Banking Apps Are Trapped in Digital Mediocrity, and It Shows

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Major bank and credit card issuers keep polishing their mobile apps and online banking functions. But as they get better, they look and feel more and more like each other, according to J.D. Power.

- Virtual assistants have been looked to as the next step up. But consumers are getting used to more versatile GenAI assistants like ChatGPT and Copilot.

- GenAI could ramp up virtual assistants’ capabilities, but banks worry about risks like hallucinations.

Banking’s digital channels — both mobile apps and online banking — are suffering from two linked syndromes, according to new analysis from J.D. Power.

First, overall satisfaction ratings in the firm’s recent studies show little change overall, a trend that’s been steady over several years.

“More than that, the differences between the ratings of top performers and bottom performers are shrinking,” according to Sean Gelles, senior director of banking and payments intelligence. “We are not seeing huge spikes in satisfaction, on average, and what we are seeing, from a satisfaction perspective, is that bank digital experiences are starting to look more and more similar in terms of what they deliver.”

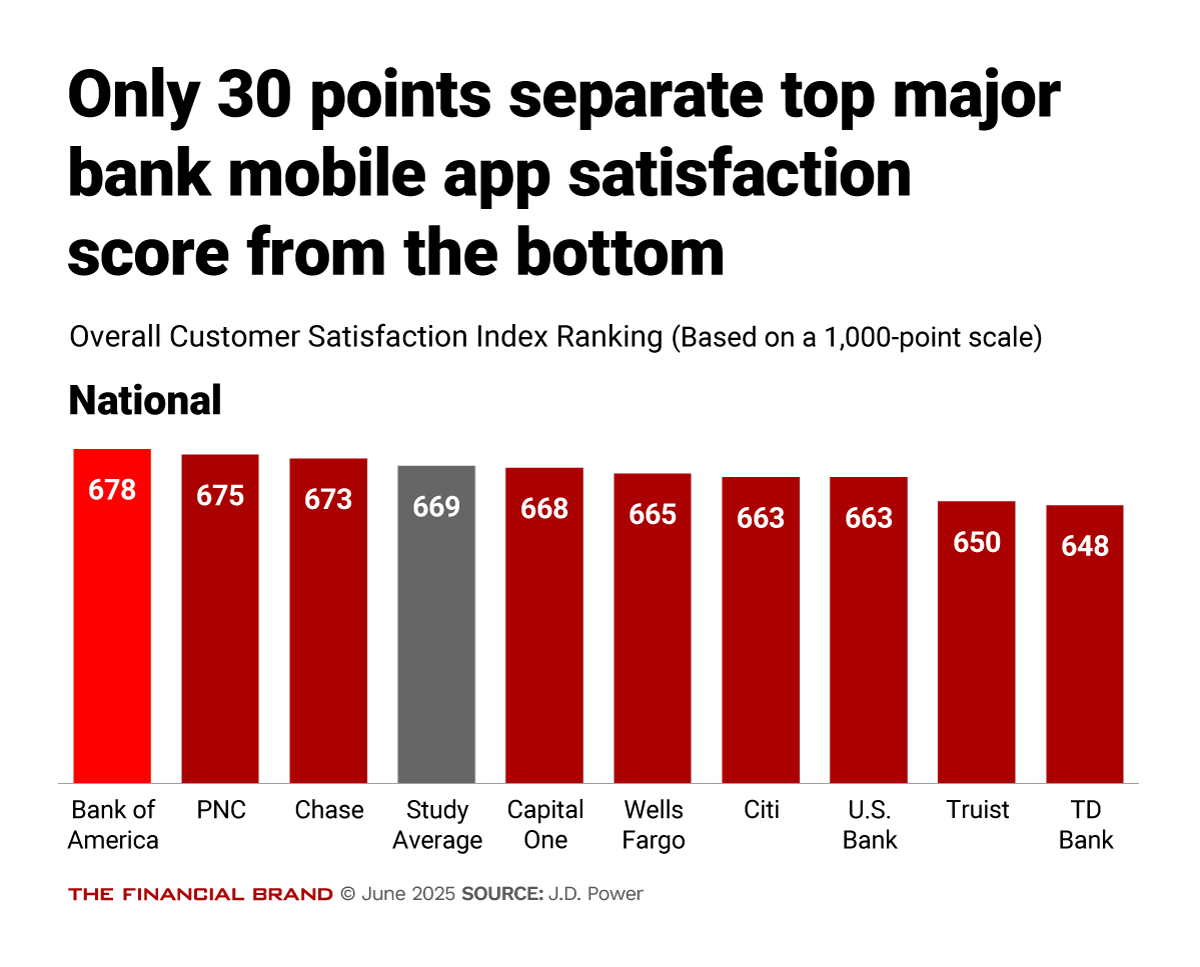

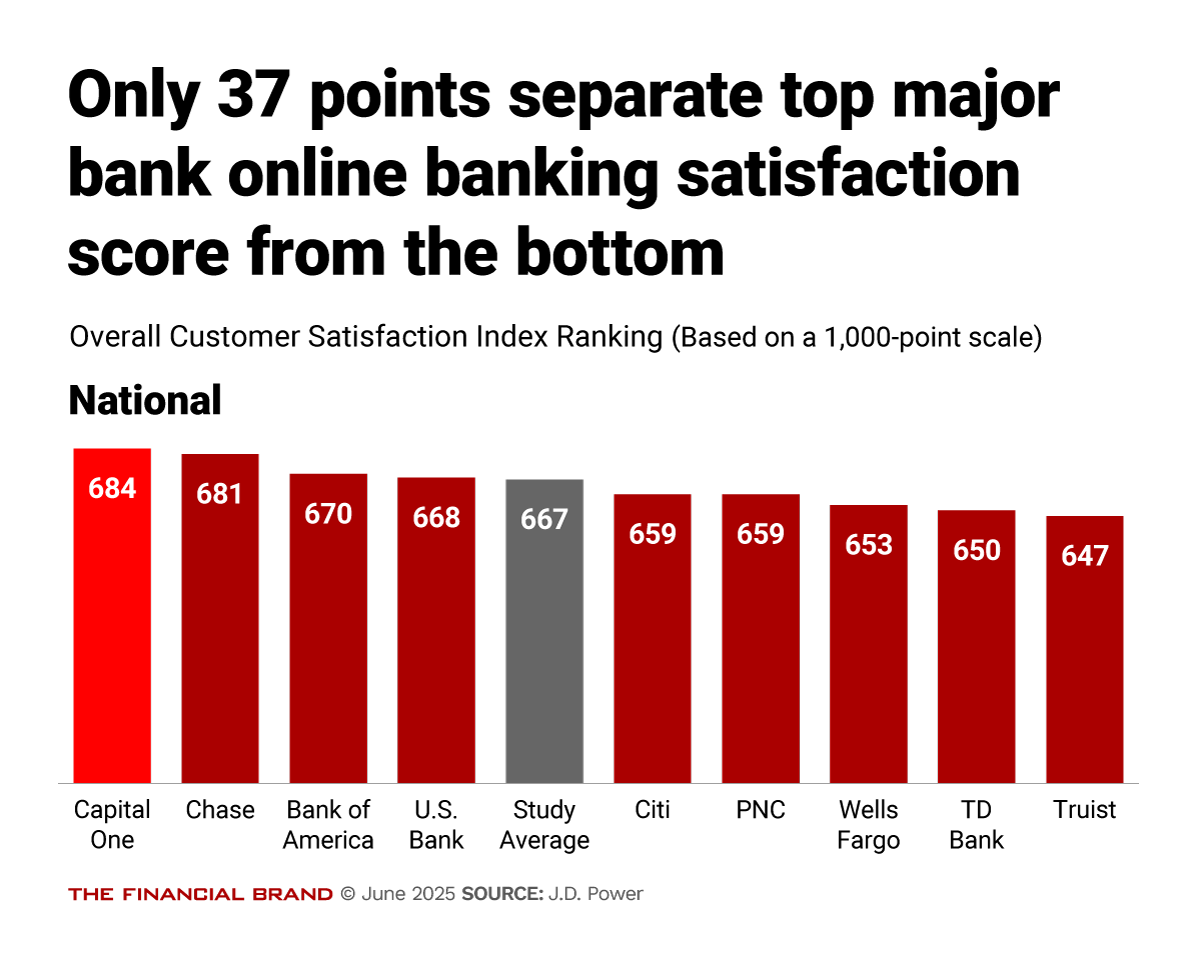

As the following two charts show, the gap between the top and bottom performers in satisfaction for national bank mobile apps and online banking has shrunk to 30 points and 37 points, respectively. (All of the J.D. Power satisfaction rating reported here conform to a 1,000-point scale.)

The difference between the top and bottom performers in national bank mobile apps went from 87 points in 2023 to 59 in 2024 to the 30 in 2025 shown in the chart above.

“Right now, we’re in a situation of parity,” says Gelles. This creates opportunities for institutions and issuers willing to buck homogeneity, he believes.

The firm is seeing similar trends in its studies of regional banks’ mobile apps and in its analysis of their online banking efforts. For mobile apps, for example, the differences were 121 in 2023, 63 in 2024 and 38 in 2025.

Though not as pronounced, the trend has emerged in credit card issuers’ mobile apps and online access as well. For credit card apps, for example, over the same periods, the differences were 133, 120 and 93.

The second syndrome is that virtual assistants aren’t providing the boost in customer satisfaction that they once did, according to analysis across the firm’s banking and credit card mobile app studies.

In fact, Gelles says there’s been a bit of slippage.

He provided The Financial Brand with averages across 2024 and 2025 mobile app studies. The average percentage of responding consumers who used a virtual assistant actually fell from 33% to 30%. The average overall satisfaction among consumers who used a virtual assistant also fell, from 691 to 687.

Now, those declines are modest, but Gelles says the bigger picture must be considered.

“Given the investments in this space, we would not expect to see declines among users who have engaged with this technology,” he explains.

Gelles believes the reason behind these declines goes beyond the virtual assistants themselves, which major institutions have been developing continuously. The challenge for the industry is that its virtual assistants are being compared to GenAI tools.

“Virtual assistants are less of a satisfaction driver and it’s because the virtual assistants in most of these apps and websites are not on par with what consumers now expect,” says Gelles.

He points to OpenAI’s ChatGPT, Microsoft Copilot, Meta AI and other GenAI tools.

These are widely available AI assistants that many consumers are increasingly familiar with, he says, and the virtual assistants that banks and card issuers provide don’t compare favorably.

“Your average consumer has probably used at least two different AI chat agents, ChatGPT and something else,” says Gelles. He believes things are getting to the point where virtual assistants that were good — or good enough — in the past are not as much of a differentiator anymore.

He blames the faltering figures on virtual assistants’ limited conversational capabilities and relatively narrow functionality, though the firm acknowledges that some institutions are slowly moving to beef things up.

Gelles, who worked at American Express before joining J.D. Power, thinks this reflects financial companies’ hesitancy in adding GenAI to their digital experiences.

“They tend to be very cautious about innovating in this regard,” says Gelles, “and there is reason to be cautious.” GenAI hallucinations may be excused by people when they are doing basic background research. Gelles says he’s had that experience himself and pointed it out to the AI and received apologies.

But it’s another matter to let hallucinations impact discussions about people’s money, especially if what they wanted was sound financial advice.

“But we’re going to continue to see the trends we’re seeing now until someone comes up with new ways to deliver banking services with the technology that’s available now,” says Gelles.

Read more: U.S. Bank’s Dominic Venturo: Impactful Innovation Means Thinking Ahead of Today’s Emerging Tech

ChatGPT Versus the Human Element

In a March article on this website, Jorge Camargo, managing director, mobile app, online banking & Erica AI executive at Bank of America, explained how the Erica virtual assistant is a blend of natural language processing, machine learning, and continuous input by a dedicated team of humans — but not GenAI or agentic AI.

At the time, Camargo said that someday both could become part of Erica. But he noted that while the bank is evaluating possibilities for both AI types throughout its operations, for the time being there will always be a person between any GenAI involvement and what the public experiences.

Camargo also said that the bank wants Erica answers to conform to BofA policies and practices — and to produce trustworthy answers. The bank sees human input and oversight as a differentiating factor. In fact, in the article Camargo said a key element of the Erica experience is the “off-ramp” — the opportunity to shift mid-query to a human banker.

There’s no human that ChatGPT and other GenAI can default to if they aren’t delivering what the user wants.

At Truist, the bank’s virtual assistant, Truist Assist, launched in late 2022, was rolled out to mobile customers earlier this year.

“We’re averaging more than 450,000 client conversations per month with an 82% channel containment rate. This means the majority of our clients are getting their everyday banking questions answered within Trust Assist without the need to speak to a teammate,” says Sherry Graziano, head of digital, client experience, and marketing. (The Financial Brand reached out to multiple national banks that offer a virtual assistant.)

Live human help is available to those who need it, and Graziano believes that this is a differentiating factor for Truist.

Where Could GenAI Take Virtual Assistants?

J.D. Power’s analysis found that customer satisfaction with apps and sites has been improving, but chiefly because of increased speed and other technical enhancements. Gelles says institutions have to begin assessing what’s missing from their digital experiences in general, as well as how GenAI could potentially improve their offerings.

Overall, ease of use of digital channels remains a sticking point for customer satisfaction, according to Gelles. He says the average across the studies for users saying that they find the tools easy to use is only 28%.

“There are some brands that are getting a better score on that factor,” says Gelles, “but that’s the average. That’s low.”

He thinks there’s some low-hanging fruit, beyond expecting virtual assistants to guide users to functions they need.

Read more:

Using virtual assistants to personalize what’s put in front of users is key, in Gelles’ view. Amazon has been doing this for many years, he says, and that is simply putting more of what people have already bought, or related items, on their pages. (In the interview Camargo noted that 60% of Erica traffic is outbound now, with the virtual assistant reaching out to account holders to do things like alerting them to unusual activity.)

In a financial context, instead of presenting static choices, Gelles says, financial players could personalize things from the get-go, drawing on what services the consumer has tapped before.

This would be akin to walking into the corner bar and not only being greeted by name by the bartender, but asked, “The usual?”

“Customizing the user interface using GenAI can make it ‘Sean-friendly’,” he says, “predicting what I’m looking for and making those things more available to me.”

Read more: Personalization and Accessibility: Are Banking Apps Doing Enough?