Consumer Credit Boomed in 2025. Why 2026 Shows Few Signs of Slowing Down

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Lenders will see continuing growth in most major consumer credit areas in 2026, on the heels of a strong 2025. Growth will come in the context of the continued normalization of consumer credit demand broadly. There will be some significant credit areas that could be opportunities.

So says TransUnion, which projects continuing momentum in originations of mortgage loans, unsecured personal loans, and credit card accounts. The only area where the company expects annual originations to tick down is auto lending. (For more, see our deep dive.)

Need to Know:

- Mortgages are projected to continue a rebound in origination volume seen over 2025 and 2024. TransUnion expects purchase mortgage orginations to rise 4% and refinance originations to rise 4.2%.

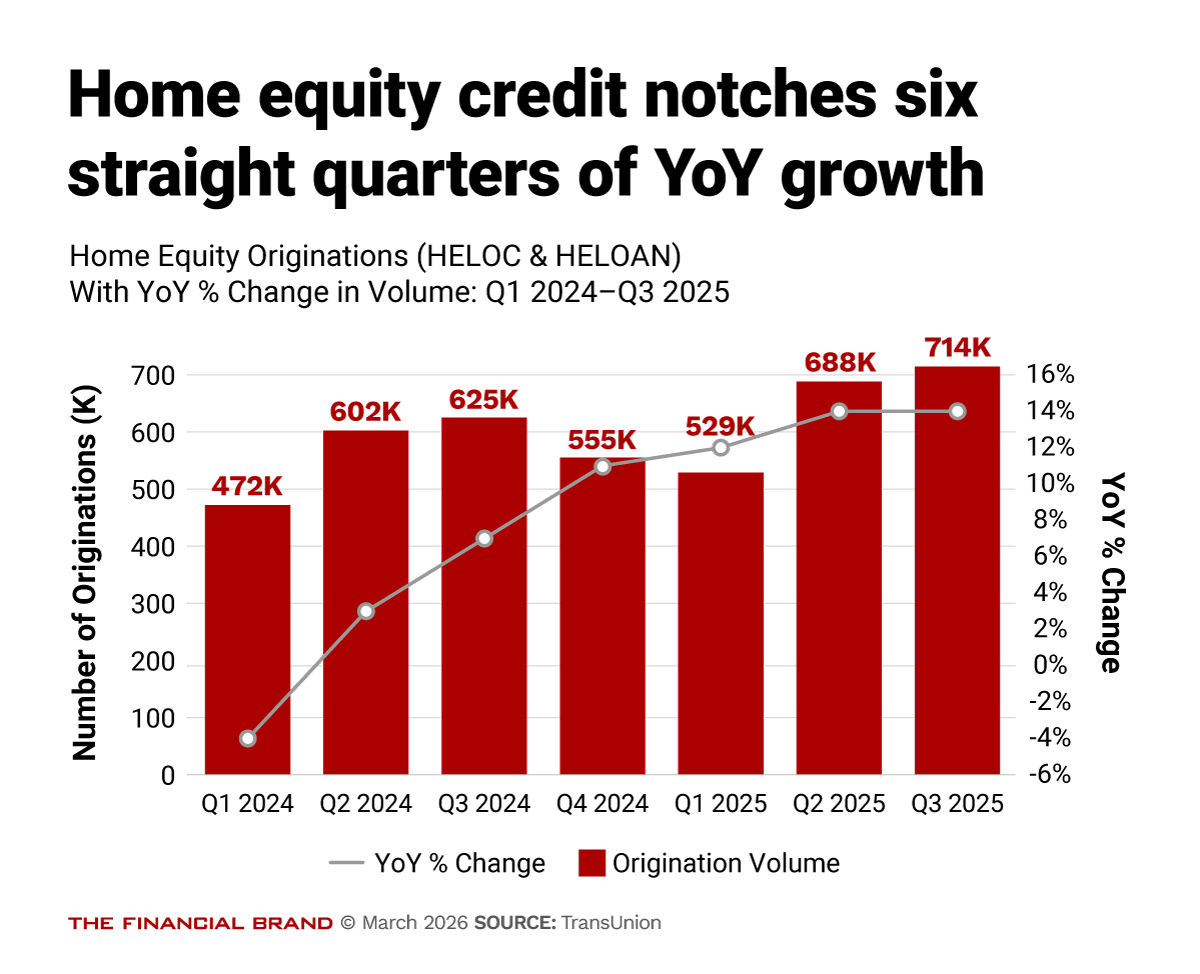

- Home equity lending is also poised for continuing growth, having hit the sixth consecutive quarter of year-over-year growth in originations.

- Unsecured personal loan originations are projected to grow by 5.7%, coming off two years of double-digit growth in originations.

- Credit card originations are projected to rise by 2%, after near-record growth in 2025 of 9%.

TransUnion notes that credit demand “remains strong across risk tiers and will likely strengthen further if interest rates fall more than expected in coming quarters.” Thus far, it reports, lenders have been taking a “disciplined approach” to opportunities to grow. (After the company’s announcement, the national unemployment rate ticked up in the wake of the loss of 92,000 jobs in February.)

Three opportunities to grow originations based on the study:

1. Home Equity Credit

By the end of 2025 nearly all homeowners with mortgages with rates below 5% continued to hang onto their low-rate loans and their homes, according to ICE Mortgage Monitor Report. This is called the “lock-in effect.” As home prices have cooled somewhat, the level of home equity has flattened out, the report says.

However, ICE Mortgage Monitor points out that going into 2026, homeowners have $16.9 trillion in home equity. Of that, just shy of $11 trillion is considered “tappable,” that is, available to secure either home equity loans, home equity lines of credit, or cash-out refinancings. TransUnion pegs the level of tappable home equity at an even higher level, based on a different method.

“Homeowners continue to sit on some of the strongest equity cushions on record, supporting financial resilience, limiting credit risk, and giving borrowers room for equity extraction,” the ICE report says.

(By contrast, “negative equity,” where borrowers owe more than their home is worth, picked up in 2025, heightened in some markets but considered modest at the national level.)

TransUnion reports that home-equity credit originations, including both HE loans and HELOCs, increased 14.3% year-over-year, in the third quarter of 2025. HELOCs rose even more, by 15.8% year-over-year, and HE loans rose 12.9% year-over-year. Such originations are reported one quarter in arrears.

“There are still opportunities, given that we’re still operating at higher interest rates,” says TransUnion’s Atsuko Watanabe, senior director, research and consulting. “Once interest rates decline, there will be pent-up demand that will generate additional volume of home equity originations.”

Marketing tip: The company indicates that the largest HELOC borrower groups are Gen Xers and Baby Boomers. The strongest growth in HE loans has been seen among Gen Z.

Read more: Success in Home Equity Hinges on Quality (and Fast) Customer Experience

2. Unsecured Personal Loans

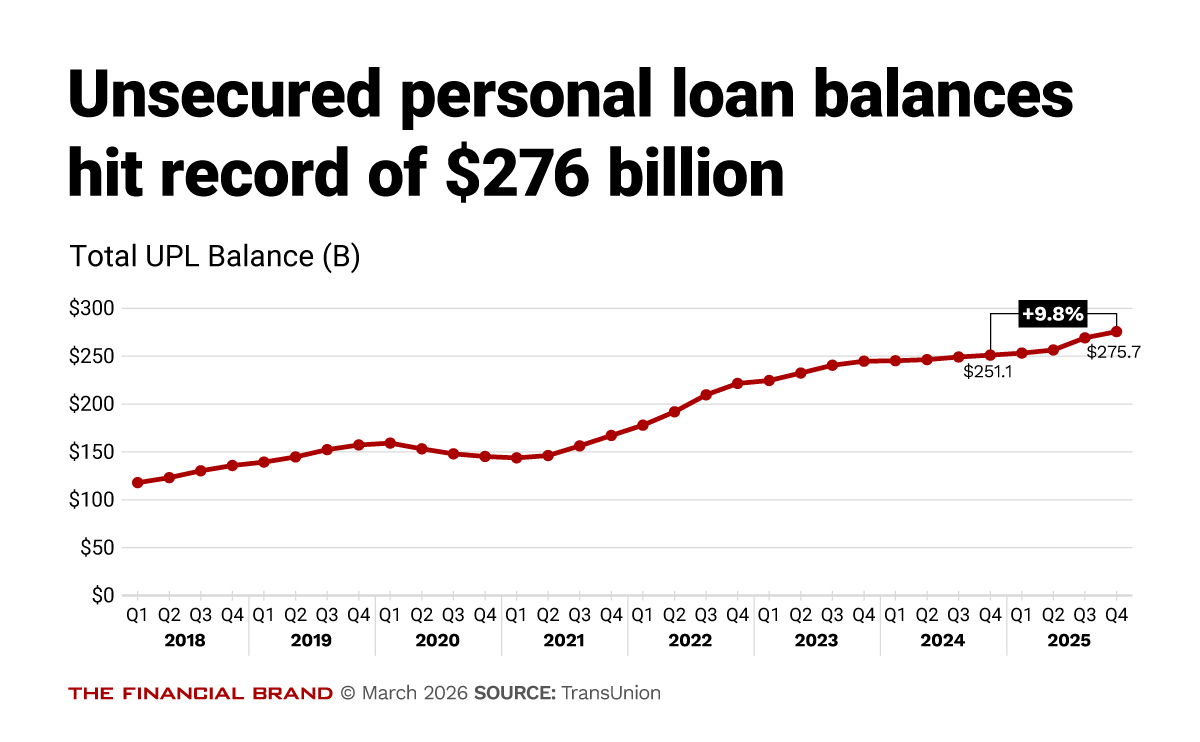

Unsecured personal loan originations hit a record of 7.2 million in the third quarter of 2025, which TransUnion says marked the second consecutive quarter of setting new records. Demand was stronger among subprime borrowers, with originations rising 32.5% year-over-year. By comparison, the near prime and super prime categories saw originations rise by 21.5% each.

The quarterly trend helped push total balances up to a record $276 billion in the fourth quarter, as shown in the chart below. More consumers are obtaining such loans, though TransUnion indicates that the average balance per consumer and per account has remained steady. Drilling deeper, the company indicated that increases among other risk tiers were offset somewhat by lower balances among subprime borrowers.

Roughly 26.4 million Americans had unsecured personal loans at the end of 2025 — 8% of the total U.S. population.

Competitive insight: The most active unsecured personal loan issuers currently are fintechs. Fintechs’ share of origination volume rose to around 42% in 2025, up from about 33%, according to TransUnion.

Watanabe points out that banks and credit unions generally have broader credit options to offer customers, such as home equity credit, whereas fintechs tend to concentrate on a more limited range of offerings.

Danger sign? These findings come at a time when recent reports indicate that more consumers are making hardship withdrawals from their 401K accounts. In 2025 6% of 401K holders at Vanguard Group made such withdrawals, up from 4.8% in 2024, according to the Wall Street Journal.

Marketing tip: Presceened direct mail volume among lenders promoting unsecured personal loans rose by nearly a third at yearend, year-over-year, according to TransUnion. Notably, at the same point, consumers online inquiries regarding these loans was up 44%.

Read more: How LendingClub Is Wielding Its Bank Charter to Steal Your Customers

3. Credit Cards

In the third quarter of 2025, bank card originations shot up by 11.7% year-over-year. That’s not only the fourth quarterly increase but also the strongest annual growth rate in three years, per the TransUnion report. The company indicated that the two main drivers were super prime and subprime customers.

As noted, TransUnion projects lower growth in card originations in 2026, but that’s after major growth.

At a recent special investor update, JPMorgan Chase officials noted that the bank had added 10.4 million new card accounts in 2025. The outlook, per Jeremy Barnum, CFO: “We expect Card to revert closer to long-term trends but still expect strong growth.”

Thoughts on the “K economy”: At the same event, Marianne Lake, CEO of consumer and community banking, remarked that the bank is “seeing a continued separation between the higher earners and lower earners, but we’re not seeing deterioration at the lower end.”

Broadly, “consumer-level delinquencies ticked up after four consecutive quarters of year-over-year improvement, though overall levels remain consistent with those seen in 2023,” according to TransUnion.

Marketing tip: The TransUnion report indicates that lenders were opening more below-prime accounts but with lower opening credit lines, as a risk management measure.

Read next: How a California Credit Union is Growing HELOCs with a Fintech Partnership