This $6.9B Community Bank Competes with Chase — By Running a $1.3B Digital Brand on the Side

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

The Greater Boston area that Cambridge Savings Bank calls home enjoys a strong economy, many deep pockets and a population projected to continue to grow after a 9%+ growth spurt in the 2010s. Cambridge Savings has been in the market for almost two centuries, but its market is getting crowded as other local institutions and megabanks like JPMorgan Chase build new branches there. Meanwhile, digital players like Chime and other fintechs keep going after checking accounts and more, remotely.

Key point: “You used to be able to just worry about the five banks around you, but now you have to worry about competition from across the entire nation, especially since Covid,” says Ryan Bailey, president and CEO at the $6.9 billion-assets bank. “We’ve got to keep an eye on everybody.”

Bailey came to Cambridge Savings in early 2024 after a long career in management positions at TD Bank, Bank of the West, JPMorgan Chase, Bank of America and USAA. He sees its independent future as hanging onto the best of its traditional historical ways of doing business, but continuing to marry that to digital channels, to bring customers an irresistible combo.

Key strategy: “What I’m going to do is make sure that if they’re sitting on their couch at home they can bank just as easily with me, or even better, than the largest institutions in the country,” says Bailey.

Nor is Cambridge averse to looking further afield itself.

While its 19 branches are all in the Greater Boston footprint, the bank launched an online brand focused in 2021 on deposit generation nationwide. Today its Ivy Bank, drawing on money from 49 other states, accounts for $1.3 billion in deposits currently — about 23% of the total deposits of Cambridge Savings.

Need to Know:

- Best of both worlds. “We’re a nearly 200-year-old community bank and we’re not going to change our tradition,” says Bailey. “What we’re going to do is modernize our bank to make sure we’re around and relevant for our customers 200 years from now.”

- CX challenge goes on and on. “Customer experience is a marathon, not a sprint. There are going to be areas that we’re continuing to evolve. There’s not an endpoint, ever,” Bailey adds.

- Expansion possibilities. Cambridge Savings unveiled a new branch in 2025 and remains open to more opportunities, though none are planned for 2026. Given the friendlier atmosphere for acquisitions among federal regulators, Bailey says the bank has the capital and appetite to do a deal if a good strategic fit becomes available.

Cambridge Savings does plenty of digital marketing, but President and CEO Ryan Bailey says traditional media also helps put across community bank messaging. The bank also continues to rely on direct mail, a proven channel.

Ivy Bank Pushes Deeper Roots Among Younger Customers

When Cambridge launched digital-only Ivy Bank, it was a pioneer among community banks.

Bailey sees that experience as an advantage.

“We’ve had some practice, if you will, and that’s really helped us to figure out what works and what doesn’t, and that’s led to some things that our competition doesn’t do,” he says.

Key differentiation: Online bank with a human voice. “With many digital banks, it’s really hard to get a live person if you need help,” says Bailey. “Often you go straight to a chatbot. That’s not our strategy. We want to be here for you, especially in those moments when you most need us to be there.”

So Ivy Bank features live agents who are available six days a week, with limited hours on Saturdays.

Frequently this saves prospects and customers from the interactive voice response “circle of death,” says Bailey.

Ivy Bank was paying 3.85% APY on high-yield savings in March 2026, competitive with many of the top-rated high-yield accounts offered on Bankrate.com.

Key challenge: Garnering more young customers. “The younger generation wants everything now and to get it with simple clicks,” says Bailey. “So, we made it easier to bank with us. We tried to make our app much more attractive to that young population.”

The streamlining paid off. In Ivy’s early years Millennials and Gen Z comprised only about 22% of the digital brand’s customer base. At present these customers have almost doubled, to more than 42% of the base. In terms of new deposit generation, over 53% of new customers are Millennials or Gen Z.

Read more: What Does It Take to Attract Deposits with a Digital-Only Bank Brand?

Don’t Reinvent the Wheel. Partner with Fintech Wheel Makers

Bring up fintech competition and Bailey is quick to point out that fintechs have two sides. Certainly, they can represent challenging rivals. But fintechs can also be helpful partners to bring superior products and services to bank customers.

“There are many good fintechs out there that I can partner with and ‘plug-and-play’,” says Bailey. “We can take the best of each and bring them into our organization and embrace some of their technology.”

Key point: Bailey says that because some fintech partners are working for many banks, they can sometimes bring competitive approaches to market faster than some of the larger institutions that he counts among his competition.

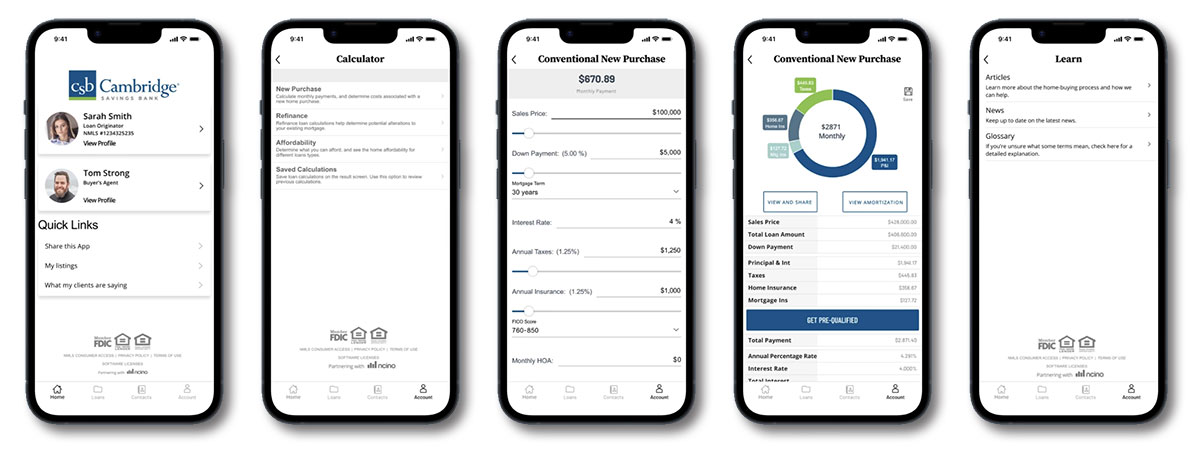

Beyond its Cambridge Bank app and the separate app for Ivy Bank, the institution also offers a dedicated mortgage app for home borrowers.

A service for applicants with loans in the pipeline is what Bailey dubs “the pizza tracker.” In mid-2025 the bank introduced the capability to see where in the process a mortgage application stands, much like the order tracker from Domino’s Pizza. Bailey credits fintech partner nCino with making this service happen.

Key insight: “We’re not just competing with banks anymore,” in terms of customer experiences, the veteran banker says. “We’re competing with Amazon and every other retailer. People want banking to be simple, one-click, and they don’t want a lot of upfront obstacles to keep banking from being easier.”

Multiplier effects: Bailey adds that improving the mortgage process with the tracker didn’t just improve CX. “Real estate agents that work with us have been sending us business because of it.”

Read more: How Proposed ‘Skinny’ Fed Accounts for Fintechs Could Alter U.S. Payments

Why Branches Still Matter to Cambridge Savings

In spite of the bank’s proclivity for digital approaches, Bailey says Cambridge continues to believe in branches. “Branches are even more relevant for a community bank. We have community centers in our branches that people in our neighborhoods use. And branches are still important to attract depositors.”

Bailey cites an example from his own family as evidence.

“I have a 17-year-old daughter, and she will never bank in a bank branch ever again,” says Bailey. “However, she walked into a branch to open her account. She wanted advice. I’m sure she’ll never step foot in it again because she uses mobile deposit and other channels, but she wanted a branch to open her account.”

Read more:

Financial Confidence Begins with Financial Understanding

Cambridge emphasizes financial education in multiple formats, including both live and online aid. Branches play a role in the live education effort.

“We want to make sure customers feel they are empowered to make their own financial decisions,” says Bailey. He says the growing evidence of the “K-shaped” economy means Cambridge Savings has two distinct customer groups, both of which it wants to serve.

New strategies require a new culture: The changing use of branches has also dictated some changes for Cambridge employees.

Bailey says many routine transactions have migrated out of branches into digital channels.

“So, we’ve had to upgrade our training for branch personnel, because more sophisticated transactions are what is coming into branches,” says Bailey.

Read next: To Win Against the Big Banks, Smaller Institutions Must Go on the Offensive