Can America’s Community Banks Close the Gap Between Their Lofty Ambitions and Limited Resources?

In a new survey conducted by BNY and the Harris Poll, community banking leaders underline the contradictory pressures building in their industry: While their institutions continue to be regarded as trustworthy and even innovative by their customers, banking executives fret that they need to make up ground fast in the products they offer and the digital technology they deploy.

By David Evans, Chief Content Officer at The Financial Brand

Simple Subscribe

Subscribe Now!

The report: 2024 BNY Voice of Community Banks Survey Summary

Source: BNY and the Harris Poll

Executive Summary

The 2024 BNY Voice of Community Banks Survey addresses the critical role of community banks in the U.S. financial ecosystem, while highlighting their challenges and opportunities in an evolving landscape. Key findings underscore the importance of technological innovation, partnerships, and digital transformation in addressing cybersecurity concerns, meeting customer demands, and maintaining competitiveness.

Key Takeaways

- Community banks play a crucial role in the U.S. financial system, providing 30% of commercial real estate loans, over 35% of small business loans, and 70% of agricultural loans.

- Nearly 50% of surveyed banks believe they’re seen as innovative, but 25% feel constrained in offering cutting-edge services.

- 90% of community banks are prepared to initiate digital transformations, yet only 20% consider themselves experts in data analytics.

- 40% of banks plan to incorporate AI and machine learning into their strategic vision to enhance competitiveness and efficiency.

What we liked about this report: It’s a succinct study of the challenges and opportunities faced by leaders at the country’s community banks and provides useful data for peer benchmarking among institutions.

What we didn’t: The survey is based on a very small number of respondents – just 108 executives from among more than 4,400 community banks in the U.S.

The Identity Crisis at Community Banks

The survey reveals an interesting dichotomy in how community banks perceive themselves and how they believe they’re viewed by their communities. Nearly half of the respondents believe they’re seen as innovative within their communities, showcasing their efforts to adapt and evolve. However, about a quarter feel constrained in offering cutting-edge services, highlighting a tension between ambition and capability.

This perception gap underscores an opportunity for community banks to explore collaborations and partnerships. By leveraging external expertise and resources, these banks can enhance their service offerings and technological capabilities, bridging the gap between their aspirations and their current perceived limitations.

Embracing Technological Advancements

In the face of increasing competition and evolving customer expectations, community banks are prioritizing technological innovation as a key strategy for staying relevant and competitive. The survey reveals that about 40% of respondents plan to focus on tech initiatives specifically aimed at enhancing customer satisfaction. This focus includes a strong emphasis on services like instant payments and automated loan processing, reflecting a drive towards efficiency and improved customer experience.

Nearly 30% of banks are looking to leverage technology for risk mitigation and regulatory compliance. This dual focus on customer-facing innovations and back-end improvements demonstrates a holistic approach to technological advancement in the sector.

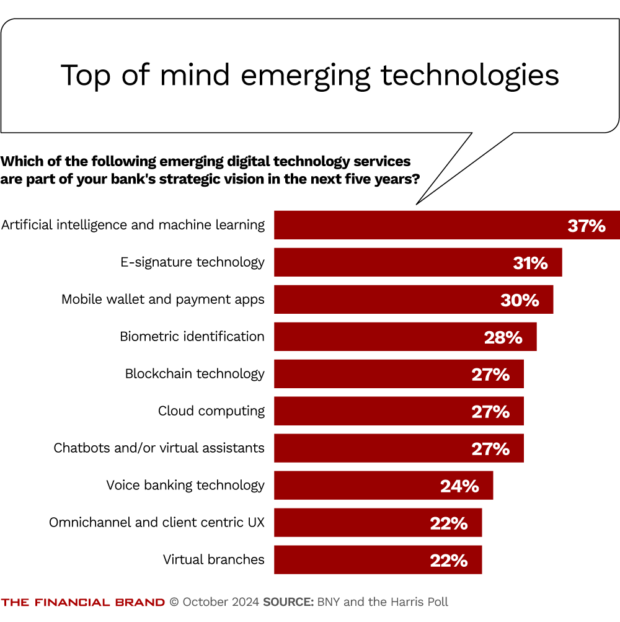

Artificial intelligence (AI) and machine learning are at the forefront of future technology spending for community banks. Almost 40% of banks are incorporating these technologies into their strategic vision for the next five years. This embrace of AI signifies a recognition of its potential to revolutionize various aspects of banking, from customer service to risk assessment and operational efficiency.

Other priority areas for technological investment include:

- E-signature technology: Enhancing convenience and reducing paperwork

- Mobile wallets and payment apps: Meeting the growing demand for digital payment solutions

- Biometric identification: Improving security and streamlining customer authentication

These priorities reflect a drive to meet growing customer expectations for security, convenience, and speed, especially among younger consumers. In fact, two in three respondents indicated that millennials constitute the majority of their retail consumer base, underscoring the importance of digital-first strategies.

Key Challenges and Emerging Strategies

Cybersecurity Emerging as the leading long-term concern, cybersecurity threats underscore the need for robust security measures. The increasing sophistication of cyber attacks, coupled with the potential for significant financial and reputational damage, makes this a top priority for community banks.

Customer acquisition and retention In an increasingly competitive landscape, banks are focusing on strategies to attract new customers and maintain their existing base. This challenge is closely tied to the need for innovative products and services that can differentiate community banks from larger institutions and fintech competitors.

Data management and analytics While 90% of banks feel prepared for digital transformation, less than 20% consider themselves experts in data analytics. This gap indicates a significant skills shortage in an area that’s becoming increasingly crucial for personalized customer service, risk management, and strategic decision-making.

To address these challenges and capitalize on opportunities, community banks are exploring various strategies:

Fintech collaborations: 20% of respondents are considering partnerships with fintech companies to enhance their technological capabilities. These collaborations can provide access to cutting-edge technologies and innovative solutions without the need for extensive in-house development.

Non-fintech partnerships: Nearly 30% are interested in collaborations outside the financial technology sector. These partnerships, which could span industries such as education, retail, or traditional banking, offer opportunities to diversify offerings and meet customer needs more holistically.

Expanded service offerings: There’s significant interest in providing wealth management and treasury services. In fact, 100% of banks looking to expand showed interest in offering wealth management services, while over 95% expressed interest in providing treasury services. This expansion into more sophisticated financial products could help community banks compete more effectively with larger institutions.

Read more:

- Is Your Bank Ready for the Coming Rate Rush?

- Why is Bank Loyalty Dying? Listen to the Folks Around My Dinner Table

- Relationship Fragmentation is Killing Loyalty: How Should Banks Respond?

The Need to Meet New Customer Demands

The survey highlighted specific areas where community banks struggle to meet customer expectations:

- 40% face challenges in providing competitive loan rates. This difficulty could be due to various factors, including higher operational costs or more conservative risk assessments compared to larger institutions.

- Over 35% want to offer better high-yield savings or advanced investment options. This desire reflects an understanding that today’s customers, particularly younger demographics, are seeking more sophisticated financial products and higher returns on their deposits.

These gaps present clear opportunities for community banks to enhance their product offerings. By exploring partnerships, leveraging technology, or developing innovative financial products, community banks can better serve their customers and compete more effectively in the market.

The Role of Government Action

The survey also touches on how government initiatives can support community banks. For instance, the Department of Treasury’s Bank Mentor-Protégé Program provides a unique platform for community banks to collaborate with large commercial financial institutions. This program enables protégés at community banks to receive management and technical assistance, helping them strengthen their balance sheets and better serve their customers.

Similarly, programs like the Advancing Communities Together (ACT) deposit program aim to increase funding for community lending. By making it easier for community development financial institutions (CDFIs) and minority depository institutions (MDIs) to acquire funding from depositors, these initiatives play a crucial role in maintaining appropriate capital and liquidity levels for community banks.

The path forward for community banks will likely involve a delicate balance between maintaining their traditional strengths – personalized service and deep community ties – and adopting the technological and operational innovations necessary to compete in a rapidly evolving financial landscape.

Editor’s note: This article was prepared with AI language software and edited for clarity and accuracy by The Financial Brand editorial team.