5 Ways to Solve the Financial Health Disconnect for Consumers

By Katie Casaday, Content Writer at MX

Simple Subscribe

Subscribe Now!

There is a disconnect between consumers’ expectations and the reality of financial health. As far as expectations go, the majority of consumers are filled with optimism. In fact, 72% of consumers say they are optimistic or very optimistic about achieving their top financial goal in 2026 — according to MX’s latest consumer research diving into financial health.

On the other hand, money remains a significant source of stress for many consumers. Fifty-one percent of consumers say that money is their main source of stress. And, money management is very hands off for some — with 17% of consumers reporting they avoid looking at their finances whenever possible.

Additionally, in 2025, the Financial Health Network found that only 31% of households across the U.S. were financially healthy. Today, banks and credit unions generally offer financial wellness tools like budgeting apps as part of their digital offering. But, the data is clear. The current state of financial tools and resources is not sufficient to completely transform consumers’ financial lives.

The disparity between optimism and stress solidifies a need for better tools and resources to promote financial health. Financial institutions are in a unique position to turn consumers’ current state of optimism into reality by solving for the disconnect.

Want more insights like these? Check out MX’s content hub: Data in Action

Need to Know:

- There is a disconnect between financial health expectations and reality. 72% of consumers say they are optimistic or very optimistic about achieving their top financial goal in 2026, while 51% of consumers say that money is their main source of stress.

- Prioritize leading with mobile and digital banking experiences to promote the innovations — personalization, AI, financial health scores — that will directly drive financial health.

- Investing in financial health pays off. The Financial Health Network found that customers who believe their financial institution cares about their financial health are 5x more likely to be interested in purchasing additional products and services.

Here are 5 ways that financial institutions can provide direct aid and solve the financial health disconnect for consumers:

Lead with Mobile and Digital Experiences

In today’s banking landscape, mobile banking is one of the most important tools that financial providers must leverage to meet consumers’ financial needs. But, it’s time for financial providers to rethink how they are leveraging the mobile experience — and lead with it.

While mobile banking experiences are not new, their growing adoption offers financial providers an opportunity to leverage mobile strategies and promote financial health on a deeper level. Fifty-two percent of consumers say they check their most used banking or finance app every single day and 23% check their most used finance app multiple times a day — according to MX research. Because most consumers access their finances on mobile applications, prioritizing these strategies can have a quick and lasting impact.

As financial institutions lead with mobile banking strategies, they will be able to unlock new avenues that will drive financial health for consumers. Through mobile, financial institutions can do more than simply put new features in consumers’ hands. They can determine the functionality that will help consumers manage their financial lives better with the ability to connect accounts, get insights into their financial habits, switch their direct deposit, and more.

When consumers have access to next-level digital banking tools, they can make informed spending decisions, prioritize their savings goals, and see their financial life as a whole.

Provide Actionable, Personalized Financial Education

Effective digital banking is driven by personalization, which is an expectation for the majority of consumers. MX research found that 61% of consumers expect their financial provider to know them.

And, these personalized financial experiences have a clear impact on consumers’ financial health — especially among the younger generations. Sixty percent of Gen Z said they have noticed a positive impact on their financial habits or goals due to personalized digital banking features — according to The Harris Poll, commissioned by Q2.

Finances are unique to each individual. This means that there is no one-size-fits-all solution for financial health. Financial institutions should leverage consumer data to offer actionable and personalized financial education. These actionable and personalized financial insights can prompt consumers to transfer money into a savings account, apply for a loan with a lower interest rate, or ensure that an account has enough money for an upcoming bill.

Financial providers can make consumers’ financial goals a reality by becoming trusted financial partners that truly know their customers.

Track the Metrics that Matter

Making a positive impact on consumers’ financial health is contingent on recognizing the metric that they use to define their financial health. For example, one clear indicator of an individual’s financial health is their ability to cover an unexpected expense. And, MX’s research found that 31% of consumers are worried about their ability to cover an unexpected expense. This statistic highlights the fact that consumers need help. That help begins when financial providers focus on the metrics that truly indicate consumers’ financial health.

When it comes to metrics, financial providers and consumers have different priorities. Financial providers often lean too hard into metrics like product usage as a clear sign of their impact. While product usage is important, that number alone doesn’t directly translate to financial success for consumers.

Financial providers should monitor product use — or engagement — and how it ties into key metrics consumers use to define their financial health. Instead of seeing deposits, account openings, and loans, financial providers should flip the script and view them from the customers’ point of view. Do these impact savings goals? Do they grow emergency funds? Do they contribute to positive cash flow? Doing so can help financial providers paint the picture of whether or not their products drive outcomes for consumers. And, it will inform them if they need to switch gears.

For example, MX conducted research using aggregated and anonymized data for those that had high engagement and interaction with its digital banking tools.

Among highly engaged consumers, MX found:

- 1.8x greater change in average for checking and savings account balances

- 3.9x greater increase in loan accounts

- $1,600 balance increase per user during the measured period

- 21.5% in this group had more accounts overall

Bottom line, engagement matters. But, only as long as you can measure how that engagement is leading consumers toward desirable financial outcomes like higher deposits, more loans, and more account openings. That’s the growth that matters — both for consumers and financial institutions.

Invest in AI that Benefits Consumers

Artificial intelligence (AI) tops the list for necessary innovations across every industry — but especially within financial services. The first wave of AI brought about simplified processes and a reduction in internal busywork for financial institutions. While the functionality that AI can provide to these institutions is nearly limitless, those benefits are not realizing AI’s full potential for consumers.

Isabelle Zdatny, head of thought leadership at Qualtrics XM Institute said, “Too many companies are deploying AI to cut costs, not solve problems, and customers can tell the difference.” Through AI’s limitless potential, financial providers should zero in on how AI can directly promote financial health.

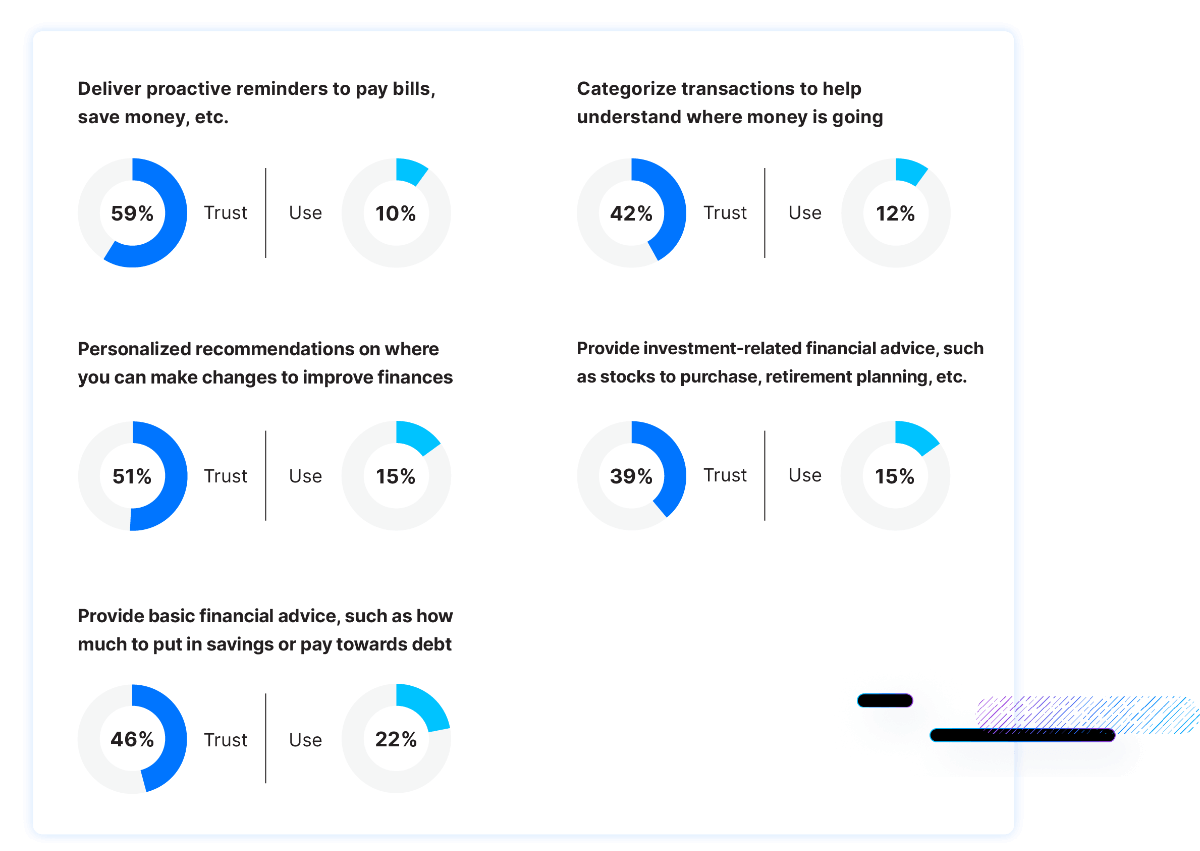

MX research found that while most consumers trust AI to assist with certain financial tasks, actual AI adoption for these same tasks is much lower.

Financial providers should invest in AI solutions that do more than cut costs on the backend. They should prioritize the AI solutions that provide value to consumers in their financial lives.

Provide a Financial Health Score

Offering a budgeting tool, especially one that is hard to use, is not enough to grow consumers’ financial health. Most consumers (64%) say they would want to know their score telling them how financially healthy they are if given the option.

And, this means going beyond credit scores. The Financial Health Network’s FinHealth score is one solution that has established metrics for individuals and businesses to assess their financial health beyond the basics of credit scores.

Many financial institutions already have access to data that would inform a financial health score, but have not taken steps to make it visible for consumers. Data tells financial providers about consumers’ income, loan balances, connected accounts, and more. But, that data’s effectiveness is limited when held back from the consumer. All of these things can have a powerful contribution to an informed financial health score.

Financial Health Helps Financial Institutions Win

Solving the disconnect between consumers’ financial expectations and reality benefits consumers while also helping financial institutions to grow. Customers who believe their financial institution cares about their financial health were significantly more likely to strengthen their relationship with that institution. The Financial Health Network found these consumers were:

- 3x more likely to be very satisfied with their primary financial institution

- 3x more likely to recommend their primary institution

- 5x more likely to be interested in additional products and services

When consumers are financially healthy, financial institutions win.