Timing, the New Way to Outcompete Peers for Time Deposits

Timing CD promotions can make or break an institution's ability to attract critical funding. With billions of dollars in CDs maturing monthly, leveraging market intelligence and responding swiftly to competitor moves has never been more essential for staying ahead in the race for depositor dollars.

By Josh Williams, Head of Partnerships, CD Valet

Simple Subscribe

Subscribe Now!

Timing is crucial for institutions gathering time deposits, not just because time is a key feature of CDs. Depositors consider the offers available when they’re in the market for a time deposit. How institutions time their CD promotions can place them in top consideration or prevent their consideration altogether.

So how does an institution “time” its promotions and offers?

Timing offers is about competitive information. Institutions with sufficient clarity of their marketplace – such as the terms available, gaps in rate-term pairings, and pricing changes from competitors – can choose their place in that market. They can defend against new top-of-the-market promotions launched by competitors, craft combinations for new segments, and carve out niches in unserved spaces.

The industry landscape also has elevated the opportunity to use information to enhance CD competition. A 12-month maturity has been very popular among savers entering CDs or U.S. Treasuries. Given that popularity, a host of time investments – across CDs, share certificates, and U.S. Treasuries – are coming to term in 2024 and 2025.

As depositors consider where their funds land next, institutions can go after strategic priorities such as controlling rising cost of funds. Using information to navigate competitive offers, they can control pricing and still gather volume through information excellence when it comes to the pricing landscape of their markets.

A Wave of Mandatory Depositor Shopping

Depositors tend to focus on three features of CDs. Certificates pay a higher rate than fully liquid accounts, come with a “locked-in” time commitment, and often auto-renew at a low “disclosed” rate if not negotiated. If depositors want a market rate of return, shopping for the best rate is nearly always mandatory at CD maturity.

The volume of certificates reaching maturity in 2024 and early 2025 is historic. According to industry data, banks and savings institutions have more certificates on their books now than ever before. And they may receive more as rates incentivize locking savings at a high fixed rate.

Data from the FDIC indicates that time deposits have grown significantly in recent years. From a low point where CDs accounted for just 6.8% of total domestic deposits, they have surged to nearly $3 trillion, making up 17.7% of industry domestic deposits as of June 2024. This unprecedented growth highlights the growing role of CDs in the financial landscape.

Depositors read the news; they see the headlines about the Federal Reserve moving rates. Change breeds curiosity, and many will shop institutions because of that curiosity.

Rates above near-zero levels also incentivize curiosity because deposits can provide meaningful returns. When people become curious, they commonly visit their institution’s website. They also check the websites of the two or three other institutions they work with. And then, they check Google. Google will

favor those institutions paying for top promotional placement or those that have made significant investments in search engine optimization. (For these reasons, community financial institutions choose to work with CD Valet, a digital marketplace where banks and credit unions can leverage the authority and consumer traffic that the marketplace has earned with Google.)

Let’s look at how market intelligence can help your institution ensure it receives more consideration than the competition when depositors are in the market.

Dig deeper into deposit growth strategies:

- How Transaction Data Can Empower the Data-Informed Digital Banker

- How Can Banks Push Back Against Mounting Margin Pressure?

- As the Fed Trims Rates Banks Must Adjust Both Deposit and Credit Strategies

Winning Consideration: Using Information as a Competitive Advantage

Institutions can only outprice competitors so much. Competing on consideration through market intelligence offers a means of acquiring funding volumes.

Here’s how.

To begin with, banks and credit unions can assess depositor interest in CD terms and compare that data to their and competitors’ offerings. Is there demand for a term that has lower supply from institutions in your local market?

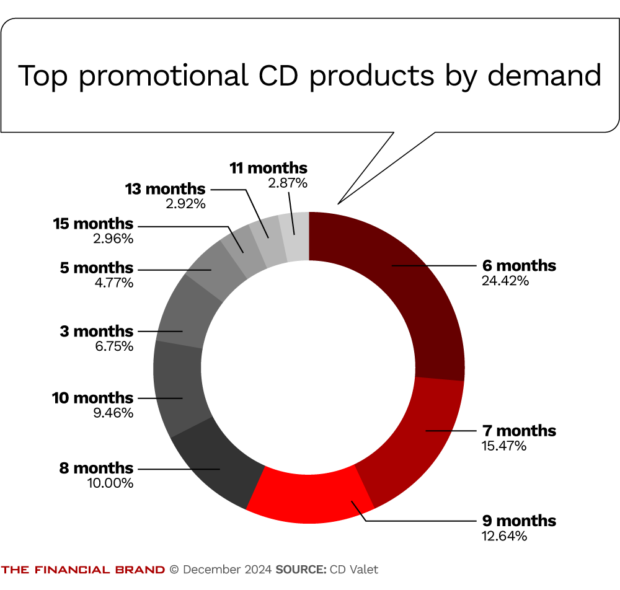

Promotional CDs are an excellent place to start. For example, six-month and seven- month CDs commonly take first and second place, respectively, for consumer demand of promotional CDs as measured through browsing data collected by CD Valet. Third and fourth place, however, vary widely. Some markets have no offerings for specific terms.

According to data gathered by CD Valet, a healthy contingent of depositors shows interest in terms less commonly offered on institution rate sheets.

In 2024, six-month CDs (24%), seven months (15%), and nine months (13%) command about 52% of the demand on CD Valet for promotional term CDs. Ten months (10%), eight months (10%), and three months (7%) receive over a quarter (27%) of the promotional CD browsing activity, according to CD Valet’s Market Intelligence Tool, which has data from over 4,000 U.S. banks and credit unions.

Pair your institution’s offers with CD terms that receive low to—or no—supply from competitors, and you can serve depositors’ unmet needs. Your institution then receives consideration through other means than a high deposit rate; you’re competing where there is demand and less competition. Your institution may even be the only one offering a term in their market.

Opportunity Cost: The Time Value of Information

When the Federal Reserve shifts rates, how much does it cost an institution – in terms of interest expense – to respond slowly with new offers? We don’t have a clear way to measure that cost. The opportunity cost, however, is easier to quantify if you look at it in terms of volume.

Consider a small independent gas station that updates prices slower than its competitors but shares a stop with larger corporate stations. When prices change, which station receives the most consideration, and what is the opportunity cost of being slower to update prices? The answer depends on how many drivers pass by in a day.

Dividing the $2.5 trillion in bank CDs maturing before April 2025 across the 12 months from March 2024 to March 2025, that’s $208 billion in deposits that reenter the market each month. About $6.85 billion will “drive by” banks and credit unions daily until March 2025. And that’s just the volume maturing in CDs. When the Federal Reserve announces a rate policy, the volume can be even more significant than that – whether it raises or lowers rates.

Banking institutions have a similar situation in their pricing operations. They don’t usually have faulty signs; they conduct a slow and manual price survey by visiting their competitors’ websites. That slow and manual market intelligence process affects their standing in depositors’ consideration for deposit dollars that must find a new home on any given day. Industry data suggests that opportunity cost is significant.

Information Arbitrage: The Opportunity in Better Timing

As interest rates rise and fall, executives should add a new question to their strategic plan: What if we knew overnight how and when competitors change pricing? What if we could respond much more quickly?

When competitors remain dependent on longer manual processes, the institutions with faster feedback loops receive far more chances to woo CD holders by simply addressing the market in closer to real-time. All banking institutions need a certain amount of deposit volume to operate. Pricing acumen improves the institution’s success in executing promotions to attract that volume. In turn, that decreases the likelihood that a bank or credit union will need to obtain funding by raising prices or going to wholesale markets.