How Digital Shopping Tools Turn Credit Card Apps into Transaction Amplifiers

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Mobile banking apps serve multiple functions, covering the waterfront of consumers’ financial needs. But a new breed of credit card tools like Capital One Shopping exists to facilitate just one thing: buying more stuff.

In fact, a new study by Keynova Group finds that issuers have been adding features to build out capabilities on both ends: boosting consumer purchasing via digital shopping tools on the front end to stimulate usage, and streamlining billing disputes on the backend.

“Issuers are strengthening the mobile credit card experience on all fronts — expanding digital shopping tools that enrich rewards and serve as powerful marketing and retention agents, while adding deepened transaction details that reduce resource-intensive disputes,” says Beth Robertson, managing director. Keynova’s study examines the offerings of ten major credit card issuers.

Need to Know:

- Increasing sales is ultimately what the credit card business is all about, for both merchants and card issuers. Programs to link consumers with deals are popular and proliferating.

- These credit card tools can tie promotion and usage on the front end and more streamlined back-end functions, such as dispute management.

- Reducing pain points is an increasing focus as more and more consumers do their digital shopping via mobile devices.

Digital Shopping Tools Usher in Card Volume

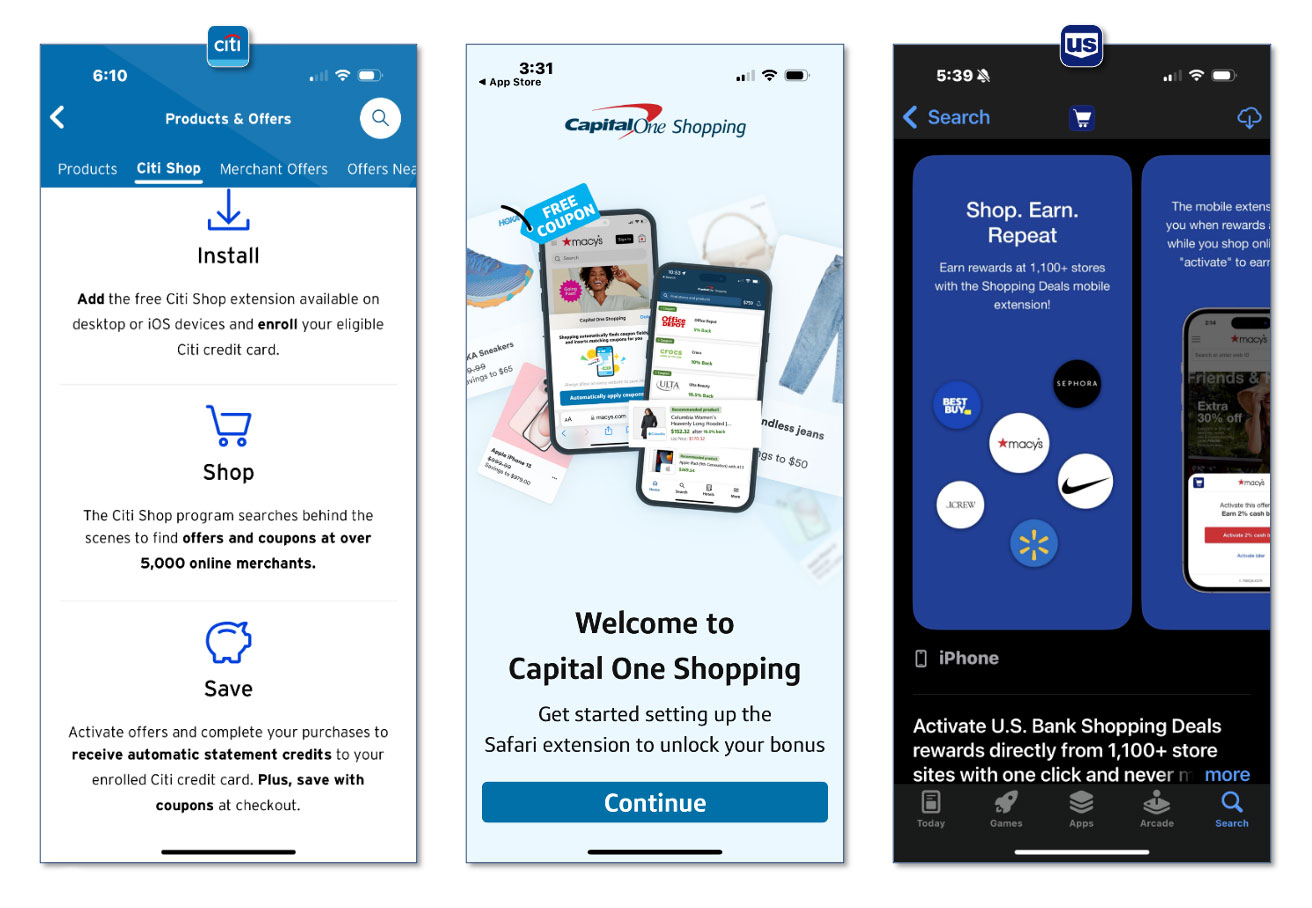

In Keynova’s report, the fourth quarter 2025 Mobile Credit Card Scorecard, Robertson traces how digital shopping tools came on the scene. Initially, the tools sprouted as standalone programs, such as Rakuten Rewards, PayPal Honey, and Wikibuy. Capital One acquired the latter in 2018 and turned it into Capital One Shopping. The report notes that these platforms, and others like them, really began to catch on during the pandemic.

Card issuers offer multiple types of programs tying in with merchants’ products and services. Keynova looked at digital browser extensions and mobile apps for automatically serving coupons and discounts when consumers shop digitally.

Once a consumer enrolls and authorizes the service’s ability to monitor shopping patterns and to seek out deals in the background, there’s no need for the shopper to find specific opportunities on their own.

“Other than installing the extension, once you go out to a site to shop, the extension generally lets you know if there is an opportunity to either use a code to get rewards or to activate particular rewards,” says Robertson.

Pile it on! These programs often offer “stackable rewards,” that is, beyond the savings identified, they also allow cardholders to retain cashback or other benefits for using their card.

By contrast, another type of program, not covered extensively in the report, are merchant offers, typically presented on issuers’ digital platforms, like Chase Offers. Cardholders must review the offerings and specifically sign up for each one they want. Generally these activations only last 30 days, according to Robertson, and must be renewed if the cardholder wants to continue getting the savings. Four out of five of the large issuers reviewed by Keynova offer such programs.

Going for “front of mind” via cards. Capital One Shopping, which works with more than 100,000 merchants, is not restricted to the bank’s customers or cardholders. The bank earns commissions from merchants when purchases occur. Robertson points out that the bank also earns goodwill and exposure by running the service. Some shopping information leads to preapproved card offers.

“Capital One’s brand continues to pop up in front of you,” says Robertson.

By contrast, two other banks that offer digital shopping tie the services to usage of their credit card. Citibank has its Citi Shop for qualifying cardholders, who must register their card with the service in order to obtain breaks from more than 5,000 merchants. U.S. Bank has been offering U.S. Bank Shopping Deals, with a base of over 1,000 merchants. The report notes that in addition to finding savings the function offers shoppers some opportunities to earn additional rewards, such as points or cashback.

Graphics courtesy of Keynova Group.

U.S. Bank has decided to consolidate Shopping Deals into the bank’s Cashback Deals program, which is where the institution has seen the greatest demand and engagement from its cardholders, according to a spokesperson. The shift, part of a streamlining of rewards programs, is to take place at the end of January. Features will include the ability to “favorite” merchants and implementation of single-click activation.

Read more:

- 5 Critical Payments Challenges for Banks in 2026. Keep Your Eye on PayPal

- How Credit Builder Cards Became a Loyalty Play

- Credit Card Satisfaction Stalls, Thanks to Surcharges, Debt, Complicated Rewards

Enhanced Transaction Records Can Drive Down Disputes

Who hasn’t had a mystery charge surface on their credit card statement? While some may be the result of fraud, often the purchaser has simply forgotten the transaction — or didn’t know that a joint cardholder made the purchase.

In its report, Keynova notes that a few years bank, a handful of issuers added functionality to their apps to enable cardholders to shoot copies of physical receipts and digitally associate them with the corresponding card transactions.

A good idea … in principle.“The concept was designed both to facilitate expense reporting for business users and to reduce the number of transaction disputes,” according to the report. But customers found the two-step process clunky.

Disputes are a time-consuming, costly process for issuers and merchants, and, for that matter, card users. Often unrecognized transactions are completely legitimate, just forgotten, or the result of joint cardholders losing track of each other’s buying.

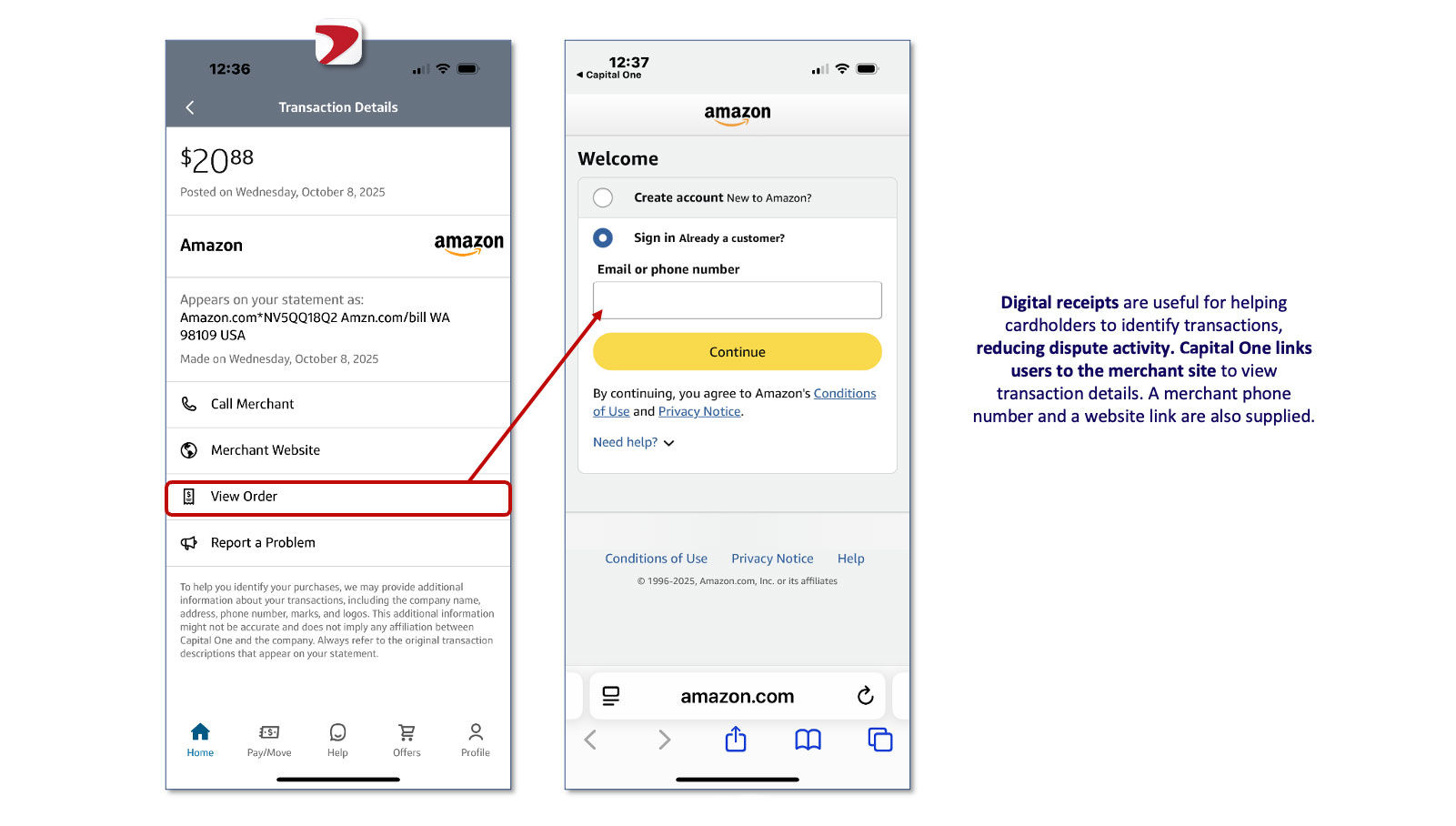

Now more than half of the issuers studied by Keynova have adapted the concept digitally. They provide digital receipts that tap merchant transaction information to pinpoint what charges were for and where they were incurred.

Taking it further. Less than half of those issuers offering such assistance offer the ability to distinguish between users on joint card accounts. “This is another useful capability that can assist cardholders in identifying transactions to reduce potential dispute activity,” the report says.

When there really is an issue… Nine of the ten issuers now offer users the option of filing disputes through their mobile device, with transaction details automatically filled in. And two-thirds of the issuers enable users to track the status of disputes on their devices.

Robertson notes that other helpful practices are being adopted as well. For example, most offer a detailed merchant address on transactions, and also a phone number. Some provide the merchant location on a mapping function, which can help narrow down a mental search from a busy week of charging.

Capital One takes things further by sending the querying user to the merchant’s own site, where possible, so they can log in and view transaction details.

Graphics courtesy of Keynova Group.

“These features can be really helpful to jog your memory and can help when reaching out to the merchant first,” says Robertson. Typically, when cardholders complain to the issuer, the first thing they’re asked is if they’ve spoken to the merchant, she points out.

Citing separate research by the firm, Robertson adds that this practice of providing purchase details is growing among debit card issuers as well. Currently only Bank of America provides actual digital receipts, according to a Keynova report as of the third quarter of 2025, but the firm anticipates more to follow.

Read next: Why Banks Are Rethinking Human Review in Dispute Operations