The Midcap Banking Crisis: Why Retail Deposits Are the Key to Survival

By David Evans, Chief Content Officer at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- The 2023 banking crisis revealed a stark reality: midcap banks with retail-focused deposit bases dramatically outperformed peers reliant on commercial or wholesale funding.

- Yet midcap banks’ share of primary checking accounts has declined nine percentage points since 2015, while their customer base skews dramatically older than the general population. With baby boomers’ share of deposit balances expected to fall by almost half by 2035, and Gen Z’s share projected to double, midcaps must urgently modernize to attract younger consumers.

- The challenge is compounded by perception gaps. Only 27% of midcap customers see extreme value in their services versus 37% at regional banks.

The March 2023 banking crisis proved a watershed moment for US midsize financial institutions. In just four weeks, banks beyond the country’s 25 largest experienced over $220 billion in deposit outflows as customers fled to institutions perceived as more stable. The turmoil exposed a fundamental vulnerability: concentrated pockets of clients with larger deposit balances represented systemic fragility that could trigger rapid capital flight during periods of uncertainty.

The crisis aftermath also revealed a stark performance divergence. Midcap banks — defined as institutions with $10 billion to $100 billion in assets — that maintained higher concentrations of retail deposits significantly outperformed peers dependent on commercial or wholesale funding. The numbers tell a compelling story about the stability value of granular retail funding.

According to a new report from McKinsey & Co., institutions with above-median retail deposits as a share of total deposits (above 42% in Q4 2024) achieved net interest margins of 3.46%, compared to 3.02% for banks below this threshold. This 44-basis-point advantage translates to substantial bottom-line impact. These retail-focused institutions also maintained cost of funds 19 basis points lower at 2.48% versus 2.67%, demonstrating the pricing power that comes with relationship-driven deposits.

The growth differential proved equally dramatic. Banks with stronger retail franchises experienced deposit growth of 6.01% year-over-year compared to 4.42% for peers, while asset growth reached 5.24% versus just 2.22%. This performance gap, sustained over time, creates compounding advantages that separate winners from strugglers in the midcap segment.

Why Retail Deposits Deliver Superior Resilience

Retail deposits demonstrate greater stability for two fundamental reasons. First, customer inertia plays a powerful role: individual consumers prove typically less sensitive than businesses to interest rate changes and tend to maintain banking relationships rather than constantly optimizing for yield. Second, the strength of personal relationships creates switching costs that commercial relationships often lack.

The granular nature of retail deposits — composed of funds from many individuals rather than concentrated commercial relationships — also provides inherent diversification. A single large commercial depositor withdrawing funds can create immediate liquidity stress; thousands of small retail customers would need to act simultaneously to generate equivalent impact, a far less likely scenario.

The Generational Time Bomb

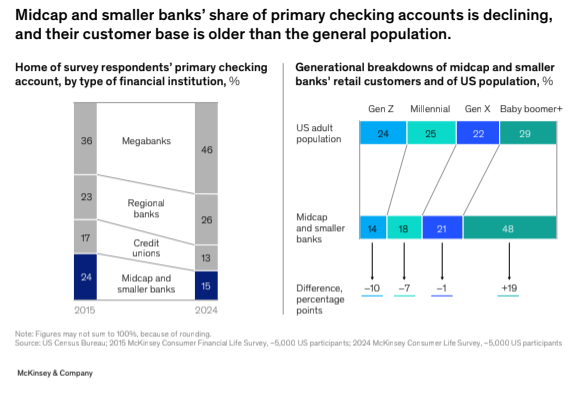

While retail deposits provide near-term stability, midcap banks face a demographic crisis that threatens long-term viability. Baby boomers and the Silent Generation currently account for 42% of midcap and smaller bank customers, significantly higher than their 29% share of the US adult population. This overrepresentation reflects historical success with older consumers but signals future vulnerability. Meanwhile, millennials and Gen Z represent only 32% of midcap customers, compared to 50% at megabanks and 40% at regional banks.

This demographic imbalance directly impacts deposit stability projections. Consumers born before 1965 currently account for 39% of consumer deposit balances nationwide, making them essential to near-term funding. However, their share is expected to decline to just 20% by 2035 as wealth transfers to younger generations and natural attrition occurs.

The Rising Importance of Younger Consumers

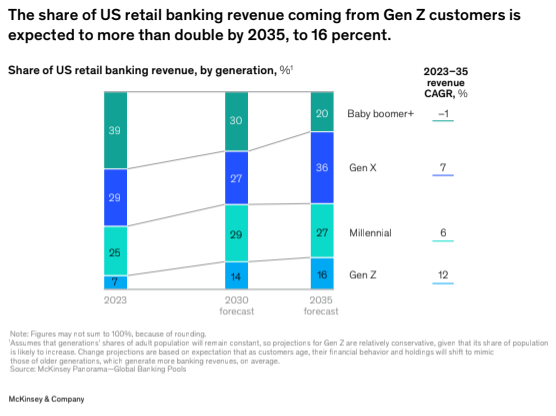

The generational shift in banking revenue potential is dramatic. According to McKinsey Panorama projections, millennials and Gen Z will account for 43% of retail banking revenue by 2035, up from 32% in 2023. Gen Z alone is projected to more than double its revenue share from 7% to 16%, representing 12% annual growth, the fastest of any generation.

This revenue growth reflects both increasing earnings as these consumers advance in their careers and their expanding financial needs as they purchase homes, start families, and accumulate investable assets. Banks that successfully establish primary relationships with these consumers in their 20s and 30s position themselves to capture decades of deepening financial engagement.

The institutions effectively engaging both ends of this generational spectrum — maintaining relationships with older, deposit-rich customers while building relevance with younger, high-growth consumers—will be best positioned to sustain stable, growing funding bases supporting long-term value creation.

The Primary Relationship Erosion Crisis

The most concerning trend for midcap banks involves their declining role as consumers’ primary financial institution. Market share data reveals systematic losses to larger competitors, particularly megabanks, with implications extending far beyond simple account counts.

Midcap and smaller banks accounted for just 15% of primary checking accounts in 2024, down from 24% in 2015, a nine-percentage-point decline representing 38% relative market share loss. Over this same period, megabanks increased their share by ten percentage points, while regional banks gained three percentage points.

This shift reflects more than competitive dynamics; it signals changing consumer preferences and expectations. Among millennials and Gen Z consumers, more than half identify megabanks as their primary financial institution, while just 25% consider midcap banks their main provider.

Primary banking relationships matter profoundly because they drive share of wallet across products. Consumers typically concentrate their financial lives with one or two institutions, making primary bank status crucial for cross-selling opportunities, relationship deepening, and lifetime value maximization. Weakening primary relationships reduce opportunities to demonstrate value and build the loyalty that drives deposit stability.

The Perceived Value Crisis

Consumer perception data reveals why midcap banks are losing primary relationships. Only 27% of consumers who have a midcap or smaller bank as their primary institution say it provides “extremely good value,” compared to 37% for regional banks, 31% for credit unions, and 29% for megabanks.

This value perception gap has widened over time. Between 2015 and 2024, perceived value increased more for mega and regional banks than for midcaps, likely driven by larger competitors’ improvements in digital experiences and more targeted consumer incentives. The relative decline leaves midcaps increasingly vulnerable to poaching by institutions perceived as offering superior value propositions.

The perception problem proves especially acute with younger consumers. Only 28% of millennials and 23% of Gen Z consumers with midcap primary banks perceive extreme value, compared to 49% and 36% respectively for those with regional bank relationships. Given these groups are the most digitally engaged and value-conscious, the urgency for midcaps to adapt to evolving expectations becomes clear.

The Cross-Selling and Digital Capability Gaps

Beyond primary relationship challenges, midcap banks demonstrate significant performance gaps in product penetration and digital engagement—areas directly tied to revenue generation and operational efficiency.

Missed cross-selling opportunities Midcap banks lag larger competitors significantly in cross-selling higher-value products to checking account holders. The gaps remain relatively small for savings accounts but become substantial for credit cards, mortgages, and brokerage accounts — products generating higher revenues including noninterest income and deeper customer relationships.

This cross-selling shortfall reflects both capability limitations and missed opportunities. Many midcaps lack the analytics, relationship management tools, and systematic approaches that larger institutions use to identify propensity to buy and deliver targeted offers. Branch staff often focus on service rather than sales, missing natural opportunities to deepen relationships through consultative discussions about additional financial needs.

The digital engagement disadvantage While midcap banks excel at customer service, their operating model remains heavily dependent on physical channels in an increasingly digital world. Only 65% of midcap and smaller bank customers report using digital channels as their primary servicing method, compared to 73% at megabanks and 70% at regional banks.

Conversely, midcaps lead in dependence on human-touch service: 22% of their customers rely most often on branch tellers or call centers, more than any other bank type. While this reinforces trust and loyalty with current customers, it creates cost pressures, limits service scalability, and becomes a compounding disadvantage for attracting younger consumers.

Among millennials, 79% cite mobile apps or digital platforms as their primary banking access point; for Gen Z, the figure reaches 70%. These digitally native consumers increasingly view superior mobile apps and online banking as primary factors in choosing financial institutions. Midcaps’ limited digital capabilities directly undermine their ability to compete for the very consumers whose relationships will drive future deposit growth.

The Strategic Playbook for Midcap Survival

Facing these challenges, midcap banks must pursue focused strategies that leverage their strengths while systematically addressing competitive disadvantages.

In its report, “Banking on the Next Generation: A Playbook for US Midcap Banks”, McKinsey identifies five moves that offer the highest impact for building sustainable retail franchises.

1. Transform Branches into Productivity Engines

Despite strong customer service reputations, midcap branch operations often aren’t optimized for customer acquisition or relationship deepening. Midcaps trail mega and regional banks by more than ten percentage points on branch productivity measures. If midcap branches had improved productivity at peers’ rate over the past five years, they would have captured an additional $200 billion in deposits.

Transformation requires equipping frontline staff with analytics-powered lead generation, targeted customer lists, and real-time insights guiding outreach. Implementing structured routines including daily huddles and individualized coaching supported by gen-AI platforms helps prioritize high-potential opportunities and enhance interactions.

Branches remain critical acquisition channels for midcaps, generating up to 80% of new accounts versus just 8% through digital channels. Megabanks and regional banks, by comparison, acquire nearly 30% of new accounts digitally. Rather than pruning branch networks, midcaps should pursue disciplined footprint expansion in high-potential markets while dramatically improving productivity per location.

2. Pursue AI-Driven Digital Transformation Strategically

Agentic and generative AI promise to reshape banking and boost productivity but realizing benefits requires more than isolated use cases. Top-performing banks integrate AI into strategic planning, setting ambitious goals across business units focused on high-impact areas aligned with core strategy.

Midcaps can’t match megabank spending power, so they must adopt strategic, phased approaches relying on cost-effective solutions and partnerships. Key strategies include focusing on high-impact, targeted AI initiatives addressing specific business needs; using cloud-based AI services to reduce infrastructure costs; collaborating with fintechs and technology vendors to access innovative solutions; and implementing open-source AI tools and frameworks.

Rather than spreading resources thin, midcaps should concentrate transformation budgets on digital journeys that matter most: routine service interactions like transferring funds, paying bills, depositing checks, resetting passwords, and viewing balances. When these core journeys are digitized effectively, they reduce pressure on call centers and branches while significantly boosting customer satisfaction — especially critical for engaging younger consumers expecting seamless digital interactions.

2. Build Precision Digital Marketing Capabilities

Capturing digitally native younger consumers requires precision-targeted marketing strategies. Midcaps should invest in performance-focused digital engines using data analytics to identify high-intent prospects, engage them with relevant content, and convert them through seamless onboarding.

This approach includes integrated tactics like SEO, social media, retargeting for conversion, referral programs, loyalty initiatives, and personalized email campaigns. Each stage should be closely managed to minimize customer loss and maximize ROI.

Using shared data platforms or marketing utilities may allow midcaps to access sophisticated targeting capabilities without requiring the same up-front technology investment as larger peers. Beyond attracting new customers, these tools powerfully improve engagement and retention, helping midcaps proactively manage term deposit renewals, engage dormant customers, and connect with those undergoing life changes.

4. Focus on High-Value Customer Segments

Midcaps don’t need to compete across all customer segments to succeed. Focusing on affluent and mass affluent individuals — including small business owners already served through commercial franchises — represents significant opportunity. These segments have complex financial needs, opening doors for midcaps to deliver greater value through integrated offerings.

Midcaps can enhance wealth and business banking capabilities by acquiring registered investment advisors or partnering with established wealth managers to broaden advisory services. Equally important is tightly integrating commercial and wealth offerings to address small business owners’ personal and business needs simultaneously.

Building this proposition requires investment in foundational capabilities: granular customer segmentation, deep analytics, and robust relationship management tools identifying high-potential customers and tailoring engagement strategies. In-branch bankers and relationship managers need training and tools to recognize wealth management opportunities and deliver consultative advice.

5. Refine Product Portfolio Through Specialization

Midcaps often err by attempting to compete across all product categories, stretching resources thin. Embracing consumer preferences to unbundle financial lives, midcaps can become preferred specialists in certain areas — best-in-class small business banking or specialized unsecured lending products — winning loyalty for targeted services.

Critical steps include identifying products most aligned with target customer segments and business objectives. Strengthening home equity lines of credit for affluent consumers can deepen those relationships. Offering digitally seamless products like app-accessed savings accounts or credit cards tailored to younger consumers’ lifestyles engages those prioritizing ease of use and innovation.

This refined approach matters given midcaps’ room for growth in savings, credit cards, and retirement products—areas presenting significant opportunities as younger generations accumulate wealth and seek providers meeting evolving needs.

These moves, McKinsey argues, offer midcap banks a path to sustainable growth. The performance data from 2024 demonstrates that success is possible: retail-focused midcaps are already delivering superior results. The challenge is extending this model before demographic headwinds and competitive pressures create irreversible disadvantages. The institutions that act decisively today will build resilient deposit bases that separate survivors from casualties in the next banking crisis.