Rising Student Loan Delinquencies May Offer Renewed Refi Opportunities for Banks

As a hard-nosed new Department of Education begins collecting on outstanding federal student debt, banks and credit unions must assess impacts on existing consumer portfolios, while also cultivating new lending opportunities.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

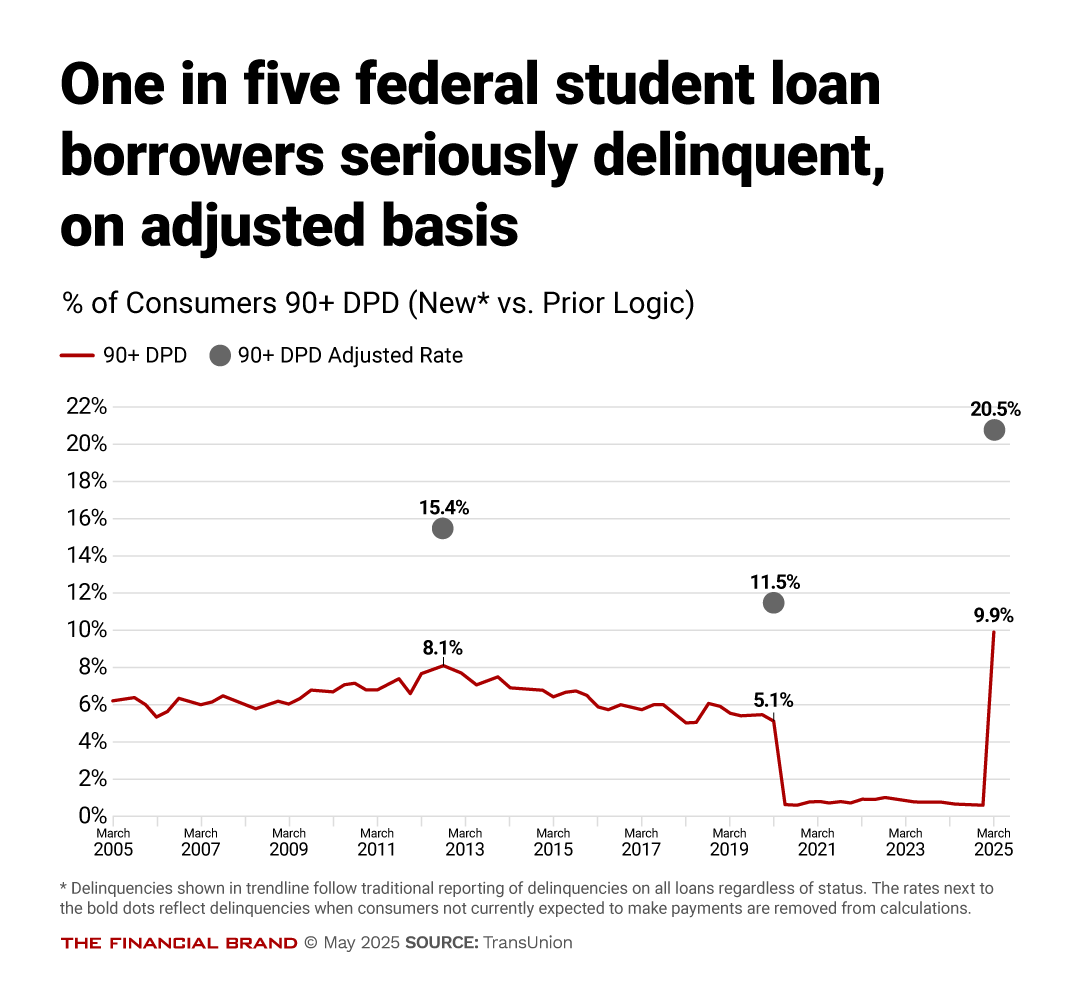

The number of federal student loan borrowers who are at risk of defaulting is surging past levels seen before the pandemic, according to new research from TransUnion. Measured as a percentage of federal student debt that should be in repayment mode, one out of five (20.5%) borrowers are seriously delinquent — 90+ days past due as of February, which is the first stage where processors report federal student loan delinquencies to credit bureaus.

TransUnion contrasts that 20.5% figure with 11.5% of borrowers in serious delinquency in February 2020 — near the start of Covid and the subsequent debt relief programs. The chart below details the trend and contrasts it with how such accounts were tracked previously — as a percentage of all student loan borrowers. The company’s revised approach computes the percentages from a base of borrowers who are in repayment mode.

TransUnion says that it will continue analyzing federal student loan reporting in anticipation that the percentage in serious delinquency could become worse. A precise fix has been challenging due to complex repayment status, according to a company statement.

For affected borrowers the effects of serious delinquency can range from significant drops in their credit scores to delays of years in being able to qualify for mortgages and potentially other consumer credit. This comes at a time when inflation has increased many consumers’ need for more credit. Actual default stays on their credit record for seven years.

For consumer lenders the impact is still coming into focus, both in terms of managing outstanding debt where the borrower has federal student debt in serious delinquency, and deciding whether to grant new credit cards, consumer loans and home loans to those consumers.

Another angle: For some lenders, new growth possibilities are emerging, as people with high student debt will look to refinance their federal loans or to consolidate their outstanding debts overall. Certain banks, credit unions and fintechs do this type of lending and some, in hiatus during federal payment pauses, could return.

What Led Federal Student Lending to Today’s Situation

Federal student loans were subject to pandemic-era forbearance efforts and the Biden administration’s attempted multiple forgiveness efforts. Repayments of federal student debt were to begin in the fall of 2023, but the Biden administration stalled a return to debt collections.

The Department of Education, under the Trump administration, estimates that 42.7 million borrowers owe the government over $1.6 trillion in student debt. The department says that nearly 1.9 million borrowers had not been able to begin repayments because of the Biden-era processing pause.

The department began collection actions on May 5 on federal loans that are in default, which had not been done since March 2020. Collections can begin when a loan hits 270 days past due, and actions can include garnishment of wages and drawing on other federal payments that a debtor may be receiving.

An overriding message from the department is “student and parent borrowers — not taxpayers — must repay their student loans.”

Impacts of Delinquencies on Borrowers and on Consumer Lenders

The Financial Brand asked a selection of large bank and credit union lenders for commentary on the trends identified by TransUnion. Over the course of a workweek, only one made a representative available, a regional bank executive who agreed to speak on condition of only being identified as such. The reason for this reticence: Much remains hazy to lenders about the current picture and the potential ramifications.

“The honest answer is we’re not going to know for a while. The more complicated answer is that there are probably folks at the margin who are going to experience hardship because they’re out of practice in paying,” the regional bank executive says.

The executive adds that “the people we’re worried about are the ones who were strapped already, who needed that [payments] pause.” The hope, the executive says, would be that they have not taken on so much additional debt that they can’t resume the federal loan payments.

TransUnion found that the reported delinquency rate varied tremendously by the borrower’s credit status. As of February, 50.8% of subprime borrowers were in serious delinquency with federal student loans, versus 38.8% in February 2020. Among near prime borrowers 23.3% were in serious delinquency status, versus 9.1% in 2020. While up over 2020, the delinquency rates among prime, prime plus and super prime borrowers were much lower compared to the subprime and near prime groups. (These numbers were computed by the same method described that produced the 20.5% figure cited earlier.)

Those consumers who actually defaulted in January and February 2025 saw significant hits to their credit score — actually, those originally in higher tiers got hit worst. The average score change, in points, for each group:

- Super prime: -175

- Prime plus: -121

- Prime: -99

- Near prime: -64

- Subprime: -42

Federal student loan delinquencies are not reported at earlier stages, such as 30+ or 60+ days past due, as are other forms of consumer credit, points out Charlie Wise, senior vice president, research and consulting at TransUnion, in an interview.

“Once it hits 90 days past due and that delinquency gets reported, it will have an immediate and significant negative impact on the credit score,” says Wise.

So, says Wise, if a super prime borrower had a score of 800, a 175-point drop would drop the borrower to 625, near the bottom of the near prime group — a fall of three tiers. Beyond the immediate impact on credit eligibility, a record of delinquency drags on for years in a consumer’s credit file.

New loans may be problematic already for some federal student loan borrowers now that repayments are underway again, says Wise.

“Repayments will very likely constrain the cashflow of some consumers,” says Wise. “And from what I understand, many lenders have already been factoring in imputed student loan payments in their debt-to-income calculations. So they haven’t been treating it like, ‘Oh, this debt doesn’t exist’.”

Wise puts the current trend in some perspective. Since December 2024, about 4 million people have gone into serious delinquency status with federal student loans. That’s 4 million out of 250 million “credit-active” Americans. (TransUnion believes that number could rise, perhaps to as much as 8 million, according to Wise. A Department of Education news release in April suggested the number could be as high as 10 million later this year.)

“It’s still material, but you’re seeing around 2% of the population impacted so far,” says Wise. “I don’t think that this, in and of itself, is going to cause a massive disruption to consumer credit overall. I don’t think this is like the mortgage crisis of 2007-2008.” However, for the student loan borrowers involved, “this is a very big deal.”

Read more:

Refinancing May Help Borrowers Through the Crunch

Wise suggests that banks with broader relationships with such borrowers may be willing to work with them in obtaining other types of credit. “The lenders don’t want to necessarily turn off the credit spigot to good borrowers,” says Wise. He says lenders who know the customer may decide to treat them differently than if they had missed auto loan or credit card payments.

“It’s completely up to them and their risk committees,” says Wise. “The problem is that we don’t have a lot of history with which to model this out.”

An option that may help some borrowers is refinancing federal student debt, through explicit student loan refinancing or through debt consolidation loans. Some lenders had slowed down that activity, Wise says, because few borrowers wanted to give up the forbearance and payment pauses of the Biden era. Now that payments must be made, and collections on defaults underway, they have an incentive to seek fresh credit.

Regarding the other consumer debts these consumers have, the regional banker says it’s a big leap to think massive charge-offs will occur because they have options. The banker expects to see refinancing and debt consolidation pick up.

“There are definitely options out there where the rate is going to be a little bit higher than what they pay right now, but the amortization is going to be longer,” the lender says. “The extra years will be more valuable to them than the change in the interest rate, in terms of how it changes the size of their payment.”

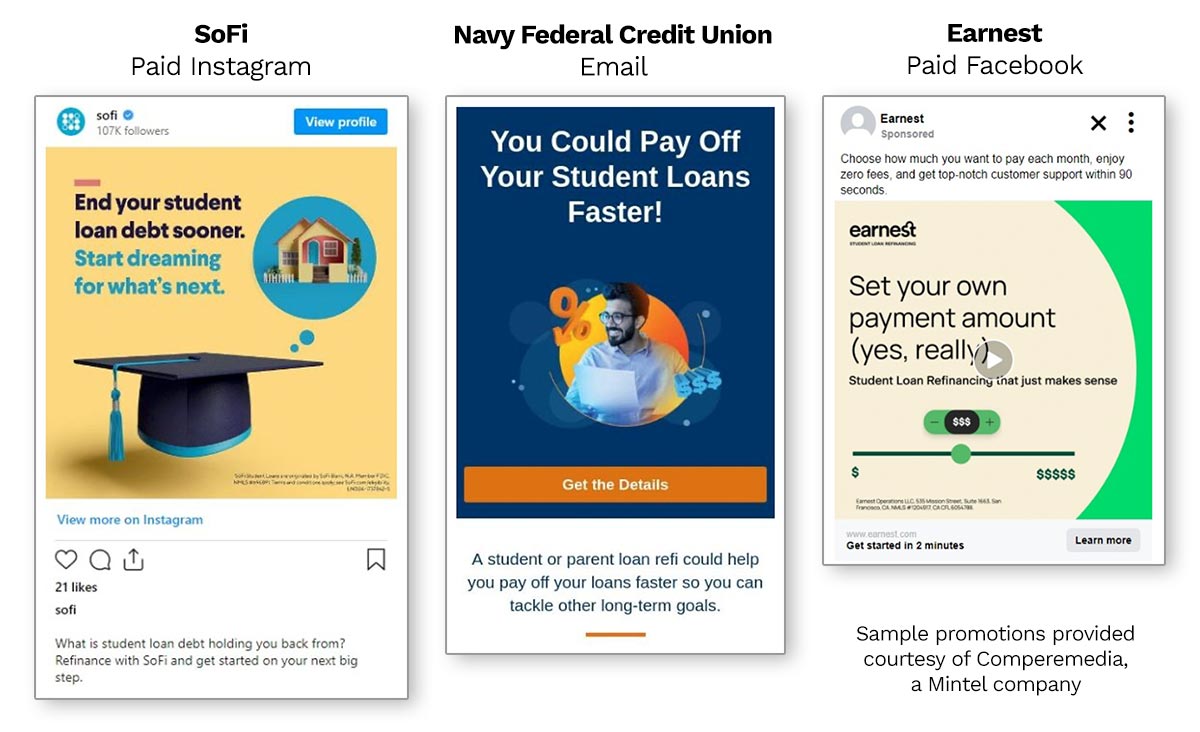

Some lenders have already been increasing their promotion of student loan refinancing opportunities, beginning in 2024, according to an analysis by Marisa Frys, a digital marketing analyst with Comperemedia, a Mintel company. Frys says they were “responding to borrower demand for stability and control in the face of rising rates and policy confusion.”

Two such players who increased spending on refinancing marketing are Earnest and Navient, both fintechs. SoFi, a fintech turned bank, has been a steady player in the student loan business overall, including refinancing. In late April, the company launched a new refinancing solution called Smart Start, targeted to recent graduates. During the first nine months of the loan borrowers only pay interest. The intent is to enable them to apply money that would otherwise go to principal payments towards expenses like relocating to a new city or finding a new job.

SoFi stresses a membership approach to its customers. In a recent earnings briefing, Anthony Noto, CEO, suggested that SoFi could actually step into the space that federal student lending traditionally held. He spoke of it as an opportunity to not only make the initial loans, but to refinance them and capture the borrowers’ other financial relationships for the long term.

The Comperemedia analysis notes that promotions have shifted in tone: “Brands like SoFi and Earnest are framing refinancing as a tool for long-term financial stability. Through app features like credit score tracking, budgeting tools, and debt dashboards, lenders are integrating refinancing into a broader conversation around financial wellness.”

How far refinancing goes and how much other forms of credit for troubled student loan borrowers goes remains to be seen. Jamie Twiss, CEO of Carrington Labs, which provides credit risk analytics and solutions, says lenders will have to evaluate consumers’ individual situations.

Some who are in serious delinquency or actual default may be facing significant economic hardship and won’t be good credit risks, says Twiss. However, he continues, for other borrowers, “student loan default is actually not representative of where they stand today.” He says that some who have had difficulty repaying student debt can be seen as good risks through alternative data sources, such as transaction history, based on their current income levels.

Read more: How Credit Reporting Models Are Failing Modern Lending