From Rosie the Maid, a humanoid robot fictional character from the 1960’s animated TV series The Jetsons, to Fritz Lang’s Metropolis and Isaac Asimov’s ‘I, Robot’ and even WALL-E, C-3PO, Optimus Prime and R2-D2, robots have always fascinated and entertained consumers. But, in real life, they have been far less entertaining (or functional).

Sure, they have become a part of every factory room floor in manufacturing and have played major roles in space exploration and taken on difficult and dangerous tasks, but until recently, robots have not proven to be nearly as intelligently evolved (or financially viable) as projected.

That is all changing. The exponential growth in the power of technology, digital sensors and information processing has improved the potential of robots at the same time as the innovation and investment in these devices is taking off. Both businesses and consumers can benefit from the rise of the robots.

While much focus is placed on making smart people smarter, the leading benefit of robots and artificial intelligence (AI) processes today is to standardize delivery followed by improved domain expertise and skills as subject matter experts, including language capabilities.

Robots and AI in Banking

The primary opportunity for robots and AI tools in the banking industry at this time is that they can extend the creative problem-solving capabilities and productivity of human beings and deliver superior business results, states Cognizant in a report on the use of this new digital technology. Their research shows that through these technologies, humans have the potential of attaining new levels of process efficiency, such as improved operational cost, speed, accuracy and throughput volume.

The opportunity for cost savings is the first place where AI and process automation will impact banking. In the Cognizant study, 26% of banking respondents stated they have enjoyed 15%-plus cost savings from automation in their front office and customer-facing functions compared with one year ago, and 55% expect those same levels of savings (15% or more savings) within the next three to five years.

According to Cognizant, the top drivers for automation beyond cost savings include:

- Reduced error rates (21%)

- Better management of repeatable tasks (21%)

- Improved standardization of process workflow (19%)

- Reduce reliance on multiple systems/screens to complete a process (14%)

- Reducing friction (11%)

Cognizant found that nearly half of the banks surveyed (45%) have also seen at least 10% revenue growth from analytics aligned with their front office and customer-facing functions, a number that is anticipated to rise to nearly three out of every four banks during the next three to five years. The result is that banking is more inclined than other industry surveyed to automate their processes, often due to their need to better focus on customers.

While process automation and the processing insight from transactions can impact all areas of the banking organization, including human resources, finance and accounting, customer service and even new product development, the impact of FTEs is projected to be significant. In fact, 19% of banks surveyed by Cognizant believe there can be a 25% FTE reduction today, with 28% believing a 25% reduction in FTEs will be possible in the next 3-5 years.

So what jobs may be at risk? As noted in a recent post by futurist and best-selling author, Brett King on the future of AI in banking, a study released by Oxford Martin School’s Programme on the Impacts of Future Technology evaluated how susceptible are jobs to computerization. Evaluating around 700 jobs, and classifying them based on how likely they are to be computerized, the jobs in the financial services industry that fit the studies criteria include:

- Bank Teller

- Loan Officer

- Mortgage Broker

- Insurance Claims and Policy Processing Clerk

- Insurance Underwriters

- Claims Adjusters, Examiners and Investigators

- Bookkeeping, Accounting and Auditing Clerks

- Tax Preparers

When asked about the biggest challenges associated with efforts to digitize processes, executives across industries say that data security is the biggest issue they confront, now and in the future. Fifty-two percent of respondents to the Cognizant survey indicated that data security is the chief challenge today.

It is believed that as digital processes proliferate, and as leaders see the value they create, an entirely new ecosystem of value-added services will develop to ensure the security, risk, privacy and compliance of the value chain of information these processes generate.

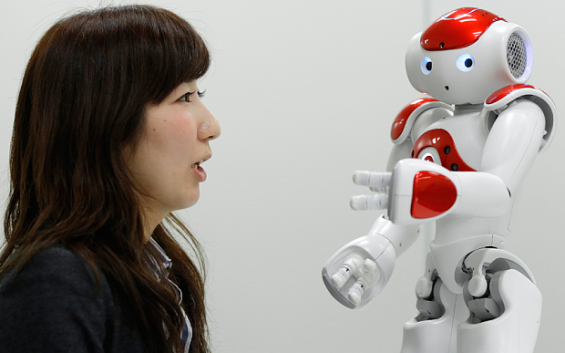

Nao and Pepper Entertain and Serve Banking Clients

As a ‘living’ example of how robots can be utilized in financial services, Bank of Tokyo-Mitsubishi UFJ took a first step toward employing non-human staff in April, with the introduction of a customer service humanoid robot at its flagship Tokyo outlet. Standing 58 cm tall and weighing 5.4 kg, the Nao robot worked at the reception area, according to Mitsubishi UFJ Financial Group Inc.

The robot, named Nao, was developed by French company Aldebaran Robotics, a subsidiary of Japanese telecom and technology giant SoftBank Corp., speaks Japanese, English and Chinese and was thought to be the first among the world’s major financial institutions to employ a customer-facing robot.

The robot uses various gestures and analyzes facial expressions and behavior to provide context appropriate responses to customer questions. It operates in 19 languages, offering the bank significant opportunity to expand the language coverage should the robot service take off.

While the robot is not intended to replace branch workers with a robot, they are being used to meet and greet customers, answering simple questions with various languages, freeing up some of the branch staffs’ time to work on more value added services. High-definition cameras record and match different customers, so identification can begin as soon as the customer steps through the door of the branch.

“Currently, in a lot of branches, there are cases where quite a few customers don’t speak Japanese or English and so we can have Nao do an initial check (on their needs) so that it can lead to a trouble-free setting up of an account or other carrying out of other administrative issues,” said Tadashi Betto, Bank of Tokyo-Mitsubishi UFJ Chief Manager of eBusiness and IT Initiatives Division.

Using stored insight, the robot routes the customer to the appropriate person based on past experience, products utilized or current mobile activity. Nao uses each interaction to learn a customer’s preferences and personality which enables the robot to increase the accuracy of each subsequent interaction.

Nao lasts 12 hours between charges, costs approximately $8,000 and can remember details from more than 5.5 million customers and over 100 different products. While there are limits to Nao’s capabilities (currently), this is both cheaper and more product conversant than any human in the same role.

Meanwhile, local competitor Mizuho Bank also plans to use a robot to assist customers in the next few months. Mizuho will use Pepper, Nao’s big brother, at several of its branches in much the same way as Bank of Tokyo-Mitsubishi UFJ.

Pepper, roughly twice the size of Nao, could become the first humanoid consumer robot and the beginning of an era of mechanized, cloud-connected ’emotion-reading’ digital assistants. Having gone on sale to the public in June for roughly $1,600 (plus data charges), the robot communicates in multiple languages, using sensors and cloud-based artificial intelligence (AI) capabilities and having the ability to evolve its skills over time through ongoing learning.

“Thanks to its ’emotion engine,’ Pepper can recognize human feelings and simulate them. It can also learn new skills as it spends more time with users and connects through the SoftBank cloud to thousands of other Peppers,”says its developers.

Robots Invade the U.S.

Sterling Bank & Trust in California have introduced two robots as greeters at the bank’s new locations opening in Cupertino and Alhambra, in the Los Angeles area. As part of their ‘training,’ the two robots made appearances at the bank’s San Francisco branches.

More a novelty than providing any significant off loading of duties during the initial use at Sterling, the robots are highly popular with children and grandchildren, said Steve Adams, senior vice president of Sterling Bank & Trust. The robots demonstrate kung fu moves and dancing while also greeting customers and handing out bankers’ business cards.

Hello Watson

IBM previously announced that its Watson-based chat advisor application built banking is being adopted by banks and other financial institutions for customer service and scaling wealth management. Genesys, a customer service company, will use IBM’s Watson system to better handle its clients’ customers’ needs. Banks are the service’s first clients. This same system is being used with the Pepper robot implementation discussed above.

IBM also sees artificial intelligence playing a big role in bringing wealth management to the masses. The intention is to take the expertise of wealth advisors and build it into a system so that people can interact with the system to get the first parts of the wealth management conversation handled. While using AI for wealth management goes beyond simple Q&A applications, Singapore development bank DBS as well as the Australian bank ANZ are already developing wealth management applications that are based on Watson.

“The goal is to take basic customer service and the wealth advisor to scale. Robotics are going to handle client interaction that doesn’t have to be face to face,” said Mike Rhodin, senior vice president of IBM’s Watson’s group. For more on robo-advising, Chris Skinner has discussed this well on his Financial Services Club Blog.

Barclays also made an announcement around the use of robot technology to make money transfers and to perform other rudimentary tasks. An artificial intelligence (AI) system similar to Apple’s iPhone personal assistant Siri may be used so that people will be able to talk to a device and receive the information they ask for.

“We’re very soon going to be entering a world where we may not have to be physically touching a device in order to execute transactions or to be able to engage with computers,” Derek White, chief design and digital officer at Barclays, told CNBC in an interview at London Technology Week. It is thought that Barclays could potentially design apps that integrate with such robot systems allowing users to do banking by talking to their mobile devices.

Preparing for the Robot Revolution

According to David Brear from Think Different Group, robots as the replacement for humans is a ways off. On the other hand, he emphasizes that, since the best customer branch experience is based on a deep understanding of the consumer, their situation and a good degree of empathy, artificial intelligence could definitely help in supplementing current, somewhat misguided and frustrating branch experiences.

“The better use of data and use of AI to standardize the decision making process should lead to every customer interaction being with empowered staff at the very top of their game. So rather than replacing them with an ‘android,’ we are heading towards improved technology and data facilitated discussions and meetings.”

When asked about the application of robots and AI in the branching system, Chris Skinner, chairman of the Financial Services Club and author of the best-selling book, Digital Bank: Strategies to Launch or Become a Digital Bank provided the following thoughts:

Most banks have used humans as robots in branches for years, (disempowering tellers and purely asking them to process transactions accurately first time, every time). These are the functions we’ve been replacing for years. After all, an ATM is an ‘Automated Teller Machine’ … a robot teller.

We should now be looking at how we can use digital functions to augment human processes. Instead of the current ‘product push’ using a flag system that provides the teller (or ATM) with a standard cross-sell message, systems should detect intelligently that the customer had looked at a specific bank service on their mobile device recently and alert the thinking customer service concierge – a role that has nothing to do with telling and transactions – allowing a personalized greeting.

Robotic process automation with sophisticated technologies is here to stay. Humans will remain essential to how knowledge work is orchestrated and managed, but technologies can now create more effective knowledge workers while simultaneously generating and capturing data that can improve processes and eliminate wasteful steps.

One of the insights of Asimov was that it is easier to ask such questions when the technology is more human-like. With this in mind, robots could serve as the collectors of new insights and perspectives – as people look at them and see them looking back … with some form of automated understanding of their needs, temperament and behavioral tendencies.

Start today, imagine how the future of work will look when digital machines, information and processes help humans do their jobs better, faster and with greater impact. By automating systems and interpreting data and insight, robots have the potential to work side-by-side with humans, allowing them to serve customers more effectively.