Despite making significant progress in digital banking transformation since the pandemic, the relative confidence of most banks and credit unions in their future readiness has decreased over the past year, according to a study by Sopra Steria. The firm says this can be attributed to several marketplace changes:

- The pace of technological change is accelerating. Many financial institutions feel overwhelmed in their ability to keep pace with new technologies, such as cloud computing, blockchain, artificial intelligence (AI) and open banking. In many instances, the ability to fully leverage these technologies to improve legacy operations and customer experiences is done in a piecemeal manner as opposed to being integrated seamlessly.

- The competitive landscape continues to evolve. Despite lower levels of funding, new fintech firms continue to enter the market, moving faster and with more agility than established financial institutions. At the same time, big tech firms are increasingly offering banking services embedded within non-banking offerings.

- Regulations are becoming increasingly complex. Financial institutions must comply with a growing number of regulations, covering privacy, open banking, transparency and ESG guidelines. Trade organizations continue to fight against differences in compliance variances where competitors are not subject to the same regulations.

- Economic uncertainty increasing. Banks are facing headwinds from rising interest rates and global economic uncertainty. This economic uncertainty often impacts the industry’s willingness to invest in future-ready solutions.

Read More:

- Digital Banking Transformation Trends for 2023

- Top Retail Banking Trends and Priorities for 2023

- Top Retail Banking Innovation Trends for 2023

- 5 Payment Trends to Watch in 2023

Future-Proofing Existing Business Models

One of the reasons for the banking industry’s struggle to digitally transform is the lack of a clear digital strategy. Many financial institutions are still trying to move beyond traditional processes and products, figuring out how to best use digital technologies to improve operations and customer experiences. Without a clear strategy, banks and credit unions will be challenged to prioritize their digital initiatives and measure their key performance indicators (KPIs). To move forward, banking executives must be willing to take measured risks to transform their business outside existing comfort zones.

At a time of economic uncertainty, banks and credit unions have to split their attention between innovating to counter the downturn and increasing operational resilience. In many cases, this needs to occur with the headwinds of cutting back on budgets and head counts, the increasing frequency of disruptive events, the emergence of new technologies, and the increasing of customer expectations.

Digital banking innovation of greatest interest includes the use of advanced technologies such as artificial intelligence (AI), cloud technology and the blockchain to enhance customer experience, improve risk management, and increase operational efficiency. Banks that are able to effectively leverage these technologies will be best positioned to meet the demands of a digital-first consumer and stay ahead of the curve in an increasingly competitive marketplace.

From the perspective of resilience, financial institutions must be able to quickly and effectively respond to and recover from unexpected disruptions caused by unforeseen events, such as cyber attacks, economic upheaval, and regulatory changes. This is crucial for maintaining the trust and confidence of customers.

Finally, banks should be prioritizing the creation of new revenue streams according to the Sopra Steria research, such as by improving environmental sustainability and supporting the financial well-being of customers. In many cases, these initiatives are being driven by cross-functional, agile collaborations with third-party solution providers and fintech firms that can improve the speed and scale of digital transformation.

Read More: Open Banking Fintech Partnerships Required For Better CX

Meeting the Changing Needs of Consumers

“Hyperconnected customers demanding personalized services are calling for an acceleration of their banks’ [digital] transformation – toward more security and advice, as well as digital and environmentally responsible products and services,” according to the firm’s 2022 Digital Banking Experience report. The consumer view suggests a widening gap between the priorities set by banks and the expectations of customers, which are changing at an increasingly rapid pace.

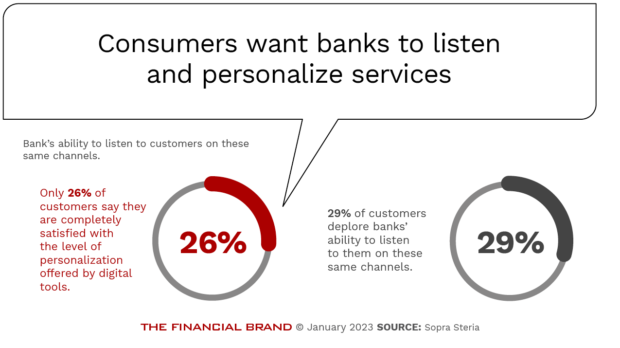

Despite the ease of communicating with banks across digital channels, consumers are becoming increasingly frustrated with the lack of listening and personalization by financial institutions. In fact, only 26% of customers say they are completely satisfied with the level of personalization offered by digital tools, and 29% deplore banks’ ability to listen to them on these same channels. This is why 46% of customers surveyed say they would open an account with a non-bank player.

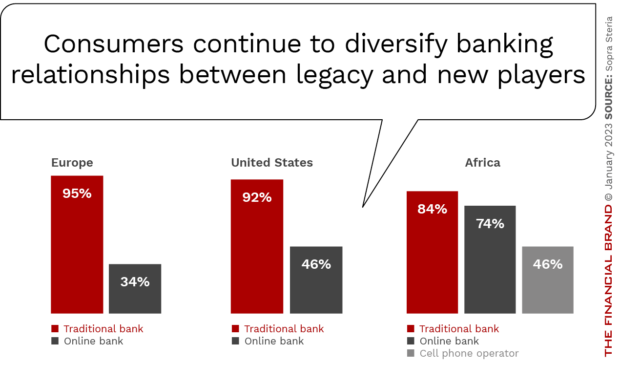

More than ever, today’s banking customer has diversified their banking relationship across multiple traditional and non-traditional solution providers. As a result, they are less likely to interact with their legacy banking institution. Sopra Steria’s research indicates mobile applications and websites from legacy and non-traditional banks are becoming the primary channels of exchange for more than half of consumers globally.

The challenge is that fintech firms and even tech companies offer mobile-first services that make it easier for consumers to manage their finances. Additionally, these companies often offer specialized services such as peer-to-peer payments, micro-investing, budgeting tools, as well as segment-specific offerings that are often not available through traditional banks or credit unions.

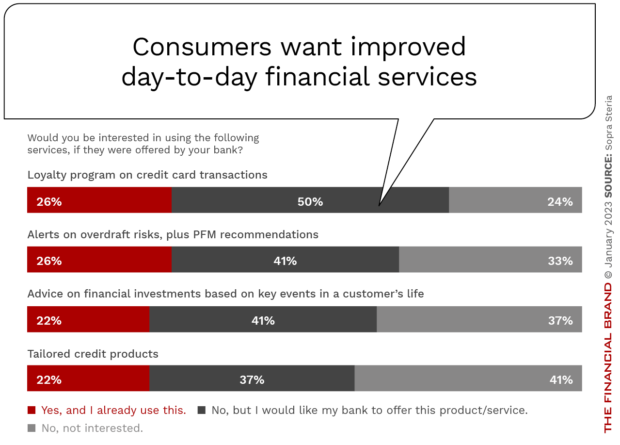

Interestingly, while banks and credit unions are trying to ramp up the development of high-tech capabilities, such as blockchain and AI, most consumers are more interested in less-advanced banking products and services, preferring improvements in basic banking. “While banks should continue to keep an eye on forward-thinking technologies, they can still benefit from fine-tuning existing digital banking offerings,” states the research.

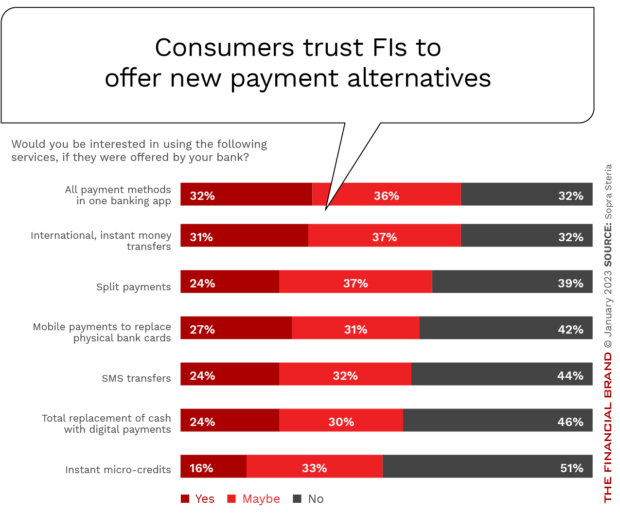

Consumers also mentioned a strong desire for increased investment in advanced payment solutions such as real-time payments, cross-border capabilities, modernization of the payment infrastructure and BNPL. This demand is driven by several factors, including the growing use of mobile devices and digital platforms for financial transactions, the increasing adoption of e-commerce and online marketplaces, and the desire for faster, more secure and more convenient payment methods.

The Importance of Collaborative Business Models

Digital banking transformation has become increasingly complex as the marketplace changes faster. To keep pace with the change occurring, progressive financial institutions are collaborating with fintech firms and third-party solution providers to assist with the integration of advanced technologies, the development of new products and services, and the adoption of new business models.

These collaborations provide access to specialized expertise, technology and new market opportunities, with supporting success stories that help deliver solutions faster and with lower risk. For instance, a bank or credit union may partner with a fintech company that specializes in the use of data and artificial intelligence to develop new acquisition, onboarding, relationship growth and retention strategies that enhance the customer experience.

Partnerships and collaborations can also provide access to new market opportunities through embedded banking, banking as a service (BaaS), open banking or other expansion strategies. Even with these expansion opportunities, banks should use their legacy advantage of trust to improve on hyper-personalized products and services. One solution set that is beginning to get a lot of traction are tools that help with financial wellbeing.

“By increasing investment in data interoperability, as well as around key consumer-facing banking initiatives, today’s bank is preparing to maintain contact with end customers, while also positioning itself as support for non-banks entering the financial services ecosystem,” states Sopra Business Software. “From the bank’s point of view, it will ideally serve both sides.”