Friendship Pays: How to Run a Powerful Referral Campaign for Gen Z Savers

The right mix of product design for your demand deposit accounts and promotion offers for your referral campaign can help drive growth, especially for Gen Z. These consumers are looking for the right saving vehicle, but they may require extra coaxing, recommendations from people they know — and thoughtful connection.

By Kirsten Knoll Longnecker, CMO of Plinqit

Simple Subscribe

Subscribe Now!

As the Federal Reserve begins easing interest rates after a period of inflation-fighting highs, financial institutions continue to compete fiercely for deposits. (A side of margin compression with your pie? Or would you prefer liquidity? It’s a rare vintage.) Unlike the gradual changes following previous recessions, we hear from clients and other bankers how intense the competition over deposit yields is and how complex it is to put together a cohesive deposit acquisition strategy. That’s a challenge for financial institutions. And it’s good news for consumers.

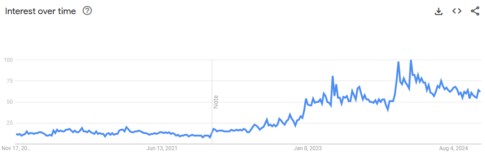

They know it, too. Google Trends data showed that, by the end of 2023, search traffic for “high-yield savings accounts” reached a historical high, with search volumes at least 5X higher than they were at the end of 2021. It brings to mind that Bugs Bunny, Elmer Fudd cartoon where the hunter was taunted by his quarry (yes, I’m older than you are, Google it).

Google Search Traffic for “High-Yield Savings Account” from Nov. 2019 – Nov. 2024

From a tactical perspective, your financial institution needs to keep rates competitive. However, if you want to avoid painful deposit repricing (and more margin compression), you need to understand the behaviors that drive younger generations of savers, such as Gen Z.

Earning the long-term loyalty of younger consumers requires a deep dive into their psychology, preferences, and financial habits. So let’s look at how Gen Z’s propensity for social recommendations can help you grow accounts and deposits.

Peeking Inside the Piggy Bank and the Smartphone

If you’re wondering where Gen Z (born 1997–2012) gets their financial advice, look no further than TikTok — often dubbed FinTok. This vibrant community, boasting more than 4.7 billion views, is a hub for advice trends on managing finances. However, with a potential TikTok ban looming, the way Gen Z accesses financial tips could face a significant shift. According to CreditCards.com, Gen Z is nearly five times as likely as adults ages 41+ to turn to social media for financial advice, raising questions about how they’ll adapt if one of their primary platforms becomes unavailable.

Gen Z is also far more comfortable talking openly about their finances than previous generations, according to a Forbes Advisor survey from 2023.

Pair those insights with the findings from Plinqit’s State of Savings Report and you’ll get a compelling picture of the opportunity for capturing Gen Z’s banking business.

Gen Z presents a ripe opportunity for banks to capture their business. This generation is the most likely to save 20% or more of their household income each month, outpacing other generations in their savings habits. However, they currently favor cash and checking accounts over products like high-yield savings accounts. And they’re the most likely to invest in crypto as a proxy for savings.

When it comes to deciding where to save, Gen Z values personal connections: 37% consider recommendations from friends and family — significantly more than Gen X (26%) and Boomers (20%). Additionally, 30% of Americans, regardless of age, rely on advice from financial advisors for savings decisions. These preferences bring to light a differentiated and exciting opportunity for banks to build strong relationships with Gen Z by offering relevant financial products and leveraging trusted recommendations to meet their needs.

Learn more:

- How Affirm, PayPal and Now Musk’s X Money Will Jockey for Gen Z’s Money in 2025

- 5 Key Demographic Trends for Bank Marketers to Watch in 2025

- The Future of Banking is Personal

It’s tempting to oversimplify the behaviors of a cohort of nearly 70 million people, many of whom haven’t even reached adulthood (see “I’m older than you” in the second paragraph), but this data is still useful and actionable.

Your institution should be tracking the social mechanisms and channels that your target audience is using, especially in light of the potential TikTok ban and where this audience will flock to next. Armed with those insights, you can tailor your marketing efforts to meet their preferences and address key pain points. For example, you might pursue a partnership with a “finfluencer” who can promote a referral offer to their followers.

Referral Programs Generate a Big Bang for Their Buck

If you’ve considered using a referral program at your institution, you’ve probably done some back-of-the-envelope math on customer acquisition costs (CAC). For the financial services industry, the numbers range from $150-780 per account holder. What really matters is that you get clear on your number.

Compare that with the accepted wisdom that it costs 5-25 times less to keep a customer than it does to acquire a new one.

Referral programs offer the best of both. By incentivizing your happy account holders to refer their friends, you stand to increase existing customer satisfaction while attracting new account holders at a nominal, predictable cost.

Ideally, you create an offer that protects your overall CAC and grabs attention. It’s also important to structure the offer so that it protects your institution from “gamers” or people who open an account and do the bare minimum to qualify for the incentive and nothing more. Gamers are the opposite of sticky deposits.

The right mix of product design for your demand deposit accounts and promotion offers for your referral campaign can help drive growth, especially for Gen Z. These consumers are looking for the right saving vehicle, but they may require extra coaxing, recommendations from people they know — and thoughtful connection.

Using High-Yield Savings to Get Gen Z’s Attention

Attracting Gen Z’s deposits will require you to embrace new approaches you might not have anticipated but will ultimately benefit from. These individuals are clearly tech-savvy, as evidenced by their investments in crypto, yet they may not fully grasp the ROI of using a high-yield savings (HYS) account. Only 13% of Gen Z respondents indicated they would be “very likely to open a HYS.”

This signals an opportunity: Even as social platforms like TikTok face potential bans, financial institutions can step in to fill the gap by providing educational content through other channels Gen Z trusts — whether it’s influencers on alternative platforms, friends, or their own branded digital experiences. By helping them understand the value of HYS accounts and giving them reasons to share their experience, you’ll foster a new stream of relationship-based deposits.

Most Americans — 90% — say they are saving for something. What can you do to make sure they’re saving with you?