Are Your Loans Really Making Money? And Will They Tomorrow?

By Scott Earwood at White Clay

Simple Subscribe

Subscribe Now!

Executive Summary

- Interest rate volatility is back — and banks that don’t factor it into their loan pricing will suffer.

- “Funds transfer pricing” enables lenders to realistically assess what they should charge for loans, building in the possibility that funding prices will change.

- When the next downturn comes, banks using this strategy will still be able to lend profitably. Those who don’t will have to shrink.

After more than a decade of relative stability, interest rate volatility has returned. As a result, many banks are feeling the impact where it hurts most: loan pricing.

As the Federal Reserve continues to adjust rates, institutions are quietly losing revenue because they’re lending at the wrong price. Loans are too often underpriced in ways that overlook liquidity risk, interest rate risk, and the true operational cost of funds.

Funds transfer pricing, the tool that can help solve this problem, is either missing altogether at many institutions or underutilized where it does exist. Larger banks frequently have FTP frameworks in place, but they are not always applied rigorously, while many community banks have yet to adopt them at all.

Funds transfer pricing is an internal pricing tool that helps banks align the price of loans and deposits with the true cost of funds and liquidity. In short, it’s a system for pricing money within the bank.

For example, when a customer deposits $1 million, the treasury function “buys” those funds from the deposit side and “sells” them to the lending side at a transfer rate that reflects market funding costs. As interest rates change, that internal transfer rate adjusts so lenders see the real cost of funds for new loans and can price them accurately.

In essence, FTP helps banks move beyond guesswork. Instead of relying on broad assumptions or legacy pricing habits, they can see the true economics of each transaction and customer relationship. It also factors in the market value of deposits, liquidity and interest rate risk, giving banks a clearer, more accurate view of profitability across the business.

Read more: Banks Flirt With AI Deposits but Fear Dynamic Pricing Backlash

Four Causes of Poor Loan Pricing Practices

So why, if the benefits are clear, do banks continue to underprice loans? There are four main reasons:

1. Cultural inertia

Banking practices are built over years of experience, and many habits were formed in an era when interest rates moved slowly, and funding was abundant. Loan pricing often meant applying a standard profit margin, relying on instinct, or simply following what had worked for years.

Although these approaches have served banks well for a long time, the market environment has evolved, and today they leave institutions stuck with assumptions that are outdated. Updating pricing practices will help banks respond more effectively to today’s market conditions.

2. Volatility of the current market.

After years of near-zero rates, we’re now back in an environment where loan rates can swing by dozens of basis points within a single week. Funding costs can rise sharply in a matter of days. When banks price loans based on outdated assumptions, they are effectively locking in terms that may have already expired.

Consider a loan priced in January that looks reasonable at the time. By March, shifts in the cost of funds can turn that same loan into a drag on margin. That’s why FTP needs to be updated at least weekly, not monthly or quarterly, so banks can recalibrate quickly and avoid loaning blind.

Without that discipline, institutions often discover too late that what seemed like profitable business has led to losses.

3. Fear of pricing for value

The human fear factor also comes into play. Lenders worry about losing business if they set rates that feel too high, so they often shave a few basis points off the price to make sure they close the deal.

That fear only grows when a competitor comes in with slightly better terms. It’s tempting to match or beat them, but that doesn’t always mean the deal is good for the bank. Instead, banks should quantify the potential loss and weigh it against the relationship’s value.

A high-profile client, long-term partner or a profitable relationship might justify an exception, but the decision should be deliberate, not emotional, and based on how much margin is being sacrificed.

What’s often missing is confidence. With solid FTP data, pricing stops being arbitrary and starts reflecting the real cost of funds, liquidity, and the value of the overall relationship. It also allows lenders to properly factor in deposits and quantify exactly what a discount costs, instead of going by feel.

That shifts the conversation. Instead of apologizing for the rate, bankers can stand behind it, explain it, and still protect margin.

4. Technology gaps

Another obstacle is the uneven use of technology. Large institutions often invest in complex systems that can model funding costs, liquidity premiums, and relationship profitability with precision. Smaller and mid-size banks, on the other hand, frequently rely on outdated spreadsheets or reports that cannot capture the full economics of their business.

But even when tools exist, they are not always used to their potential. I’ve seen banks with sophisticated software that still default to simplistic models, leaving out factors like deposit stickiness or cross-sell opportunities that can dramatically change the profitability of a client relationship.

The technology gap, then, is not only about access but also about adoption. If tools are not fully utilized, they cannot provide the insights lenders need.

Data silos are a further challenge. When client information is scattered across core platforms and supporting systems, bankers are unable to gain a full picture of the relationship. Breaking down these silos and consolidating data into a unified, accessible profile enables bankers to accurately evaluate which client relationships drive or diminish profitability.

Read more: Why Deposit Profitability, Not Deposit Volume, Should Be Your Goal

How Funds Transfer Pricing Works in Practice

It can be tempting to dismiss these pricing issues as small slippages that even out across the portfolio.

However, the reality is that even a little mispricing can compound into significant revenue losses worth millions of dollars.

A real-world example demonstrates this clearly.

In March 2022, a bank priced a five-year commercial loan at 3.25%, based on its internal deposit cost of 25 basis points (0.25%) plus a 3% profit margin. At the time, this seemed reasonable: deposit costs were minimal, and the profit margin appeared to cover credit risk, operational costs and profit.

However, the bank’s calculation only considered the deposits it already had on hand — not the potential need to fund the loan if those deposits left.

Deposits are fluid, and if they left, the bank would have had to replace those funds in the markets, such as through Federal Home Loan Bank (FHLB) loans, at much higher rates.

When the same loan was analyzed using FTP, the picture changed. FTP looked at the five-year Treasury rate (2.40%), a baseline for what money cost in the market, and the true cost of funds (2.10%), which reflected what it would have actually cost the bank to replace deposits if they left. With these factors, the loan’s actual profit margin was only 1.15%, far below the 3% the bank had expected.

Without FTP, the bank would not have realized it was underpricing the loan, and nearly 40% of its loan book could have ended up earning much less profit than intended.

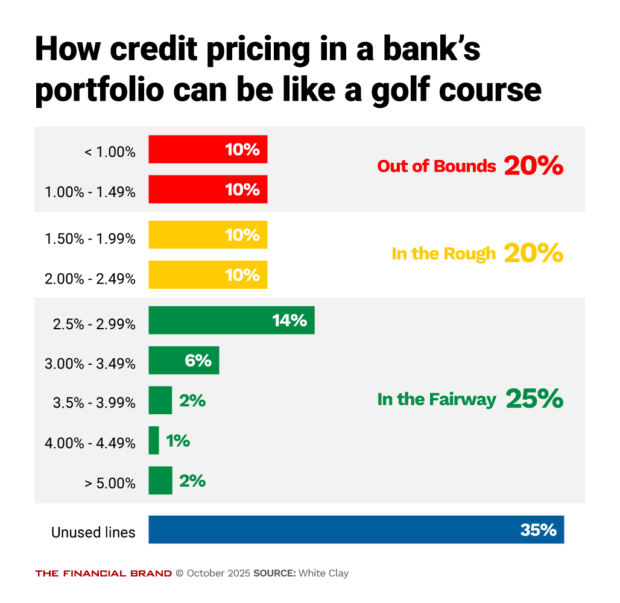

Here’s a visual example of where a bank’s profit margins landed after applying FTP:

Think of it like golf: the green bars are the fairway, where profit margins are healthy, yellow is the rough, where returns are too thin, and red is out of bounds, where pricing doesn’t cover risk or cost.

In this case, about 40% of the portfolio ended up in the rough or out of bounds, meaning profit margins below 2.5%. Only about a quarter of the book was in the fairway, with profit margins of 2.5% or better, and more than a third of credit exposure sat in unused lines that generate no income at all.

The lesson is simple: without a disciplined FTP process, too many loans drift outside the fairway, leaving profitability far short of where banks think it is.

And the payoff of FTP is not just stronger margins today but also resilience when market conditions tighten. When the next downturn comes, as it inevitably will, banks that have mastered FTP will be the ones with the capital and liquidity to keep lending. Those that have not will find themselves forced to shrink their balance sheets, pulling back just when opportunities to grow are emerging.

Whether a bank has never implemented FTP or has it in place but underused, the message is the same: Now is the time to take this concept seriously. Loan pricing has always been a balancing act, but in today’s environment the stakes are higher.

Banks that continue to rely on habit, and fear and operate with technology or data gaps, will keep leaving money on the table, while those that adopt and fully apply FTP will be positioned to grow stronger, even in volatile times.

Read this next: The Era of Ever-Growing Bank Deposits Is Over. Now What?