Citizens Bank Is Out to Dissolve Account ‘Stickiness’ – And Steal Your Customers

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Consumers often stick with a bank or credit union, not because they love their provider, but because it’s just too much work to unhook their life from their checking account and move everything elsewhere.

- But what if moving a bank account and reestablishing all those financial relationships was as easy as a few clicks on an app?

- Citizens Bank thinks its new switching service can be the solvent for stickiness, allowing customers to move their entire financial life to Citizens in just a few minutes. Right now, it is the only Mastercard partner using the technology.

For a long time, retail banks seeking primacy enjoyed the security of “stickiness” that only got stronger as more and more outside relationships got tied to customers’ checking accounts.

The convenience of having these accounts serve as “life hubs” for automated deposits and automated payments, as well as quick transactions in and out via other, connected financial apps, made a convincing case for staying put. Inertia played a role, of course, but also the effort required to change all those connections created over the years.

Now, Citizens Bank has introduced new services that may be the solvent that unsticks the glue that some retail bankers have come to rely on.

“I don’t just want the account that you’ve got a couple of bucks in, and that you think about once in a while,” says Chris Powell, head of deposits and customer engagement at Citizens. “I want to be your primary bank.”

To Powell, that means steady inflow, whether the customer has a single direct deposit coming in twice a month or is a gig worker with 30 direct deposits in that period. “I want the important life transactions to be running through our account.”

Citizens Expedites Payment Switching, Direct Deposit Switching

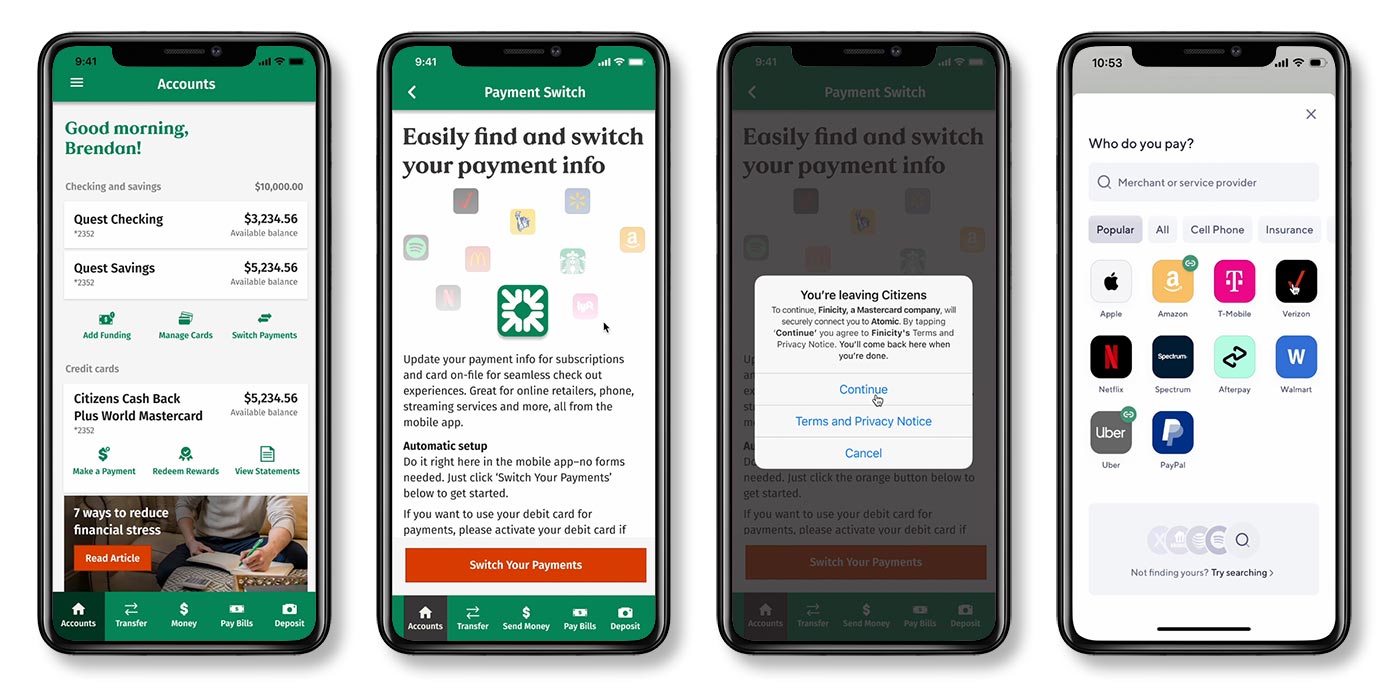

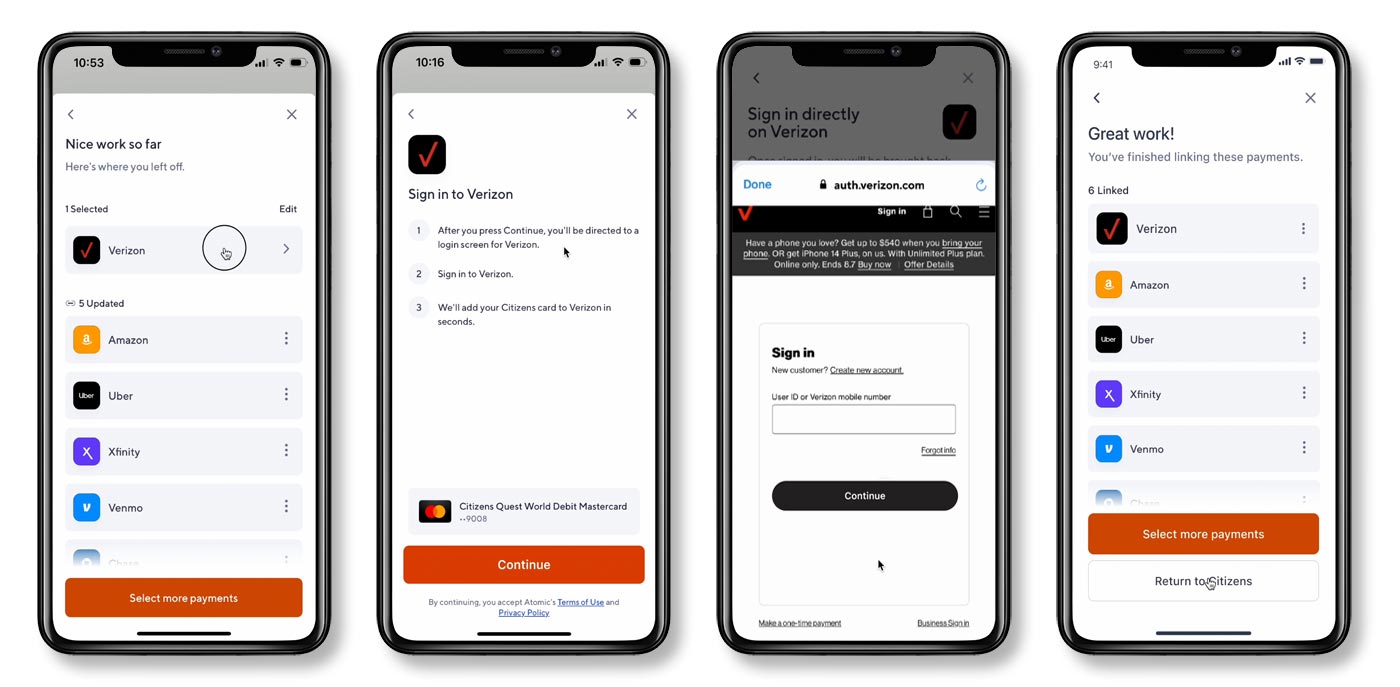

The first new functionality, based in the bank’s mobile app, enables the Citizens customer to easily update saved payment methods stored with many popular billers, online retailers and subscription-based goods and services. At the outset, over 70 organizations are tied in, including Amazon, Netflix, Verizon, Lyft and Spotify.

The technology, provided through Mastercard’s Finicity subsidiary, not only enables the consumer to connect their Citizens account to the merchant, but behind the scenes it also disconnects the customers’ previous payment arrangement. Each change can be completed in under a minute via the bank’s app.

The screens below illustrate how this process works. (You can also visit an emulation of the process on Citizens’ website.) The feature authenticates the switcher through facial identity and a one-time passcode.

Citizens says the service will automatically update billers should the accountholder’s debit card be lost or stolen and then replaced.

“Doing all of this without the friction of having to remember and type in 20 different usernames and 20 different passwords is really compelling,” says Powell.

The second new functionality, also in the bank’s app, addresses direct deposit. It enables accountholders to quickly update where their direct deposits go rather than filing manual paperwork. This is based on direct integration with major payroll companies, making it unnecessary to go through employers’ human resources departments.

The two services rely on two open banking solutions provided by Mastercard working in conjunction with Atomic: Bill Pay Switch and Deposit Switch. Mastercard unveiled these services in June 2024, promoting them as relief from “tedious tasks like rerouting direct deposits and paying bills.”

Mastercard also noted at the time that Gen Z often prefers debit cards for paying everyday costs, all of which run through checking. A Mastercard spokesperson confirmed that Citizens Bank is its first institution to make both services live.

Powell says the bank is already looking at add-ons to the basic switching service. For example, right now everything is deposit-oriented, but he thinks some consumer will want to add in credit cards for various merchants. That could be for budgeting purposes or perhaps to obtain card rewards. In time he sees such discussions becoming part of the bank’s onboarding process.

Read more about Citizens Bank:

- How Citizens Bank Beats the Giants with Style, Smarts and Soul

- Citizens Bank Insulates Against Economic Turmoil With Focus on Upmarket Consumers

- Citizens Bank Pushes Digital Services Deeper for Better Customer Engagement

Overcoming Inertia, But Not Settling for Checking Accounts

Asked if this wasn’t a lubricant for consumer inertia, Powell says he thinks this is where open banking is headed, eliminating friction.

“If you think about real open market competition, we shouldn’t be thrilled that we’ve got customers who are staying with us because it’s so hard to leave. We should be winning on the strength of value,” says Powell. Value includes advice and other assistance to increase financial health and creative solutions, he says.

Powell sees the switching services as a way for Citizens to win good relationships and demonstrate value. He adds that internally the focus is to “aspire to be America’s easiest bank to switch to.” Whether that would become an actual marketing tagline or theme he couldn’t say.

More specifically, he says, the bank sees the switching service as a key component to establishing new relationships.

“A customer doesn’t want to open a checking account. A customer wants to switch their banking,” he says. Powell believes banks need to give them integrated ways to do that, rather than a long series of tasks.

He says the bank is trying to bring the same functionality to the in-branch experience, to help prospects quickly move their business to Citizens. Critical to that strategy, he says, is building in ways to re-engage, because prospects don’t always pull the trigger on a whole new banking relationship right away.

Citizens doesn’t have an exclusive on the technology, which means others will eventually take it up or avail themselves of similar approaches. Powell says “I’m a product guy, through and through,” but acknowledges that simply pitting one product against another would be a losing battle over time.

“Once it becomes table stakes, that really puts the onus on the bankers to improve the quality of advice and customer interactions to drive long-term value,” says Powell.

In the meantime, he adds, I think we are carving out a really good niche for ourselves.” Simply being the consumer’s checking bank is only a beginning, he says. That relationship needs to be a spearhead for selling more products and services, once the bank demonstrates it handles the basics well.

For some time Citizens has been pursuing a strategy of courting upmarket customers, who are more likely to be able to avail themselves of a broader selection of products, from cards to mortgages and home equity loans to student loan refis.

Noting the bank’s push into New York and New Jersey, Powell says that many “have heavy incomes but also heavily complex financial lives.” Demonstrating how Citizens can simplify the basics is an entrée, not a conclusion.

Read more: Banks Lost $3 Trillion to Fintechs in the Last Five Years. Blame the Primacy Myth