Forget Share of Wallet. Engagement and Outcomes Are Now the Drivers of Primacy

By Jessica Kendall, Senior Director, Content, MX

Simple Subscribe

Subscribe Now!

Executive Summary

- Primacy has shifted from deposit volume to engagement and personalized outcomes. While 80% of consumers still have a primary financial provider, success now depends on delivering data-driven experiences that rival Apple and Amazon, not just holding the most money.

- Convenience beats rewards in driving consumer behavior. Nearly half use a “top of wallet” account for most purchases based on ease of use, and 60% have never switched direct deposit. While incentives attract customers, simplicity drives long-term engagement.

- Consumers want personalized experiences but providers are underdelivering. Over half would share more data for better experiences, yet 30% receive irrelevant messages. With 67% abandoning apps with poor experiences, providers must leverage data effectively or lose customers.

Is primacy dead? No, we don’t think so. And, neither do consumers. Our previous research found that 80% of U.S. consumers say they have a financial provider they consider as their primary financial provider.

Today’s primary relationship just looks different than in the past. Consumers don’t have one account anymore — they have multiple accounts. Consumers don’t turn to just one financial provider to meet their needs — they look for the best fit.

At the same time, consumers aren’t just comparing their financial experiences to those from other financial providers. They’re comparing them to Apple, Amazon, Netflix, and other data-driven, personalized digital experiences.

As a result, today’s definition of primacy isn’t just about where the most money gets deposited. It’s about engagement and outcomes.

MX’s latest consumer research shows what consumers prioritize when it comes to the apps, accounts, and financial providers they engage with most.

Want more insights like these? Check out MX’s content hub: Data in Action

What Do Customers Want?

Consumers want more simplicity. As a result, they are consolidating apps, accounts, and financial providers. In the past 2 years, at least 1 in 10 consumers have made an effort to consolidate the number of financial providers they have accounts with today. Today, 46% of consumers say they only have 1 to 2 financial accounts.

Consumers prioritize convenience when it comes to “top of wallet” accounts. Our research makes it clear that consumers often prioritize convenience in their financial lives. In fact, 67% of consumers say they keep their bank or credit card information on file for recurring bills and/or services, leveraging it to pay for everything from streaming services and utilities to rent and insurance.

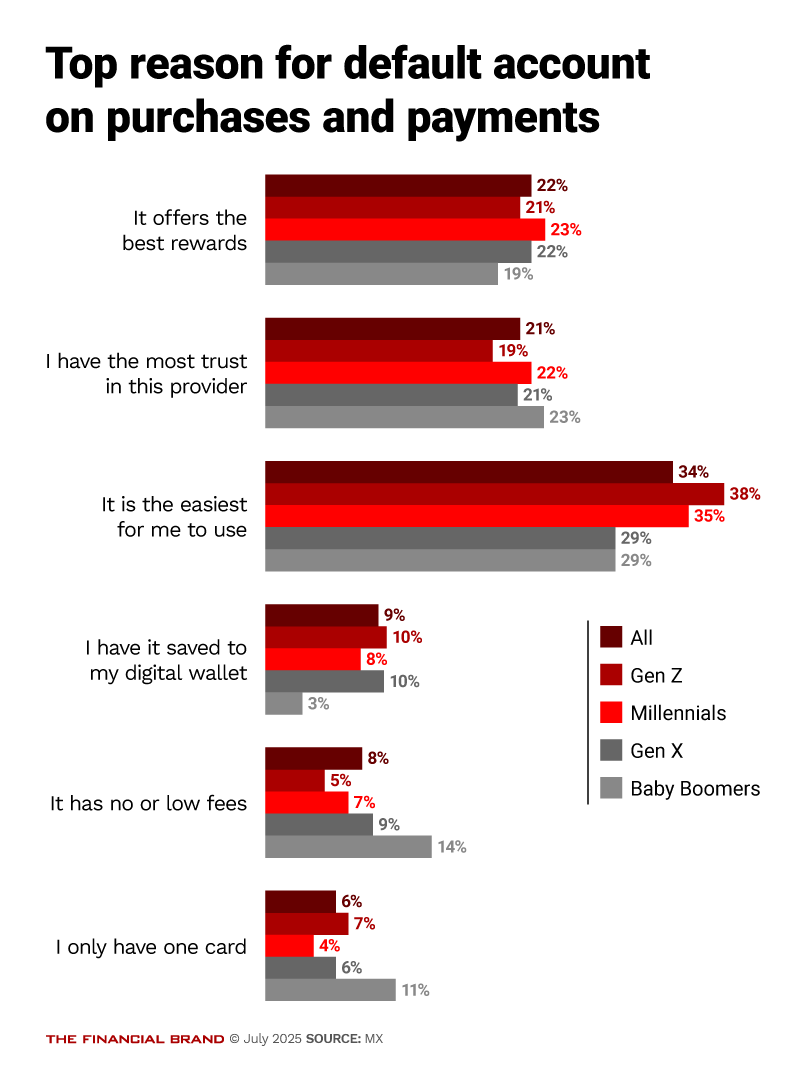

In addition, 44% of consumers say they have a “top of wallet” account they use for the majority of their purchases and payments. Why? Top reasons include it’s the easiest for them to use, offers the best reward, or it’s the most trusted.

Consumers are also likely to save their bank or credit card information with a store or vendor for online purchases. In fact, 1 in 5 consumers say they do this whenever it is an option. And, 45% have created an account and saved their information with an online store after just 1 purchase.

Convenience trumps rewards, but rewards can open the door. For most consumers, setting up a direct deposit at a financial institution yields a long-term relationship. In fact, 60% of consumers say they have never switched their direct deposit to a different financial institution. But, better rates and incentives could drive more consumers to consider a switch. When asked what is likely to make them switch their direct deposit, the top 3 factors for consumers are:

- Ability to earn higher interest rates (42%)

- Concerns about fraud (15%)

- A data breach or privacy concerns (13%)

What About Cash Incentives?

In addition, when asked specifically if a cash incentive would encourage them to switch, 44% of consumers say yes. That said, while offering cash incentives and better rates can drive new account openings, the financial providers who make it simple and easy to use their accounts will have greater engagement in the long run.

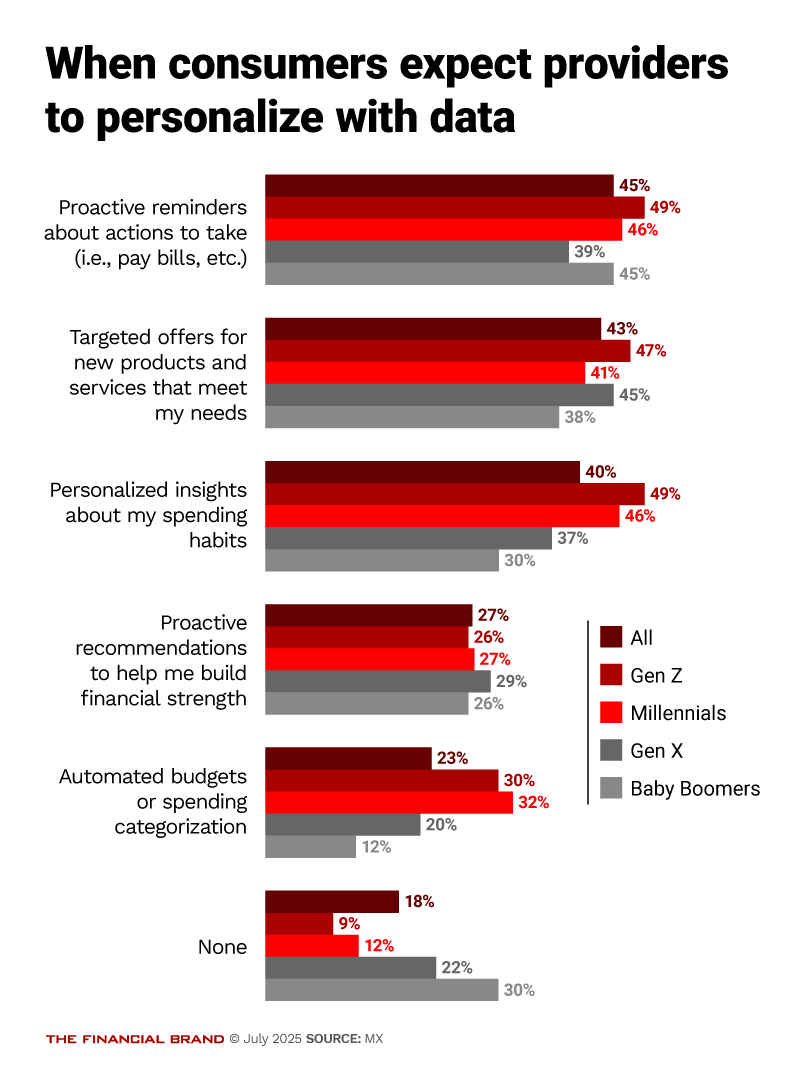

Consumers expect financial providers to use their data to drive better outcomes for them. Our previous research shows most more than half of consumers would give their financial provider access to more of their data if they knew it would result in a better experience. However, many financial providers still struggle to leverage data effectively. In fact, 30% of consumers agreed they often see messages from their financial provider that are not personalized or relevant for them. And, less than half of consumers (42%) believe financial providers use their data only in ways that will benefit them.

So what do consumers want from their data? When asked in which cases they expect financial providers to use their data to offer a more personalized experience, only 18% of consumers said none.

Finally, it’s no surprise but consumers want consistently good mobile experiences and customer service. Sixty-seven percent of consumers say they will stop using a mobile app if the experience changes for the worse. In addition, 51% of consumers say they have closed or switched a financial account.

This shows that consumers aren’t afraid to move to a new financial institution if their current one doesn’t meet their needs as often as it takes. When asked how often they have opened a new account, 1 in 4 consumers are doing so at least once per year on average.

It’s clear that basic features and functionality are no longer enough to earn — or keep — primacy among consumers. As consumers become more selective, financial providers that deliver personalized money experiences that genuinely solve their financial needs in simple, intuitive ways will win.