Big Banks Are Upgrading Their SMB Offerings. Why Community Banks Still Have the Edge

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

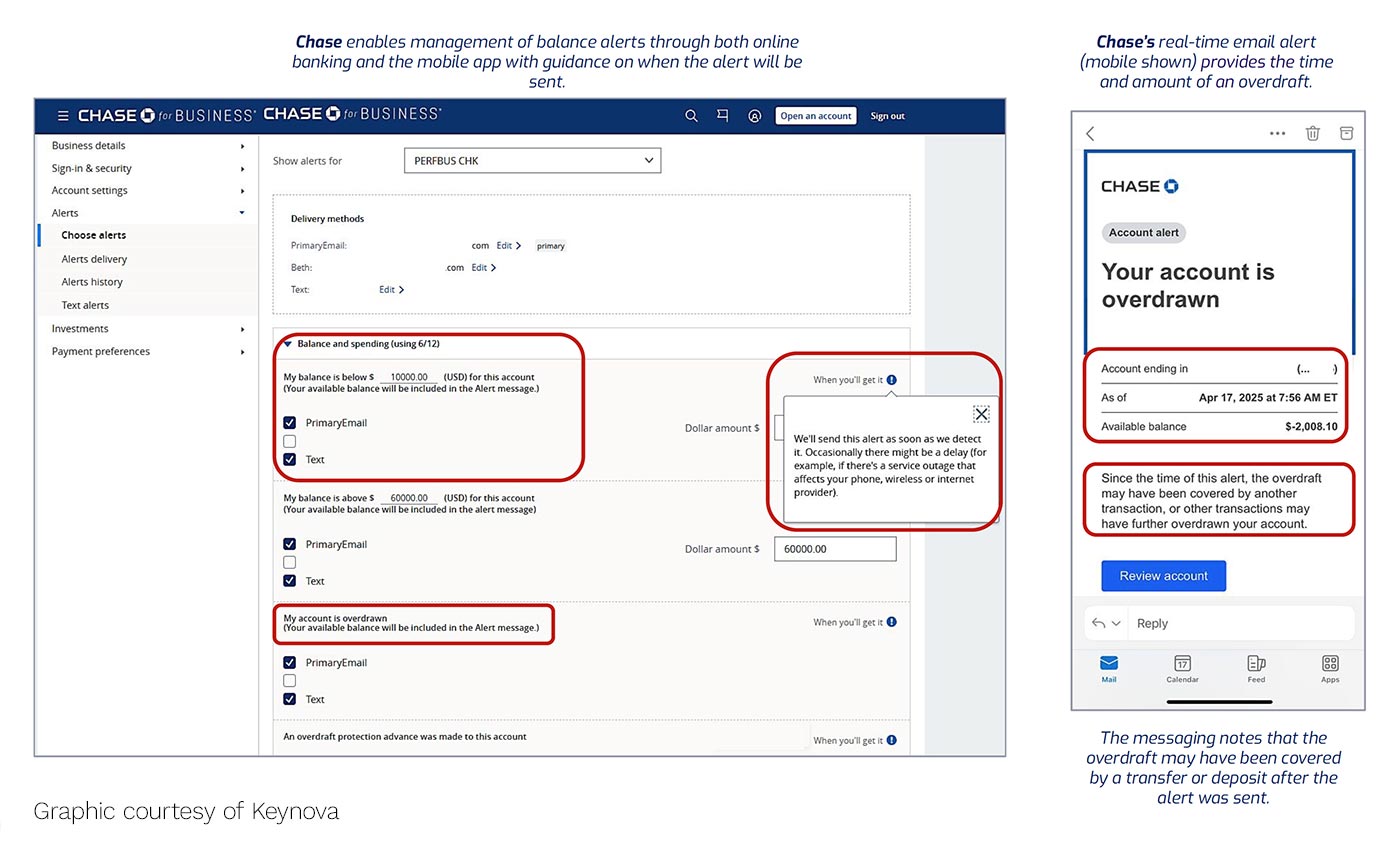

- Major banks are improving their small business online access and mobile apps, but some are missing key elements. One example: Alerts warning owners that their account could be overdrawn.

- Only one in five major banks provide aggregated transaction reports, and those that do could improve their offerings.

- According to Keynova Group, one key element routinely left out of all of the major bank digital small business channels is: the customer’s relationship manager.

Small business digital channels, including online and app access, are growing deeper and more sophisticated at major banks. Yet progress is uneven: Even as real-time messaging, payments management and security features push some players ahead of the pack, other institutions still have gaping holes.

More importantly, recent research by Keynova Group has found that one key feature — a low-tech one that many small business customers find crucial — is missing from every institution in the 11-bank sample the firm studies. (The banks include Bank of America, BMO, Chase, Citibank, Citizens, Huntington, PNC, TD Bank, Truist, U.S. Bank and Wells Fargo.)

Consider real-time nonsufficient funds and overdraft warnings: Of the 11 major players Keynova studied in its “2025 Small Business Banking Scorecard,” only about half — 55% — provide such alerts. Shortfalls can be an even bigger deal for businesses than for consumers, triggering fees and risking the embarrassment of returned business payments. (Four out of five institutions do send alerts when a balance actually goes negative or the account has shown suspicious activity.)

Part of the reason lies in the legacy processing systems that some major institutions still rely on, according to Susan Foulds, managing director at Keynova. They simply can’t pump the information to business-side online banking and apps in a timely fashion.

Foulds knows of one big bank that doesn’t send NSF and overdraft alerts until the next morning, after the damage has already been done.

Meanwhile, the missing low-tech element that Keynova identified is simply this: A lack of the human element in all 11 institutions’ business-side apps and online channels.

“None of the banks in our study are doing something seen routinely in insurance and wealth management digital accounts — they don’t list your banker’s name and their contact information,” says Foulds.

While contact centers can help with run-of-the-mill questions in off hours, says Foulds, some matters will come up that a small business owner or manager can only settle with the account officer or relationship manager.

Providing a way to get through to the banker who knows their account best would be a way of making such relationships stickier, Foulds believes, because establishing that kind of availability doesn’t exist now.

“Running a small business is not a nine-to-five job,” says Foulds in an interview with The Financial Brand. Even if they can’t reach their banker, they ought to be able to get hold of someone who can clear things up, she adds.

Discussing live communication with bankers may seem counterintuitive in the context of digital channels. Foulds disagrees.

“This is why so many community banks still corner the small business market, particularly outside of the large metro areas,” says Foulds. “Small businesses can pick up the phone and dial the banker who is managing their relationship.”

Read more: How Regional and Community Banks Can Compete (And Win) in Payments

Daily Expense Transaction Reports Are a Standout Practice

For many small firms, their business checking account is the financial hub of their company. Any feature that improves the utility of that account, then, serves busy owners and managers and keeps them focused on the banking relationship.

One service that’s still sparse among the big banks is the option of an email alert that gives small firms their current balance along with a summary of the day’s transactions in the account. Only one out of five institutions offer this feature. (Note that the study focused on each bank’s basic small business online and app services, and not on more advanced options that get into cash management, for example.)

Foulds says spend reports should be expanded to include not only transactions in and out of the customer’s core account, but also other relationships, such as a business credit card. She thinks this service should go beyond the single institution to include all financial relationships the company has that involve transactions. Offering such a service can help keep the bank that does so central in the customer’s mind.

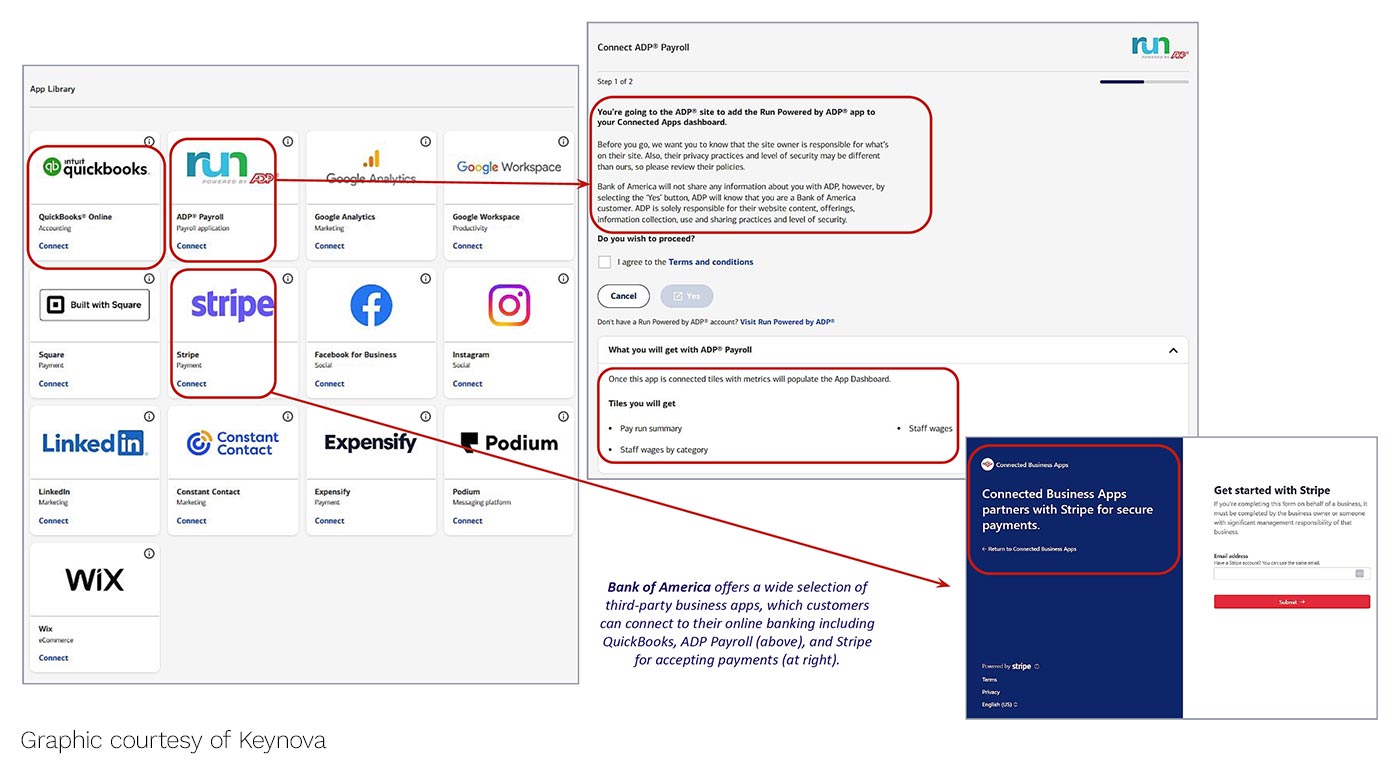

Another offering that’s still fresh is integration of third-party services that add value and functionality to the small business’ banking relationship. This includes such offerings as QuickBooks, Stripe and LinkedIn marketing.

Creating seamless connections between banking and these services is still nascent enough that it helped keep Bank of America at the top of Keynova’s annual ranking in the small business digital area.

Foulds noted that TD Bank also provides this service, using its “Small Business Dashboard” to enable customers to link their business accounts to accounting software.

Payment Flexibility and Ease Count for a Lot

Streamlining payments inbound and outbound plays an increasingly important part in the digital channels.

More institutions are offering invoicing services to small business customers from within their own digital channels.

Foulds says this practice can be a mutual advantage for the customer and the bank provider.

“QuickBooks is not simple for those who are not dealing with spreadsheets and finance all the time,” says Foulds. “So the fact that a bank provides a more intuitive way to send an invoice through their online banking without having to learn QuickBooks makes sense.”

In this way, as well, she adds, the small businesses’ financial hub can continue to be built around the banking relationship, rather than gradually migrating to the relationship with QuickBooks.

Money movement options are important to small businesses and leaders have been adding more choices to their digital channels. This includes Zelle — including its business-to-business variation, wires, external transfers, and automated clearinghouse transactions. Foulds notes that none of the banks are offering FedNow payments through their small business digital channels yet, but adds that Chase and Citibank have been offering The Clearing House Real-Time Payments option.

Read more: How to Streamline Banks’ Payments as Pathways Proliferate

Security Features Becoming Tables Stakes, But Some Still Mark Leaders

Given the continuing uptick in fraud, especially targeted at small firms, features working to control this are also paramount.

The study found that almost all of the banks researched offer businesses the capability of setting tiers of access for different people who have access to the company bank account. This applies to factors like the information they can view as well as the size of the transactions they can execute.

More banks are offering multi-factor authentication to safeguard higher-risk online and mobile transactions.

A new effort at BMO and Wells Fargo entails stronger controls at sign-in, including passkey authentication.

Passkeys dispense with the traditional need for passwords. In simple terms, the passkey approach uses a public key that is shared with the account and a private key connected to it that only the user possesses. It is stored on the device that created it, such as one’s smart phone.

The organizations backing the system say it can provide protection from phishing, interception and “man in the middle” attacks, where a third party inserts themselves between two parties who think they are communicating directly with each other.