Why Most Borrowers Don’t Remember Being Offered Payment Protection, and What It’s Costing Credit Unions

By Nicole Volpe, Contributor at The Financial Brand

Simple Subscribe

Subscribe Now!

As household finances grow increasingly stretched, credit unions are taking a closer look at payment protection insurance: add-on coverage that helps cover or cancel borrowers’ loan payments if they face a qualifying financial hardship, such as job loss or disability.

Such protection is especially relevant in today’s economic environment. Non-housing debt hit a record $5.17 trillion in Q4 2025 (up 2.6% year over year), with serious delinquency rates for credit card and auto loan debt now at 12.7% and 5.2% respectively. While mortgage delinquencies are at low levels, card and auto delinquencies exceed 2008 financial crisis peaks. Meanwhile, roughly 6% of workers took a hardship withdrawal from their 401(k) in 2025, a record high, and a signal that many households have run out of easier options.

Consideration of payment protection tends to rise when economic conditions narrow. More than 80% of consumers in TruStage’s most recent Consumer Lending Preferences Study, which surveys more than 1,000 borrowers, expressed interest in such products, and nearly 70% reported being more open to the coverage than in prior years. More than 9 in 10 said a single unexpected life event — job loss, illness, disability — could derail their ability to repay a loan.

But even against this backdrop, many institutions haven’t seen the payment protection uptake they might have anticipated. More than half of consumers surveyed by TruStage say they don’t remember being offered payment protection on their most recent loan. And that may be because of a phenomenon known as “the recall gap.”

The stakes are high. For credit unions, the recall gap is a missed opportunity both to grow non-interest income and reduce loan portfolio risk. Membership vulnerability is broader than most institutions recognize, according to Lisa Pavelski, who leads product experience in TruStage’s lending business segment.

Financial fragility is prevalent across a much broader slice of membership than most credit unions might assume, Pavelski said. “Consumers are taking on more and more debt, and understanding the implications of the debt-to-income ratio is critical so the financial institution can protect against their own risk and be there for a member when they need it.”

Understanding what drives the recall gap, and what can close it, has become an increasingly pressing question for credit unions as their loan portfolios absorb the stress of a more financially fragile membership.

Invisible Fences (Why the Gap Happens)

Start with borrower fatigue. As much as payment protection is an antidote to anxiety — helping members more confidently meet an important life goal like a car purchase or home improvement — the payment-protection decision comes at a moment of high stress. It’s emotionally loaded, often made in haste, within a single compressed session (online or in person) in which the consumer ultimately inks a $30,000 or $50,000 obligation.

“Unlike getting a carton of milk at the store every week, getting a loan is an infrequent purchase,” Pavelski said. “It comes at a time of very heightened emotions. You’re stressed because you need a new car or your water heater has broken down. It is a high-fatigue event.”

At the same time, the transactions that payment protection rides alongside can be complex: Loan applications are often detailed, requiring the member to provide a range of personal information and data (some of which may not be easily accessible) while also wading through regulatory disclosures and terms and conditions. Product and marketing teams are, of course, continuously looking to reduce friction in such applications. The key takeaway here is that the payment protection point of purchase is not only a stressful place, but a busy place, with information and data coming at the consumer from all directions.

Amid so much stress and distraction, is it any wonder that an offer of ancillary coverage, however relevant, can simply fail to register?

A second driver of the recall gap are lenders’ assumptions about who is likeliest to want payment protection. One instinct lenders often act on is to most actively offer payment protection to members who are most financially vulnerable, based on lower credit scores and income levels. This can happen programmatically, through triggers and prompts in the digital workflow, as well as at the branch: Loan officers, even well-intentioned ones, may make snap judgments about which borrowers are likely to be interested, resulting in offers that are delivered in a cursory way.

“You have a lender who has some amount of confirmation bias,” Pavelski said. “They see a borrower come in and decide, I’m not going to offer this, not knowing that maybe that person has experienced a disability, or someone in their family died and left another family member with a lot of debt.”

The 90% of borrowers who said an unexpected life event would affect their ability to repay a loan spanned consumers at all income levels. Pavelski said: “There are preconceptions that somebody who has a certain credit score or makes six figures wouldn’t benefit from that product, and the data just doesn’t support that.”

Relatedly, the institution’s priorities may lie elsewhere. In many lending environments, the loan officer’s attention, and in some cases compensation, is directed toward closing the loan quickly. Payment protection, which requires a different kind of conversation, can end up deprioritized as a result.

Breaking Through (Remediating the Recall Gap)

For institutions looking to close the payment-protection recall gap, a good first step might be to adopt what Pavelski calls a 100% offer, offering it to every eligible borrower, much as travel insurance is offered when buying a flight. “It’s the best way to ensure a consumer can learn about a product when it’s convenient for them.

Also: Institutions that don’t currently offer payment protection within the online lending flow should consider doing so. Presenting the product as an integrated component of the application experience, rather than in a sidebar conversation, reduces human variability. This is also when members are most receptive to offers — at the time of application — and can make the choice themselves.

Perhaps paradoxically for deep believers in consultative selling, Pavelski said digital offers lead to “more robust packages, more features, and higher-value sales overall than what’s sold in face-to-face channels.” The implication is that when borrowers can review options on their own terms — in the privacy of their own homes, without time pressure — they engage more deliberately and choose more complete coverage.

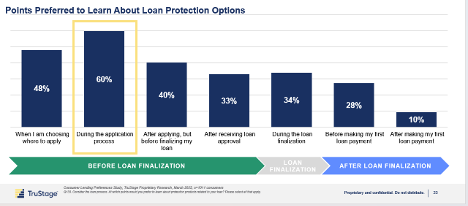

Another way to get ahead of the recall gap is to implement a multi-touch, multi-channel approach. TruStage’s consumer research finds that 74% of borrowers expect more than one opportunity to learn about payment protection across the loan journey. Moreover, their timing preferences vary: some borrowers want to encounter the option early, while researching where to apply; others aren’t ready until closer to closing.

The data is instructive here. Sixty percent of borrowers say they want to receive an offer during the application process itself (the highest-rated moment), but meaningful respondent cohorts also want contact before and after that point. The implication for credit unions is that relying solely on a loan officer conversation at closing leaves a significant portion of interested borrowers unreached.

TruStage, which works with 11 point-of-sale providers, says it reached 2.1 million consumers through digital channels during the application phase last year. A multi-touch approach combining digital presentation with a lender conversation, the company reports, drives a 10 to 15% improvement in conversion rates compared to either channel alone.

Zooming out, it’s helpful to keep credit unions’ traditional member-service focus in mind — the idea that the institution exists to protect members’ financial wellbeing, not just book loans. Especially at a time when potentially more expensive ways to limit the impact of big-ticket purchases (like BNPL and cash advance apps) are on the rise, the combination of credit union financing and payment protection can be a direct expression of that mission. The recall gap is what happens when the delivery mechanism, and an institution’s willingness to innovate, fall short of that standard.