Digital is Draining Banks’ Emotional Connections with Customers. GenAI May Make Things Worse

Digital transformation has dominated much of the industry's thinking, so much so that it is eroding customer experience ratings issued annually by Forrester. How can banks provide the latest in digital without becoming generic and unsatisfying?

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Forrester’s average customer experience scores for both multichannel banks and direct banks fell for the third year in a row, hitting the lowest levels in years.

Worse, the industry risks driving these measurements lower still if institutions don’t provide greater balance between digitization of financial services and the human factor, according to a senior analyst at Forrester. Further, misguided adoption of generative artificial intelligence could open further chasms between banks and their customers.

Alyson Clarke, principal analyst, says the industry is in some cases working against its own interests.

“Primacy is back on the table,” says Clarke. “But what’s fascinating is that banks say they want primacy, but they don’t want their customers to interact with them. They keep pursuing cost reduction, but they don’t understand what drives customer loyalty.”

Increasingly, many institutions are pushing most customers towards self-service solutions, which are very efficient and good for keeping costs down. But they increase the distance between the bank and its customers.

“I don’t know about you, but I find it just becomes increasingly harder and harder to talk to a human being at your bank when you want to,” says Clarke.

Clarke says too many bankers have begun thinking like ecommerce retailers, equating personal financial services with physical goods.

“Banking’s not Amazon,” says Clarke. “It’s not buying a shirt or a pair of socks. If something’s not right, you want to speak to a person.”

In an interview with The Financial Brand, Clarke discussed the declines in CX scores and the reasons behind them, the risks she sees in adoption of GenAI, and suggestions banks can use to improve CX. The firm’s report, “The U.S. Banking Customer Experience Index Ranking, 2024,” is a subset of a larger study Forrester conducts across over a dozen industry categories.

Roots of Banking Industry’s Three-Year Decline in CX

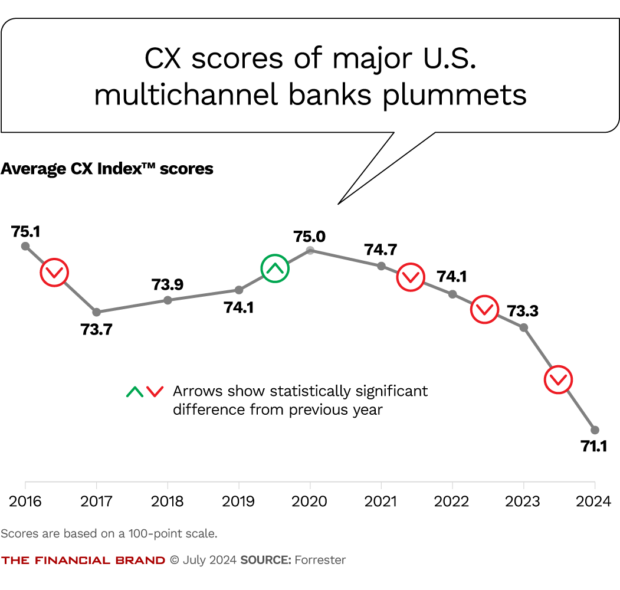

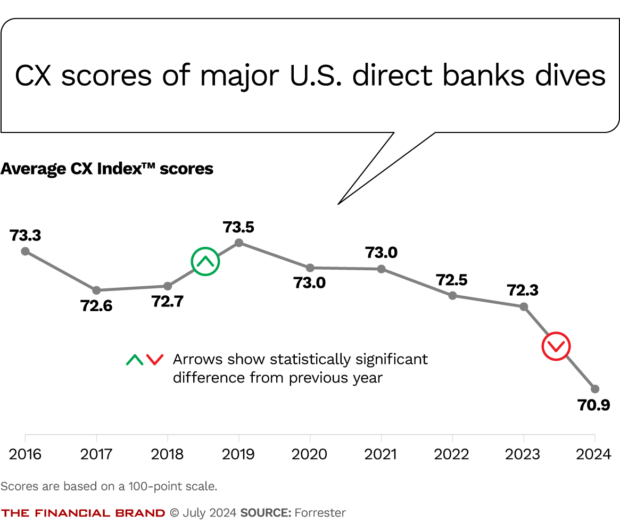

As shown in the charts below, average CX peaked in 2020 among 17 multichannel large banks, and in 2019 among 10 direct banks. No bank saw a significant increase in its score in 2024, and some had very significant drops.

Why the fall? First, says Clarke, customer expectations have been rising. This reflects a trend seen among many industry categories in Forrester’s broader study. In that report, 39% of brands saw significant declines in consumers’ rating of their CX, a level that the firm called “unprecedented.”

The trend was worse among the multichannel banks. Among that group, 53% of the institutions saw significant declines in their rating, as identified by the firm. Among the direct banks, 40% saw significant declines. (Among credit card issuers, not part of the bank report but included in the broad report, 33% of companies saw significant declines.)

Clarke thinks part of the decline can be traced to the relationships between banks and their customers during the height of the pandemic. During that period, there were voluntary forbearance programs even before the government became involved, for example. Institutions engaged in heavy outreach in multiple ways to assure the public that they could help them with their needs. One on one, customers found accommodation from many banks during the worst of the pandemic.

“People were talking to human beings,” says Clarke. “Banks and credit card issuers were being far more considered and empathetic when they were dealing with their customers. There was a feeling of, ‘We’re all in this together’.” Late payments were excused and fees got waived.

But it was a temporary change.

“The practices in place that created positive emotional experiences during the pandemic completely disappeared afterwards,” says Clarke. “And so the industry has been pushed on a downward spiral.”

However, Clarke says the return to normalcy is only one reason for the decline in CX ratings. Key is the increasing digitization of retail banking.

She blames a good deal of the decline in many banks’ ratings and the fall in the averages on how institutions have been implementing digital banking.

Read more: Nine Best Practices As Banks’ Online and App Customer Experiences Converge

Digital Banking Focus Has Reduced the Human Factor

Customer ease and effectiveness is a key part of CX, but it’s not the only part. It can also be very perishable. According to Clarke the shelf life of any “cool” digital service is short. Nowadays the most innovative services rapidly become table stakes. Clarke says she’s watched this happen time and again, and institutions soon get no points from customers for offering those services.

“When something simply works, it doesn’t make the customer any more enamored of the brand or more loyal to it because there’s the expectation that ‘what I can do with one bank, I can do with another’,” says Clarke.

Many digital services are mechanistic, and once the novelty goes, “who gets excited about paying bills?” says Clarke.

The missing ingredient for many of the banks is an appeal to the emotional aspects of banking, according to Clarke.

Among the elements in Forrester’s CX Index scoring template is emotion, defined as “How did interacting with the brand make the customer feel?”

“Bankers are forgetting that that money can be very, very emotional. There are many aspects of banking that are more than moving money around,” says Clarke. “There are a lot of other journeys. Banks are forgetting that they are in the relationship business.”

Some numbers from the study underscore the risk of ignoring emotional factors. Forrester found that among direct bank customers who don’t feel valued — one of multiple emotional facets the firm studied — only 25% intended to stay with that provider. The same percentage held for multi-channel bank customers that don’t feel valued.

Example: Virtual assistants don’t correlate with higher CX rankings by consumers.

The average rating among multichannel banks for 2024 was 71.1 out of 100 points. Six major banks that offer virtual assistants scored below that, including U.S. Bank (Smart Assistant), with 70.6; Truist (Truist Assist), with 70.6; Fifth Third (Jeanie), with 69.6; KeyBank (MyKey), with 69.5; Bank of America (Erica), with 68.6; and Wells Fargo (Fargo), with 68.4. Other banks with virtual assistants, such as Capital One (Eno), with 72.3, and Chase (Chase Digital Assistant), with 71.6, were above average.

Read more: How American Express Keeps Gen Z and Millennials’ App Preferences in Focus

‘Hybrid Banking’ May be a Solution to Lagging CX Ratings

Clarke thinks banks need to stir in more emotional appeal to improve their ratings, and humans are a key additive.

“Hybrid experiences create better CX than digital-only journeys and even physical-only journeys. I call it a triple threat: You get the ease and effectiveness of digitization and you also get the positive emotional element from human interaction.”

— Alyson Clarke, Forrester

Ease and effectiveness are two aspects of the CX index that, with emotion, go into the CX quality part of the firm’s index ratings. Forrester defines “ease” as “How easy was it to work with the brand?” and “effectiveness” as “How effective was the brand at meeting customer needs?”

Branches are part of solving the emotional aspect of CX, according to Clarke, but this is not the only alternative. Direct banks, for example, don’t have branches, typically. But consumers like to be able to reach a real person when they have issues, as noted earlier. This leads into a concern Clarke has about the way the industry may start adopting GenAI.

Read more: How BofA Is Driving to be ‘Local’ in More Markets

Could Poor GenAI Adoption Make Banking’s CX Problem Even Worse?

Clarke also worries that the tendency for digitization to remove the human element from banking will be amplified as institutions move into GenAI.

It’s early days, of course. But Clarke thinks the relentless urge to drive down expenses will tempt bankers to try to use GenAI in place of people who face the public.

“I don’t know that enough of these GenAI models are being trained on empathy and other things that help generate a positive emotional experience for the customer,” says Clarke. “These tools are only as good as what you train them on.

As more institutions introduce GenAI that directly interacts with the public, cool will rule for a while, says Clarke.

But that won’t last so long. “Then it’ll be ‘ugh!’,” she warns.

Case in point: Contact centers. Clarke says many institutions have been beefing up training of center staffers to enhance their empathy and other pro-customer qualities. Unless GenAI is trained to deliver the same behavior, she believes CX ratings will suffer.

Read more: How Banks Can Get Past the AI Hype and Deliver Real Results