How Much Do Online Reviews Matter to Banking Decisions? A Whole Lot.

Almost 90% of banking consumers say they use online reviews to make their banking decisions. Most important are user reviews on Google – while over 40% have never heard of Bankrate, WalletHub, or SmartAsset.

By Corey Wrinn, Rivel Banking Research

Simple Subscribe

Subscribe Now!

Why ask one person for a recommendation when you have the wisdom of millions at your fingertips?

Online reviews have become a crucial factor in shaping consumer decisions across various industries, including the banking sector. The influence of these crowdsourced opinions is undeniable, as consumers increasingly seek transparency and authenticity in their choices. In research exclusive to The Financial Brand by Rivel Banking Research in Q2 2024, among a national sample of banking consumers, 78% of banking consumers say they consistently utilize online reviews when they are deciding on their new home for a bank account.

This staggering statistic underscores the power of online reviews in swaying consumer behavior and highlights the need for financial institutions to prioritize their online reputation management strategies. As consumers navigate the complexities of selecting a banking partner, they turn to the collective wisdom of their peers, seeking insights into everything — from customer service quality to account fees and digital banking experiences.

Digital Word of Mouth: It’s A Generational Thing

Our previous research has shown how younger generations have flocked to mobile apps for their everyday banking. Their digital affinity extends beyond just app usage — younger consumers are also more inclined to rely heavily on online reviews when selecting financial institutions.

Millennials and Gen Z consumers, having grown up in a world saturated with online information, have developed the keen ability to sift through vast amounts of user-generated content and place significant trust in the collective experiences shared by their peers. According to Rivel’s research from Q2 2024, 88% of both generational groups rely heavily on online reviews when evaluating a new financial institution or banking product. Only 78% of Gen X consumers and 61% of Baby Boomers have the same level of trust and usage.

Where the Young Generations Go:

Nearly nine out of 10 of every Millennial and Gen Z consumer say they lean heavily on online reviews.

Unlike older generations who may prioritize personal experiences, recommendations from family and friends, or traditional advertising, these younger cohorts are more likely to consult online review platforms, social media, and other digital channels to inform their banking decisions. This reliance on online reviews aligns with their preference for instant access to information and their comfort with leveraging digital resources for decision-making processes.

With that mindset, where should banks focus on managing and tracking their ratings, scores and reputation across the web?

First, The Right Platform Matters

Consumers are looking for good products, good value and, importantly, good service. Using customer reviews to go comparison shopping is secondary nature now. Mobile searches for “bank near me” or “best CD account near me” immediately bring a user to an interactive Google Map with recommendations. Ensuring your bank or credit union is on that map and rated highly is essential to not only brand awareness but consideration for new business.

In Rivel Banking Research’s study for The Financial Brand, consumers indicated that they rely on this top-level, Google Review framework 76% of the time when deciding on a new financial institution or banking product. While 37% of Baby Boomers are not using these Google Reviews, more than 70% of the other generations are.

While the ubiquity of Google Reviews is its most important attribute, it’s also flexible for those willing to put in a little time and effort. Consumers can utilize readily available Google Reviews in a few different ways in their research journey, including checking star ratings, seeing locations, reading multiple reviews, looking at the most recent reviews, identifying common themes and evaluating the bank’s responses to complaints.

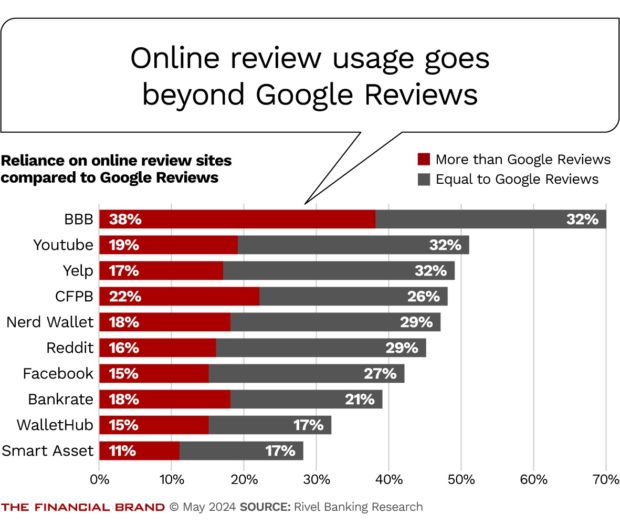

However, not all platforms are relied upon equally. In Rivel’s research, over 40% of consumers have never heard of Bankrate, WalletHub or SmartAsset . Only the Better Business Bureau and YouTube have reliance scores equal to or above Google’s, positioning them to be great secondary resources for banks and credit unions. YouTube is being relied upon for over 50% of Gen Z and Millennials while the BBB is used by over 73% of Gen X and Boomers.

According to research conducted at the Harvard Business School, consumers react most strongly when a review contains more information and is fully detailed. Additionally, for a site like Yelp, a one-star increase was found to lead to a 5-9 % percent increase in revenue. To improve visibility on review results, the key action banks should take is proactively requesting customer reviews. Although dissatisfied customers often voice their complaints on social media platforms, satisfied customers rarely leave positive reviews unless explicitly prompted by the bank to do so.

Your Reputation Among Customers Still Reigns Supreme

While online reviews and individual research play a crucial role in the consumer decision-making process, personal recommendations from trusted sources still carry significant weight, especially when it comes to financial matters. This is evidenced by Rivel’s semi-annual research among banking consumers, in which 48% agreed that it was especially important to get the recommendation of a friend or family member when choosing a new bank.

Interestingly, the younger age groups are even more likely to lean on those they trust — 54% of Millennials and 57% of Gen Z consumers are looking for advice. This trend suggests that, despite their digital nativity, these tech-savvy cohorts still value the opinions and experiences of their inner circles when it comes to matters as consequential as selecting a banking institution, as it’s a task they may not have undertaken before. Moreover, this could be attributed to the long-term implications of such choices.

Read more:

- Online Reviews Are Critical to Bank Marketing: Here’s How to Get More

- Why Wellness Tech Will Redefine the Race for Deposits

Despite the wealth of information available online, many consumers still value the opinions of those closest to them, perceiving their firsthand experiences as more reliable and trustworthy. This highlights the enduring importance of cultivating strong relationships with existing customers, as their satisfaction can directly impact the bank’s ability to attract new clients through personal recommendations. Financial institutions would be wise to prioritize delivering exceptional service and fostering a positive customer experience, as satisfied customers can become powerful advocates, driving growth through their personal networks.

This year, The Financial Brand and Rivel have partnered to bring banking professionals exclusive primary research and analysis on US banking consumers, on a monthly basis. For more information on Rivel Banking Research’s benchmarking, market opportunity highlights and on-hand brand perception insights for your institution, contact: Corey Wrinn, Managing Director, Rivel Banking Research at cwrinn@rivel.com