How Citizens is Growing Student Lending Into Lifetime Relationship Banking

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Executive Summary

- Citizens Bank wants to expand its private college lending expertise into a broader thrust for growth in loans and deposits and for long-term customer acquisition.

- Having acquired College Raptor, an online college planning site, in 2022, it is integrating that platform with other bank products to deliver a student banking “hub.”

- Meanwhile, the end of the federal “Grad Plus” program will double demand for private graduate school loans. Citizens wants a piece of that action.

Citizens Bank is mining the private student loan business, broadening the bank’s strategy to attack longer-term opportunities. Simultaneously, the bank is developing plans to take competitive advantage of major changes coming in 2026 that experts believe will double the size of the private market for graduate school student loans.

The bank’s concentration on the student market — which includes parents — ties into Citizens’ strategic shift to focus more on upmarket customers.

The bank’s execution has included acquisition of College Raptor, an online college planning platform purchased in late 2022 and the unveiling in late September of its digital Student Banking Hub.

Underpinning the bank’s thrust is a belief that the student market, often focused exclusively on the college years, is actually composed of four life stages.

Each has its own needs that can be met with an evolving mixture of products. These stages include the high school years, the period nearing college application and acceptance, the college years, and the years beyond college. The bank hopes that the final stage will deliver ongoing relationships with graduates as they require more banking services.

A key part of this new approach is a growing library of digital content to assist people at each stage with common financial challenges, supplemented with webinars and live seminars.

“Historically, we have been focused largely on the financial aspects. But there’s a lot more to going to college than just financing school,” says Chris Ebeling, EVP and head of student lending. “We needed to engage students and their families in ways that weren’t purely financial.”

Growing the Student Market from a Credit Core

Currently, Citizens’ student lending effort consists of two main categories. The first is education loan refinance, predominantly refinancing government loans. At the end of the third quarter, this portfolio totaled $5.3 billion. The second is education loans provided during students’ time in undergrad and graduate work, which came to $3.3 billion in the same period. Combined, both are nearly 13% of the bank’s retail credit portfolio.

A key differentiator for Citizen’s student lending program is its multi-year approval feature for qualifying borrowers and parents.

When an applicant seeks a loan in their freshman year, the bank does a single hard pull on their credit, explains Ebeling. If the applicant is eligible, the bank will offer them authorization for their estimated needs for the duration of their undergraduate work. Actual disbursements each year are made for their annual needs. In each subsequent year, the bank performs only a soft pull. By contrast, says Ebeling, the bank’s competitors — especially market leader Sallie Mae — typically do a hard pull and a fresh credit analysis every year.

Ebeling says the multi-year approval option has been a major selling point for Citizens as it works with individual schools to be included in the financial aid department’s list of preferred lenders.

Ebeling first came to Citizens in 2017 as EVP for corporate strategy and development. Past posts included more than a decade in consulting at Bain & Co., and Ebeling initially concentrated on finding acquisition candidates for the bank.

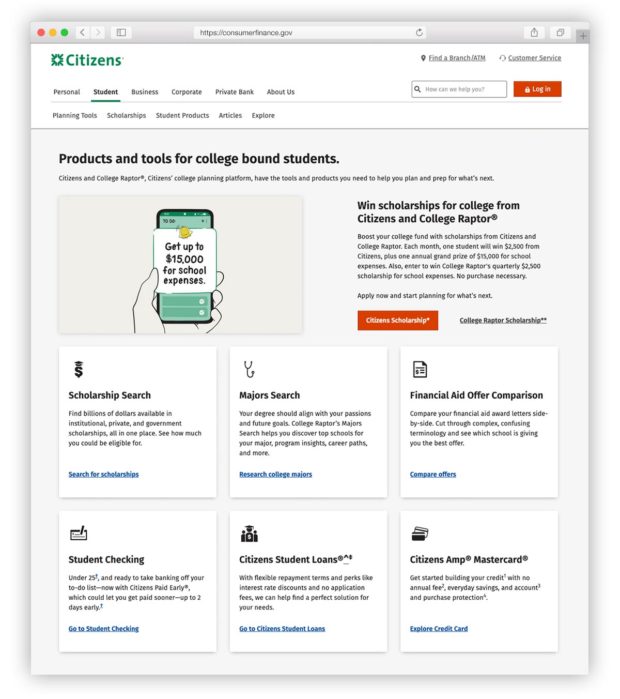

Later, the opportunity to take charge of student lending arose. Not long into the job the bank saw the opportunity to satisfy people’s need for information and advice. Ebeling says several platforms offered content and tools for the college-bound and their parents, but College Raptor was the best. Among its features are side-by-side comparisons of potential scholarship aid at schools.

“With College Raptor, with our deposit and lending products, we have had the broadest set of capabilities out there for students and their families. But our customers didn’t know it,” says Ebeling.

The problem was that the products and services resided in corporate silos. College Raptor, a wholly owned subsidiary of the bank now, was isolated.

“It was not coming together in a way that was holistic,” says Ebeling.

Read more:

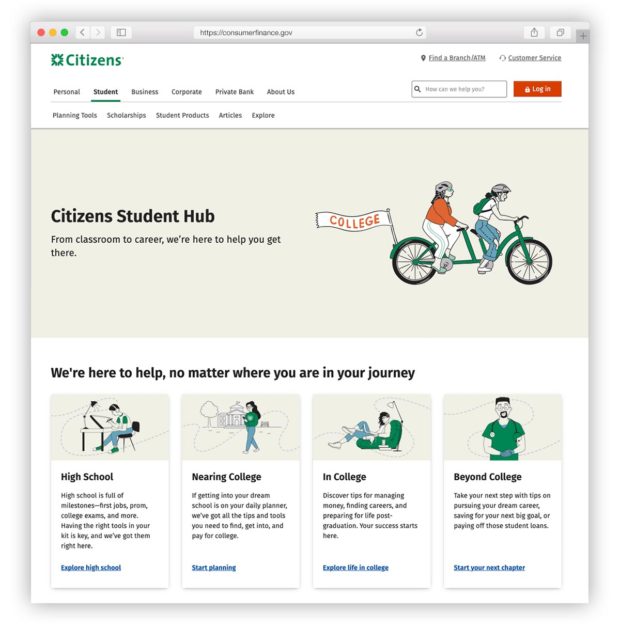

The Debut of the Student Banking Hub

At the very top of the Citizens’ home page, major business lines are listed in the horizontal menu. A recent addition to the usual categories is “Student,” coming right after the first category, “Personal.”

Behind that now resides the bank’s Student Banking Hub. Visitors can navigate the hub through the four life stage choices.

Further down on the home page are modules that lead to tools and content, much of it from College Raptor, as well as links to product categories. Among the latter are discounted student checking accounts and the Citizens Amp Mastercard, which is designed for student cardholders with no annual fee.

Life stage sub-hubs start off not with a hard-sell, but with content tailored to the stage the students have reached.

The first example, below, is the page for undergraduates.

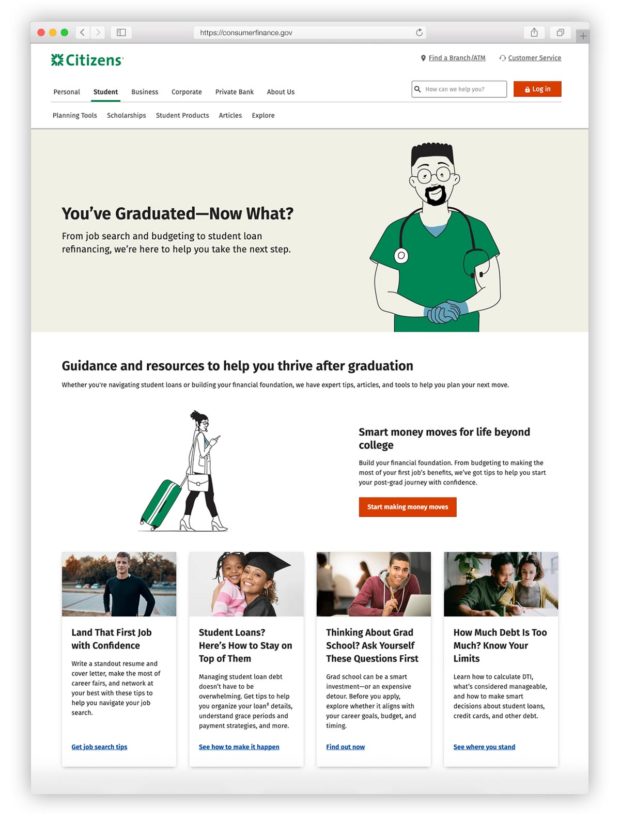

The second example demonstrates how the bank hopes to gain graduates’ business — beyond loan payments — once they start working. Content here addresses life challenges and a realistic assessment about whether going back for graduate education makes sense.

Ebeling says the hub is supplemented with an email newsletter to promote availability of the broad array of services.

“We actually already had a lot of the ingredients — but we’re just starting to put them together in ways that are compelling,” says Ebeling. This meant that setting up the hub didn’t require substantially expanding the student lending team. Instead, Ebeling hired someone to guide the strategy and to coordinate among digital staff and staff in other functions providing deposits and other services.

Read more: Gen Z Conundrum: How to Help Young Adults Save While They Pay Off Debt

Earning Entrée to Two Tiers of Affluence

The bank is hoping this strategy will also attract more affluent consumers to the bank.

First, there’s the parents. “Households that have college-bound people in them tend to be a little bit further up the income spectrum,” says Ebeling.

Then there are the graduates. “If we can retain them into adulthood, they’re going to become the next cohort of engaged mass affluent customers,” says Ebeling. “They tend to have higher earnings potential than those who are not college educated. But that’s a longer-term play.”

The play is still coming together at Citizens, Ebeling admits. He says the bank’s strongest efforts among the four life stages are the nearing college and college segments. Both lean particularly heavily on College Raptor.

Ebeling says the bank has more work to do on the bookend stages, the high school and beyond college stage.

Read more: As the Wealth Gap Widens, Banks Have to Pick Between Two Distinct Customer Sets

A Major New Opportunity Lurks, Courtesy of Washington

The impact of delinquent federal student loan debt is widely known as a pending credit risk, as the federal government has returned to collecting on seriously delinquent student loans. Less well-known is that the government is also cutting back on its lending.

Case in point: The federal Grad Plus loan program for graduate students will begin sunsetting in July 2026, under the terms of the Big Beautiful Bill.

The private student lending market represents about 10% of the total, notes Ebeling, but that will change as the private sector begins competing for graduate school loan volume that used to go to the federal program. (Capping of federal undergrad student loan amounts may also send more business to private lenders, according to Ebeling.)

“The addressable market is roughly going to double” for graduate lending, Ebeling says. Up until now, private student lenders’ production has chiefly been undergraduate loans, but he says now grad school lending may become an equal part of lenders’ business.

Ebeling says the bank is already considering how the hub could be expanded as graduate school finance becomes a more significant factor.

However, there’s also a fundamental challenge. Many school’s grad students depend on the Grad Plus program. Ebeling says that colleges and universities are already asking if private lenders can accommodate all of the grad borrowers with credit.

He explains that nearly all undergraduate borrowers need to have a co-signer, whereas grad students generally don’t want a co-signer. Lenders must figure out how to adapt a product chiefly meant for undergrads to graduate borrowers.

One of the concepts Citizens is exploring is some form of risk-sharing between the bank and graduate schools. He knows that competitors are also looking at this strategy as institutions ask how they will meet the credit demand.

“I think some schools will ultimately do them,” Ebeling says, especially those with very large endowments. “But we’re still working through this and we’ll see how this all plays out.”

Read this next: More Banking Apps Offer Predictive Insights, But Many Alerts Arrive Too Late