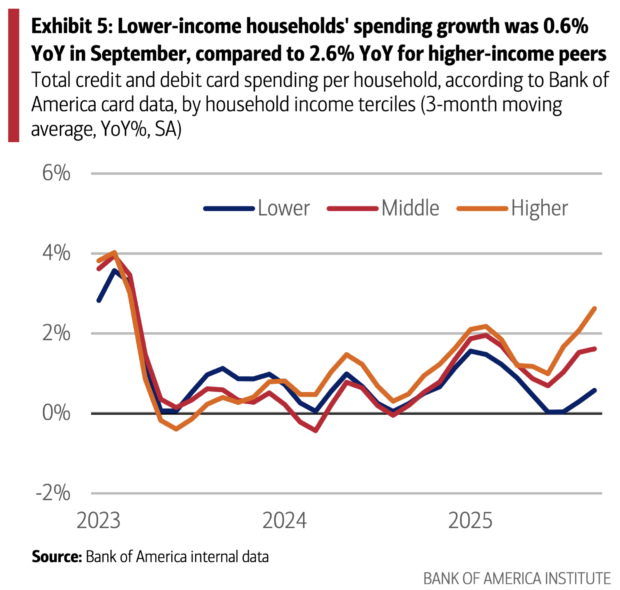

- According to Bank of America, decent 2% YoY growth in total household spending in September masked a widening chasm between lower-income households and higher-income consumers.

- Higher-income households benefit from a wealth effect driven by equity markets, while lower-income households, particularly Millennials and Gen X, face cooling wage growth and lack the assets to maintain spending momentum.

- For retail banks, products and marketing must address fundamentally different financial realities: expanded credit access and financial education for struggling households versus wealth management and premium services for the affluent.

September’s consumer spending data looks reassuring at first glance — 2.0% year-over-year growth, four consecutive months of positive momentum, the strongest performance since December 2024.

But strip away the averages and a starkly different picture emerges, according to new analysis by Bank of America: American consumers aren’t experiencing one economy, they’re living in parallel financial universes increasingly determined by asset ownership rather than employment alone. The 2.6% spending growth among higher-income households contrasts sharply with the anemic 0.6% managed by their lower-income counterparts, creating a divergence that retail banks can no longer afford to ignore.

This bifurcation matters because it’s not cyclical, it’s structural. Lower-income households, particularly Millennials and Gen X, have watched their wage growth cool throughout 2025, with September’s 1.4% year-over-year gain representing less than one-third the rate higher-income households enjoy.

More critically, they lack the asset buffer to smooth consumption when income growth slows. Higher-income households, by contrast, increasingly derive spending power from wealth effects that compound independently of their paychecks. When the top 20% of earners hold an average $1.6 million in equities while the next quintile holds just $130,000, a 15% stock market gain doesn’t lift all boats — it creates tidal waves for some while leaving others treading water.

For retail banking executives, this divergence demands radical rethinking of product strategy.

The traditional middle-class customer facing temporary liquidity constraints looks fundamentally different from today’s lower-income household struggling with structural wage stagnation and zero wealth cushion.

Similarly, affluent customers with seven-figure investment portfolios require sophisticated wealth management and premium services that weren’t part of the retail banking playbook a generation ago. Marketing campaigns promoting one-size-fits-all checking accounts or generic savings incentives will increasingly miss the mark when customer financial realities have never been more disparate.

When Stock Portfolios Matter More Than Paychecks

The most significant development in September’s data isn’t what happened. It’s why it happened. Higher-income spending growth is increasingly decoupled from wage growth alone, driven instead by wealth effects that magnify market gains into consumption increases. Bank of America’s analysis reveals a striking correlation: the difference in discretionary spending growth between the top 5% of households and middle-income peers has closely tracked S&P 500 performance since 2020. When equity markets rise, affluent consumer spending accelerates not just because people feel wealthier, but because they are wealthier by amounts that often exceed their annual salary increases.

Example: A household in the top 20% holding $1.6 million in equities and mutual funds experienced roughly $208,000 in portfolio gains from the 15% year-over-year market appreciation through Q3 2025. Even if only a small fraction of those gains translates to increased spending through the wealth effect — typically estimated at 3-5 cents per dollar of wealth increase — that’s $6,000 to $10,000 in additional annual consumption. For many high earners, that portfolio gain exceeds their nominal wage increase, making asset appreciation a more important driver of spending capacity than employment income.

This wealth concentration has profound implications for retail banking strategy. Traditional deposit acquisition focused on capturing direct deposits and building transactional relationships. But when your affluent customers derive significant spending power from investment portfolios, the real relationship battle occurs in wealth management, trust services, and investment advisory. Banks that treat high-net-worth retail customers primarily as checking account holders rather than investors requiring comprehensive financial planning will lose wallet share to competitors who recognize the new reality. The data suggests discretionary spending among the top 5% moves with the S&P 500 — meaning the institution managing their investment portfolio increasingly influences their spending patterns and product needs.

Housing wealth plays a supporting but more limited role. Home equity is less concentrated than financial assets, with the top 20% holding average equity of $770,000 compared to $220,000 for the next quintile — substantial but not the 10-times differential seen in stock holdings. More importantly, house price appreciation has been modest recently, limiting current wealth effects. The more promising channel is home equity lines of credit, where utilization has risen modestly as the Federal Reserve cuts rates.

However, even significant HELOC growth will have muted macroeconomic impact given total balances represent just 2.0% of consumer spending. For banks, this suggests opportunity in targeted HELOC marketing to homeowners with low mortgage rates who won’t refinance but may tap equity for large purchases or debt consolidation as borrowing costs decline.

Dig deeper:

- The Wealth Transfer Problem No One Talks About — And the Community Banks Solving It

- Don’t Wait for the ‘Great Wealth Transfer’ – Help Younger Customers Reach Goals Now

- The Great Wealth Transfer: How Banks Win the Next Generation of Business Owners

The Lower-Income Squeeze Intensifies, and It’s Not Temporary

While affluent households ride equity market gains to spending growth, lower-income consumers face a different and deteriorating reality according to the BofA report. September brought a small uptick in lower-income wage growth to 1.4% year-over-year, but context reveals this as false comfort. That rate represents less than half the 2.5% average since January 2024 and a fraction of the 4.0% growth higher-income households enjoy. More concerning, lower-income wage deceleration has persisted throughout 2025 across most generations, with Millennials and Gen X particularly affected. These aren’t workers between jobs or temporarily sidelined — they’re employed households watching their real purchasing power erode as nominal wage gains fail to keep pace with inflation and fall well short of the income growth occurring higher up the distribution.

This matters because lower-income households lack the asset cushion that buffers consumption for their wealthier peers. When wages slow, spending must slow proportionally — there’s no investment portfolio generating gains to offset income weakness, no substantial home equity to tap through credit lines, no diversified wealth enabling consumption smoothing. Bank of America’s data shows spending among lower-income Gen Z households holding up better than other cohorts, likely because they’re earlier in careers with stronger wage trajectories. But Millennials and Gen X in the lowest income tercile face a particularly difficult situation: they’re in prime earning and family formation years but experiencing cooling wage growth without accumulated assets to bridge the gap.

For retail banks, this dynamic creates both challenge and opportunity. The challenge is that traditional credit products may not address the fundamental issue — structural wage weakness rather than temporary cash flow mismatches. Offering a credit card to a household whose income isn’t keeping pace with expenses doesn’t solve the underlying problem and may actually accelerate financial distress. The opportunity lies in products and services that help lower-income households build assets and improve financial stability: matched savings programs, automated savings tools, financial education focused on building emergency funds, and products that reward positive financial behaviors rather than simply extending credit. Banks that help these customers build even modest asset buffers — $500 in savings can prevent costly overdrafts and emergency debt — create loyalty while serving genuine financial needs.

Marketing to lower-income households also demands fundamental recalibration. Promotions emphasizing luxury travel rewards or premium account features miss the mark for consumers struggling to maintain spending growth. Instead, messaging should focus on practical value: no-fee checking, overdraft protection, savings automation, and financial education resources.

Community engagement and branch presence also remain critical for this demographic, as does mobile banking capability that enables real-time balance monitoring and spending management. The institutions that combine practical products with empathetic marketing and genuine financial education support will earn relationships with customers who, while facing current headwinds, represent tomorrow’s middle class.

The Bottom Line

September’s consumer spending data confirms what many suspected but couldn’t quantify: America increasingly has two consumer economies, one powered by wage growth and another by wealth effects.

For retail banking executives, this bifurcation demands strategic clarity about which customers you’re serving and how their financial realities differ. Products, pricing, marketing, and service delivery that ignore these diverging circumstances will underperform. The institutions that succeed will be those that acknowledge different customers need fundamentally different solutions — from asset-building tools and financial education for struggling households to sophisticated wealth management for portfolios driving discretionary spending.