Can Offer Management Become a Super-Power for Your Financial Institution?

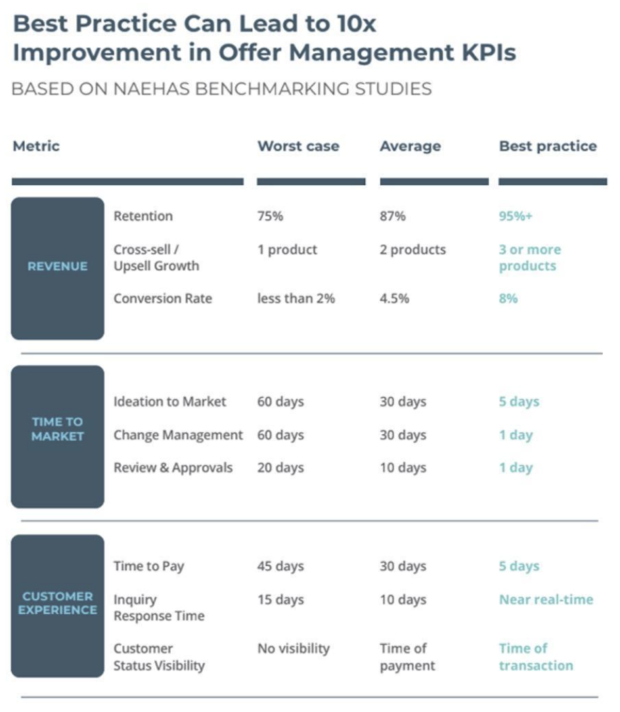

Offer management has emerged as a critical growth driver for financial institutions, yet most financial institutions convert less than 5% of campaigns despite allocating nearly half their marketing budgets to these efforts. There are three key benchmarks that separate top performers — who achieve 8% conversion rates — from the pack: accelerating time-to-market (cutting launch times by up to 30 days), eliminating compliance bottlenecks (reducing review time by 90%), and building real-time feedback loops that enable rapid optimization.

By Mark B. Egan

Simple Subscribe

Subscribe Now!

Offer management is emerging as a high-leverage growth driver for financial institutions. Those that apply up-to-date best practices in creating, deploying and optimizing offers are seeing dramatic gains across performance metrics — from customer retention and conversions to upsell rates and time-to-market.

The increased focus on offer management is a result of two converging trends: growing dissatisfaction with traditional marketing automation platforms or outdated offer management systems and rising consumer expectations for personalization. The shift has come with a growing body of research, including a 2022 study by Capgemini that frames the issue starkly: Financial institutions allocate about 45% of their marketing budgets to offers and campaigns, yet average conversion rates remain low at 4.5%. Top-performing banks, by contrast, achieve conversion rates closer to 8%, underscoring the opportunity for more effective, targeted execution.

For financial services marketers, the problem is well-diagnosed. Capgemini points to three roadblocks that hinder better outcomes. First, offer management processes are slow, often taking up to six months from ideation to fulfillment. At the same time, banks frequently can’t execute the kind of programs they want to due to rigid data models. Finally, legacy approaches don’t prioritize feedback loops that track offer performance, leading to poor offer attribution and little insight about what works and what doesn’t.

But diagnosis isn’t a cure. Improving offer management requires rethinking workflows, automating decision points, and enabling real-time responsiveness across teams. A new white paper from Naehas, a firm that helps financial institutions structure, govern, and execute products, pricing, and compliance more effectively, provides a roadmap. Drawing on extensive industry research, the report outlines best practices and key benchmarks that can help teams transform their offer management capabilities into significant drivers of growth.

Want more insights like these? Check out Naehas’ content hub: More Speed, More Value: Bring Personalized Offers to Market Faster.

1. Improve Time to Market

The benchmark: Speed is critical. With customer needs and credit conditions shifting quickly, banks that spend months building offers risk missing opportunities and losing ground to faster-moving competitors. According to Naehas’ Product Management Principal Hayat Yahia, doubling positive outcomes is achievable through greater agility and more precise targeting — made possible by rapidly iterating on offers. Such an approach, Yahia said, can cut time to market by up to 30 days for entirely new campaigns and fewer than 15 days for subsequent offers.

What typically goes wrong: Many institutions have structured their offer management processes around outdated systems that depend on manual steps, from exporting customer lists and hand-coding rules to copying content across channels and awaiting compliance reviews. Each handoff adds friction and delay. Compounding the issue, internal teams often operate under service-level agreements that allow turnaround times of up to two weeks per team. Such long development cycles, Yahia notes, also tend to drive teams to seek workarounds that add costs even as they seek to circumvent problems. “It doesn’t really matter if the tool can do things faster. If a process says somebody has two weeks to review an offer, that’s how long it’s going to take,” she said.

How to do it right: Best practices begin with defining a clear vision for each offer. From there, teams should map relevant data, assess the systems involved, and identify redundancies. A key step is to align the customer segments you are targeting with the right mix of channels, whether social media, email, direct mail, or others. Planning the offer and its supporting content as a unified package ensures consistency. Early collaboration with stakeholders on content and terms reduces the potential for delays and increases the likelihood of hitting targets.

Want more insights like this? Check out Naehas’ content portal: Bring Personalized Offers to Market Faster

2. Solve for Bottlenecks and Blindspots that Lead to Bad Data

The benchmark: Time doesn’t only bring inefficiency; it also brings risk. A lengthy compliance process increases the likelihood that a campaign’s underlying data will have changed by the time the campaign is launched. The same holds true for segmentation and product targeting. Naehas offers the example of a bank that was able to cut document compliance review time by 90%, enabling campaigns to go live within just 24 hours of reaching that stage. The bank achieved this by automating formerly manual processes, such as compliance checks and approvals routing — a shift that increased accuracy and reduced compliance risk.

What typically goes wrong: Campaigns are often built on flawed or incomplete data, relying on rigid systems that are isolated from compliance workflows. According to Naehas, 43% of banks lack complete visibility into which campaigns are active or whether they were properly vetted. This lack of oversight has real consequences: Naehas cites enforcement actions that have cost institutions millions, including one bank that paid a $19 million fine. The white paper also notes that 50% of banks say review and approval of marketing materials creates bottlenecks, further delaying execution and increasing risk exposure.

How to do it right: Automating compliance reviews offers many advantages, especially when it comes to updating dynamic elements like fees or interest rates. Institutions using automation report dramatic gains in speed and accuracy. And they are better able to create an audit trail for regulatory compliance. Using up-to-date data is another best practice: Not only does it maximize the chances that all targets will meet eligibility requirements — improving engagement and revenues — it is a key to a good customer experience. Once a customer has accepted an offer, they should be able to track its progress in real time. For instance, a customer who will get a bonus for opening and funding a savings account should be able to easily check when the terms of that offer are met. Too often, the customer and the bank’s contact center do not have that information readily available. Flexibility and integration are key to turning data from a liability into an advantage.

3. Build Feedback Loops

The benchmark: Top-performing institutions, working collaboratively from shared data resources, can achieve redemption rates above 90%, according to Naehas. Personalized marketing done well can deliver up to an 8x return on marketing investment and increase sales by more than 10%

What typically goes wrong: Many institutions lack a useful feedback loop. Offers are launched without thoughtful, clearly defined KPIs, and performance data is either delayed or incomplete. Adjustments, if they happen at all, are reactive, rather than process-driven. Campaign teams operate in silos, and critical insights, like fulfillment status or customer response, don’t reach decision-makers in time to act. Yahia notes that without holistic coordination across departments, banks miss opportunities to improve results and customer experience.

How to do it right: Start with clearly defined business objectives, whether growing deposits, expanding card usage, or increasing cross-sell. From there, establish KPIs that are tightly linked to those objectives. Finally, measure your success in near real-time and iterate while campaigns are live, performing A/B tests, refining targets, and adjusting content. Visibility into performance, fulfillment, and customer response, shared across teams, turns data into action. When the whole organization works from the same source of truth, agility becomes sustainable.

“You must think holistically and bring everybody together for greater transparency and visibility. It takes a whole family to get it done right,” Yahia said.

Offer management may not be new, but it is being redefined. The combination of better data access, integrated platforms, and more transparent processes allows institutions to move faster, reduce risk, and deliver more relevant experiences to customers. As the examples here show, those gains are measurable and can have a major impact.

Improvement goes beyond deploying new technology. It requires holistic rethinking of processes — including, critically, fixing what slows teams down: ambiguous lines of accountability, manual workarounds, and disconnected systems. With targeted adjustments and the right support, financial institutions can make offer management a powerful and reliable lever for growth.