In the future, excellent CX will define winners and losers in financial services. As consumer expectations rise across all delivery channels and with every demographic segment, the ability to deliver against these expectations will have a direct impact on an organization’s revenue and profitability.

When customers enjoy a better experience, it is more likely they will stay with, buy more from, and recommend an organization to others. However, the components of a great experience are not static. In fact, our research shows that customer expectations around what they want from their bank or credit union has changed more in the past 18 months than at any time in the past.

The biggest inhibitors to delivering an exceptional experience mostly reside in the foundation of an organization – a foundation that is steeped in tradition and a delivery network that is comprised of physical structures. To deliver a positive experience for today’s customer requires a commitment to the following:

- Modern IT infrastructure

- Data and applied analytics

- Partnership with fintech and third-party providers

- Culture of innovation

- Seamless omnichannel delivery

- Digital-ready workforce

Beyond the six requirements above, there must be leadership that is willing to embrace change in legacy business models, is open to experimentation, and is skillful at bringing an alignment between all key constituents within and outside the organization.

Read More: The 6-Step Survival Guide to Digital Banking Transformation

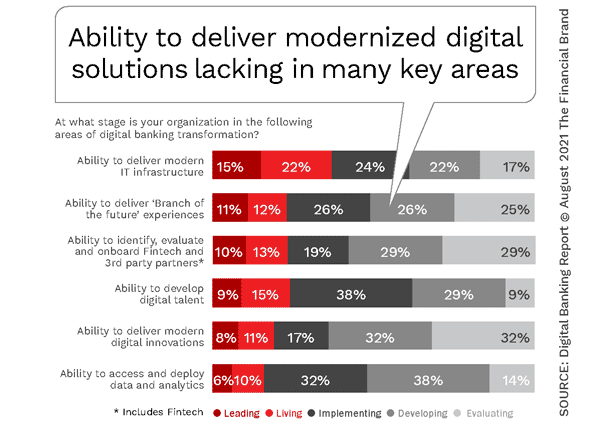

Challenges in Delivering Modernized Digital Solutions

To assess the ability to deliver modernized digital solutions, the Digital Banking Report surveyed financial institutions globally to determine how future-ready organizations were. More than 200 executives from organizations of all sizes provided a self-assessment of their organization across a spectrum of categories. The levels of maturity were:

- Leading: These standards are central to our organization’s strategy, and these capabilities are fully and consistently implemented and optimized across our organization.

- Living: The value of these practices is recognized and the capabilities are widely and consistently deployed across our organization.

- Implementing: We understand the value of modern approaches. However, such capabilities are implemented in just a few parts of our organization.

- Developing: We recognize the value of these best-practice standards — but investment, experimentation and development are in the early stages and we are working on a holistic strategy.

- Evaluating: We are at a preliminary stage. Our organization does not plan to invest in these areas in the next three years.

Primary findings include:

- The most success by organizations of all sizes has been with back-office IT infrastructure (83% of organizations are doing something, with 37% “leading” or “living”).

- While fewer organizations see themselves in the top levels of implementation, there is a greater deal of attention being paid to developing internal skill sets and data/analytics (lowest % of organizations in “evaluation” phase).

- Data/analytics maturity is the least developed of categories, potentially impacting all other areas of digital banking transformation.

- The ability to deliver modern digital innovations is not only low, but one-third of organizations are only evaluating the development of an innovation culture.

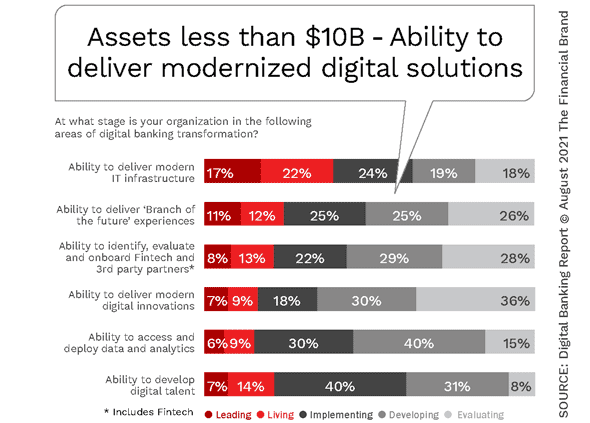

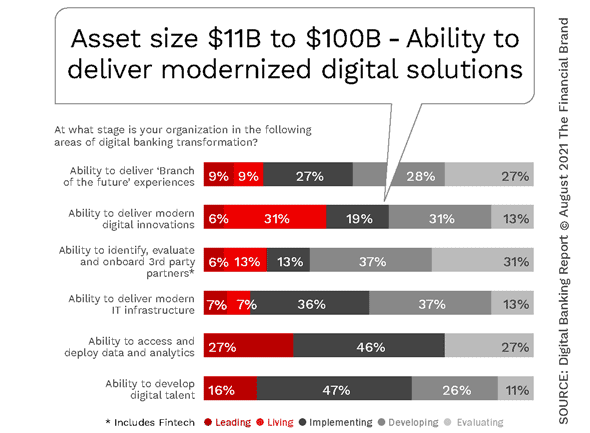

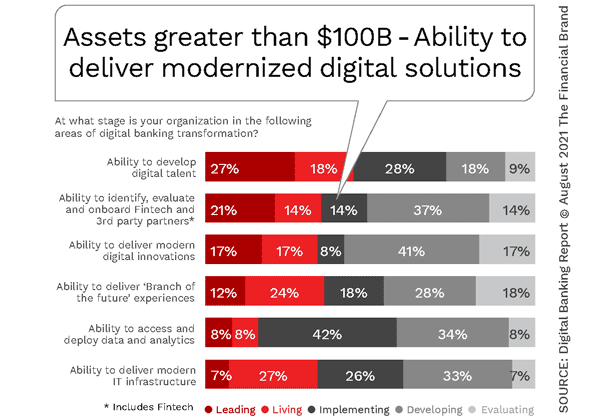

Future-Readiness Varies by Asset Size

When we analyzed the research results by asset size, there were significant differences between the big, small and mid-asset organizations. As we have found in other research regarding digital banking transformation, in several of the categories, the least-prepared institutions were the mid-asset category ($11B – $100B).

Mid-Asset Banks Challenged:

While smaller and the largest banks and credit unions are making major digital banking transformation progress, mid-asset firms continue to lag the industry in future-readiness.

The reason for this gap in performance is thought to be caused by a more established legacy management team at mid-asset firms that may be less prone to embrace change, the cost of changes required, and the scope of the challenges within a modest-sized organization. Alternatively, many smaller organizations and credit unions have made significant strides in several areas, while the largest banks have the resources to transform their organizations at scale.

Primary findings include:

- The smallest organizations (under $10B in assets) are further ahead of the overall industry in development of IT infrastructure, but are behind in building an innovation culture.

- Mid-asset organizations ($11B to $100B) are far behind the industry as a whole with the development of a modern IT infrastructure, but are ahead of the industry in creating an innovation culture and data/analytics maturity.

- The largest organizations (over $100B) are investing in skill set development and working with fintech and third-party providers, but lag the industry as a whole with the development of a modern IT infrastructure.

- The largest organizations are ahead of the industry with data and analytics.

Updating IT Infrastructure is the Foundation for Success

When organizations were asked to self-assess their ability to deliver modern IT infrastructure, while the number considering themselves to be “leaders” or “living” were the highest of any category surveyed, the numbers were still very modest, with only 15% believing they were leaders and 22% considering themselves in the “living” stage. What was concerning was that almost four in ten organizations were only “evaluating” or “developing” modern IT solutions.

When we broke out the results by size of organization, we found that the smallest institutions ($10B and under) mirrored the industry average across the board, with 39% being in the top two categories and 37% being in the two least developed rankings.

For mid-sized organizations ($11B – $100B), the level of IT modernization maturity was much lower than the industry as a whole, with only 14% of organizations in the top two levels (“leading” and “living”). Half of the organizations of this size were in the “evaluating” and “developing” maturity levels. This slowness to implement modern infrastructure is directly tied to the cost of deployment for organizations of this size.

What was surprising was that the largest financial institutions also lagged the overall industry in their modernization of IT infrastructure. While not as far behind as the mid-asset organizations, this category had the lowest maturity results for the largest firms (7% considered themselves “leading,” with 27% saying they were “living” in modernizing IT infrastructure). One-third of firms larger than $100B said they were in the “developing” stage.

The level of lag for the largest financial institutions can be explained by the potential assessment as to the level of change that most larger financial organizations believe is required to stay on par with nontraditional financial firms and tech organizations encroaching on the delivery of financial services.

Digital Readiness to Support Digital Transformation

Digital banking transformation is more than just deploying digital technologies or building a new digital application. The goal of digital transformation is about optimizing business or organizational effectiveness within and outside the organization. Transformation occurs when overall business strategies are changed for the future. The lack of digital readiness can slow digital transformation and negatively impact growth opportunities.

An important component of digital banking readiness is preparing the culture for what is needed to succeed in the future, and having the leadership required to constructively cause, and respond to, disruption.