Opportunity Grows in Home Equity, And So Does Competition

Record home equity levels — and card debt — are prompting banks and credit unions to ramp up promotion of equity loans and lines of credit. But technologically savvy competitors are taking away crucial market share.

By Steve Cocheo, Senior Executive Editor at The Financial Brand

Simple Subscribe

Subscribe Now!

Several factors are expanding opportunities for banks and credit unions to build their home equity lending business. But lenders also face eroding market share to nontraditional competitors, many of which have demonstrated greater agility.

The potential expansion in opportunity also has a lot of moving parts — and it takes place against an uncertain economic backdrop, and a hazy outlook for future interest rates.

Nonetheless, lenders have been placing their chips on growth. “From 2023 to 2024, total home equity line of credit marketing spend rose 130%, with email and direct mail volumes up 201% and 125% respectively,” according to a report by Comperemedia, a Mintel company, which tracks ad spending. “Early 2025 data suggests this momentum is only accelerating.”

Why Are Home Equity Products Heating Up?

Among the factors that favor more home equity lending:

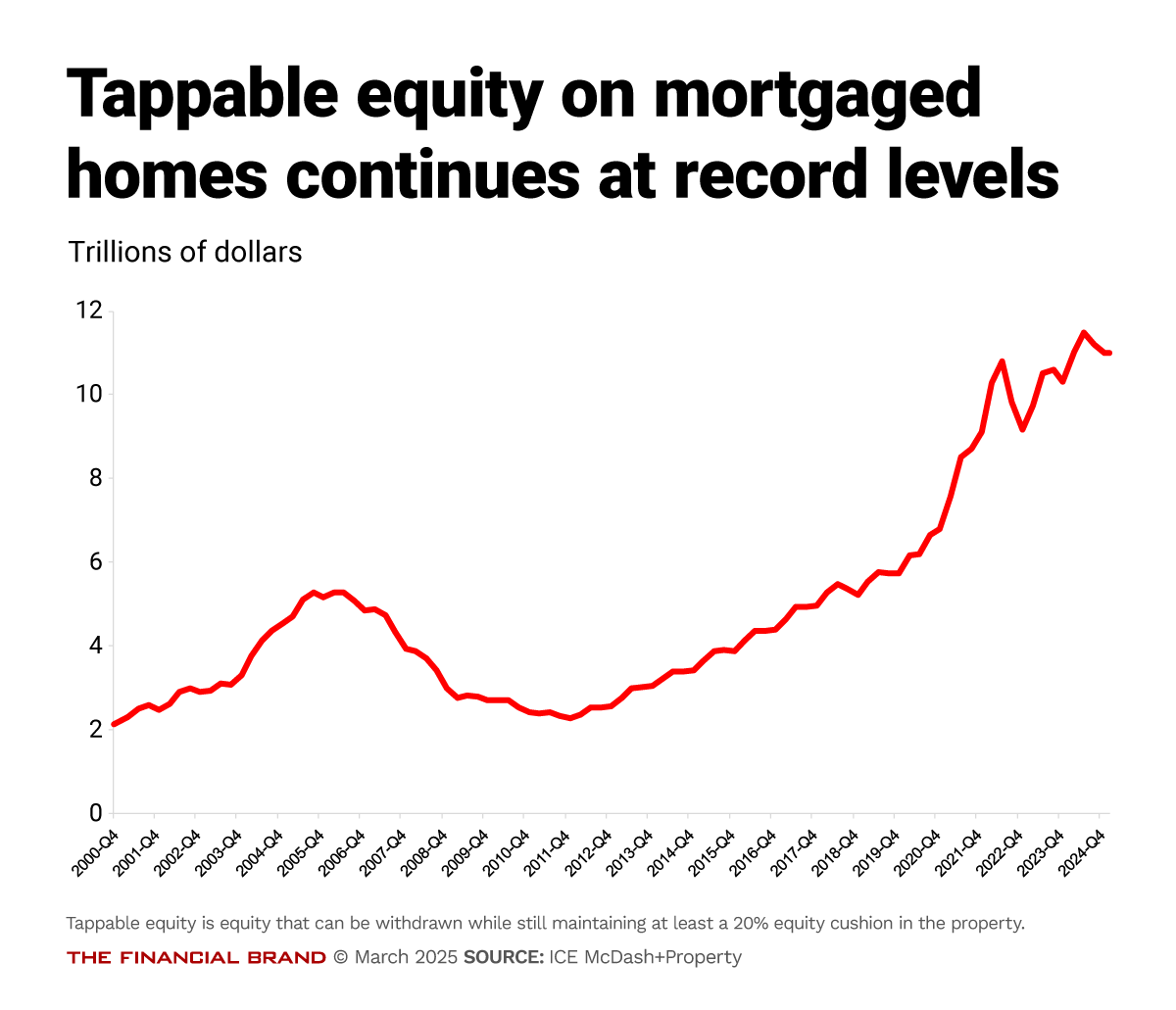

• Tappable home equity is huge. This is equity that can be used while still maintaining at least a 20% equity buffer — it reached a record level in the second quarter of 2024. Though it fell off a bit, it remained at $11 trillion at yearend, up from the same point the year before. It’s also the highest level of tappable equity in a fourth quarter on record, according to the ICE (Intercontinental Exchange) Mortgage Monitor Report.

ICE reports that at yearend the average homeowner had $203,000 of tappable equity in their home.

• Credit card debt has reached record levels — at sometimes astronomical interest rates. For debt-burdened consumers, borrowing against their homes is again becoming a tool to consolidate consumer debt at lower rates, thanks in part to home equity lines of credit and home equity term loans being secured credit.

• The nation’s housing stock is growing older, increasing the need for renovations. At the same time, high prices and still relatively high rates are keeping more people where they are. The National Association of Home Builders’ Eye on Housing reports that the median age of owner-occupied housing is 40 years and that homes built before 1970 comprise just over a third of the housing stock.

Renovation and expansion — the finished basement, the dormer, the new roof, updated electrical service — have long been key reasons for tapping home equity. “Many homeowners will address deferred maintenance, and equity loans will offer owners a cost-effective solution to fund critical updates,” says Marisa Frys, digital marketing analyst at Comperemedia, a Mintel company.

• The balance of rates on existing mortgages versus home equity credit favors HELOCs and HE loans. During a late March webinar sponsored by the Consumer Bankers Association and Curinos, Ken Flaherty, senior manager, retail lending, at the consultancy, noted that about 67% of first mortgage holders have home loans with rates under 4.5%. The rate on first mortgages would have to fall below that. As of mid-March, the average rate on 30-year fixed-rate mortgages was 6.76%, according to Bankrate.com.

Home equity products offer homeowners the opportunity to tap equity, albeit at current rates, without subjecting their entire mortgage to those rates. Some lenders’ marketing points that out explicitly, such as SoFi: “Up to 90% or $500,000 of your home’s equity with no change to your current mortgage rate.”

• Interest rates are not expected to move much lower in 2025, if at all. Flaherty noted that many mortgage holders are sitting on rates between 3% and 4% from the heyday of lower levels, so it would take major movement of rates to push them toward cash-out refis instead of home equity products.

“Perhaps we might get a little bit of rate relief, but certainly as the Federal Reserve is trending right now, we’re likely to get maybe one cut, or maybe no cut, this year. We might even see some increases later this year,” said Flaherty.

• Credit performance on current home equity lending is decent. Flaherty pointed out that where consumers run into difficulty, in the current economic environment, they are more likely to be slow payers than defaulters.

So what’s the catch? We’ll look at several caveats from Flaherty and other Curinos analysts, as well as current home equity marketing trends and approaches, as tracked by Comperemedia’s Frys.

Read more: Lending Will Accelerate in 2025 As Consumers Get Used to Today’s Interest Rates

Economic Uncertainty Hangs Like a Gray Cloud

For now, while the stock market has been a very unpleasant theme park ride, the economy remains in decent shape.

Flaherty said the employment picture continues to encourage people. “There is more uncertainty regarding what the future holds,” he said, “but we’re still holding relatively strong and that’s keeping consumers confident. It’s also keeping many home equity lenders very confident on the health of their portfolios and they continue to perform well.”

But …

The balance could be disturbed if there are upticks in unemployment, warned Flaherty. If that happens, it will coincide with a time when the dollar isn’t going as far — and as tariffs may add to lingering inflation. Salary levels are already not keeping up with inflation, he points out. And the U.S. household savings rate is at the lowest level it’s been in over two decades.

So, according to Flaherty, it might be difficult for home equity lenders to continue to push further if cracks start to show in the performance of current borrowers.

For consumers, he said, “there’s just not that much of a cushion to fall back on.”

Homeowners as a group seem cognizant of the risks, going by the ICE report. “Borrowers are withdrawing equity at less than half the rate they typically would,” the report says. “… That means more than a half a trillion dollars in home equity have gone untapped, and not flowed back through the broader economy through retail and other spending.” In this atmosphere, HELOCs offer more control versus lump-sum HE loans.

Read more: How Pay-Over-Time Can Help Banks Fight the BNPL Surge

Lines of Credit Don’t Always Turn into Actual Borrowing

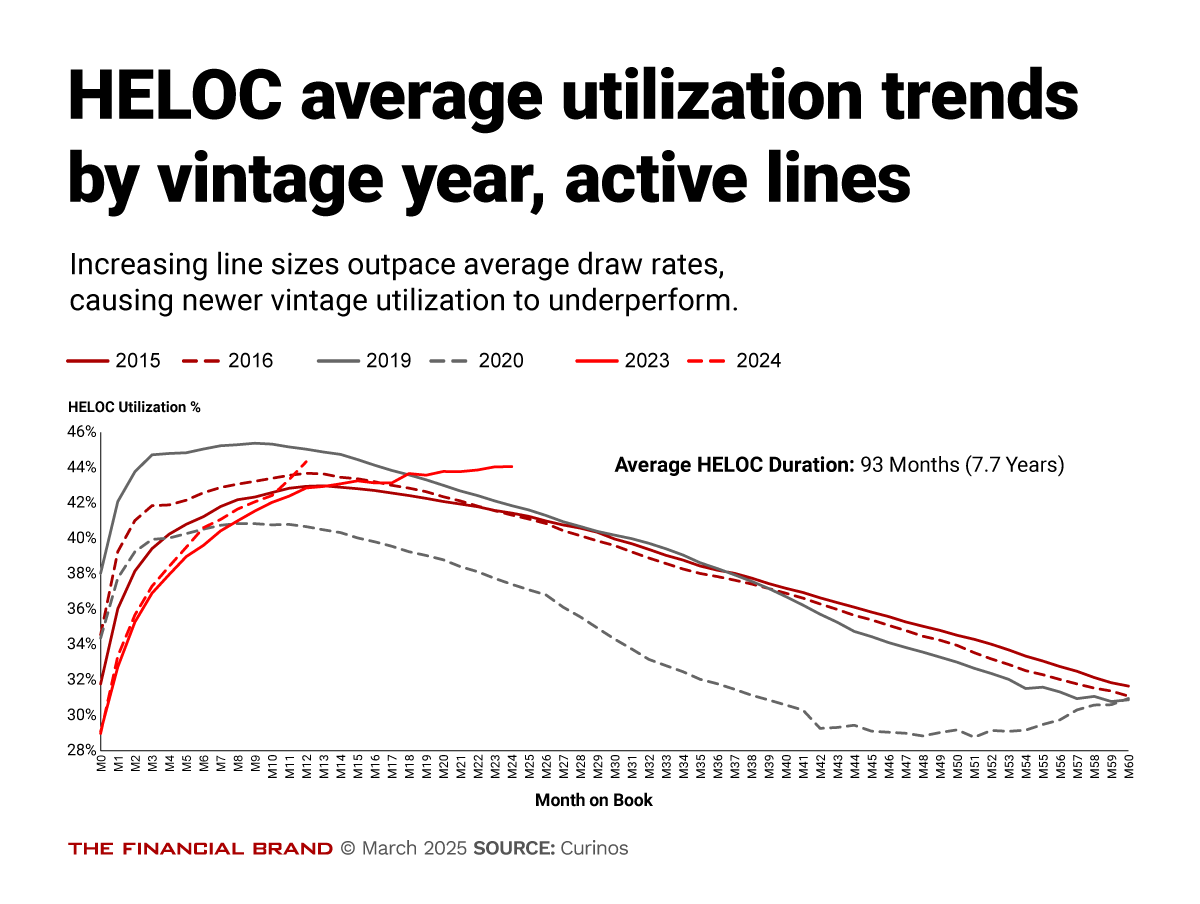

In recent years the rate of HELOC line originations has been flat to lower, according to Kinley Hicks, senior associate, retail lending, at Curinos, but the size of the lines has been increasing due to the ballooning home prices. Hicks said that in 2015 the average HELOC line came to just under $120,000. In 2024, this had jumped to an average of $150,000.

However, as these are lines of credit, borrowers don’t necessarily use them completely during the drawdown period of these loans. Hicks pointed out that utilization rates can be a challenge. A lender may have authorized so much credit based on the property and the perceived risk of the consumer, but interest is only earned on what’s borrowed. Among the 2015-2016 vintages, which are widely reaching the end of their draw down period, the utilization rate is currently around 20%. So far, the utilization rate on the 2024 vintage is higher, at around 40%.

And from a separate Curinos report: “The fact is that two-thirds of depository applicants that don’t take a draw at closing never will.” (More on that point in a moment.)

New Competition and Digital Promotion Challenge the Status Quo

Curinos speakers pointed out that the balance of power has been shifting in the home equity credit space. Ten years ago, Flaherty said, depository lenders — banks and credit unions — accounted for virtually all home equity lending.

But Flaherty says that in 2024 depository institutions accounted for 80% of home equity originations, based on the firm’s computations.

Nontraditional lenders, notably fintechs and independent mortgage banks, won 15% of the pie in 2024, up from 2% only five years back. The remaining 5% went to “HEI” firms. That stands for “home equity investment.” In simple terms, the company — examples include Hometap and Point — invests in the property, advancing money in exchange for a stake in future price appreciation of the home. Repayment comes at the end of the agreement or when the home is sold.

Typically, according to Flaherty, traditional lenders don’t have minimum draw requirements and many don’t charge origination fees on HELOCs. Generally full documentation is required.

By contrast, fintechs and independent mortgage banks have high minimum draw requirements and charge fees of 1% to 6% of the HELOC or HE loan amount.

The investment firms require full payout of the amount they are investing, he said, and charge a fee of 3% to 5% of their total investment.

The nontraditional lenders want more of the business, said Flaherty. Even though their products aren’t substantially different from banks and credit unions, they do offer two advantages — less friction and more speed. Analysis presented by Hicks indicated that many traditional players still take a lot of time to evaluate home equity credit applications and can take weeks to deliver funds.

In contrast, according to Curinos: “Non-traditional lenders close faster than depositories, by a lot, and their draws at closing are much higher, even when depository closings that result in no draw are thrown out of the mix.”

Borrowers in urgent need of credit may especially value speed above all — and are willing to pay for it.

“If that’s the case,” Curinos says, “depositories would be well advised to speed things up, which may result in higher draws and fewer closings resulting in no draws at all.”

Already, traditional players have had to adapt to changing preferences. In 2015, Kinley said, 79% of HELOC originations in traditional lenders came from branches. Thus far in 2025, the firm has found, only 52% are originated via branches. The rest comes from call centers (25%) and digital sources (23%).

Read more: Subprime Auto Loan Delinquencies Boom, Spurred by Rates and Car Prices

Promoting Financial Institutions’ Home Equity Offerings

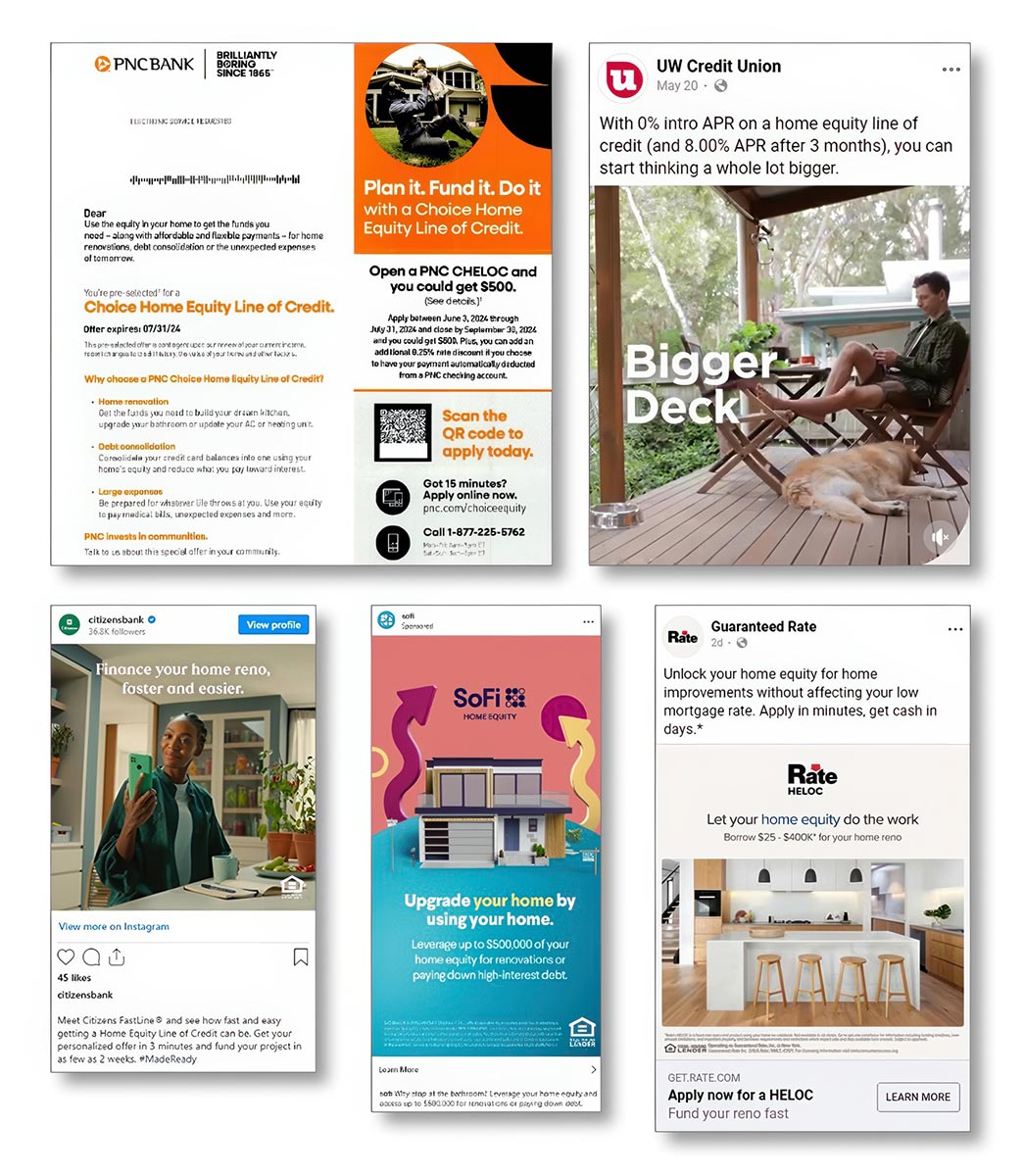

In her analysis of channel spend, Comperemedia’s Marisa Frys indicates that, excluding direct mail, a perennial favorite, about 58% of spending goes toward paid social media ads. Multiple approaches by both depository institutions and nonbanks are sampled below. (Direct mail accounted for 96% of overall promotional spending for home equity products, so the industry has a long way to go.)

“In 2024, lenders sharpened their messaging to reflect HELOC’s evolving role in consumers’ financial lives,” says Frys. “Campaigns emphasized speed, ease of application, and personalized offers — positioning HELOCs as practical tools for funding renovations, consolidating debt, or navigating financial challenges.” (Ad compilations provided above and below by Comperemedia.)

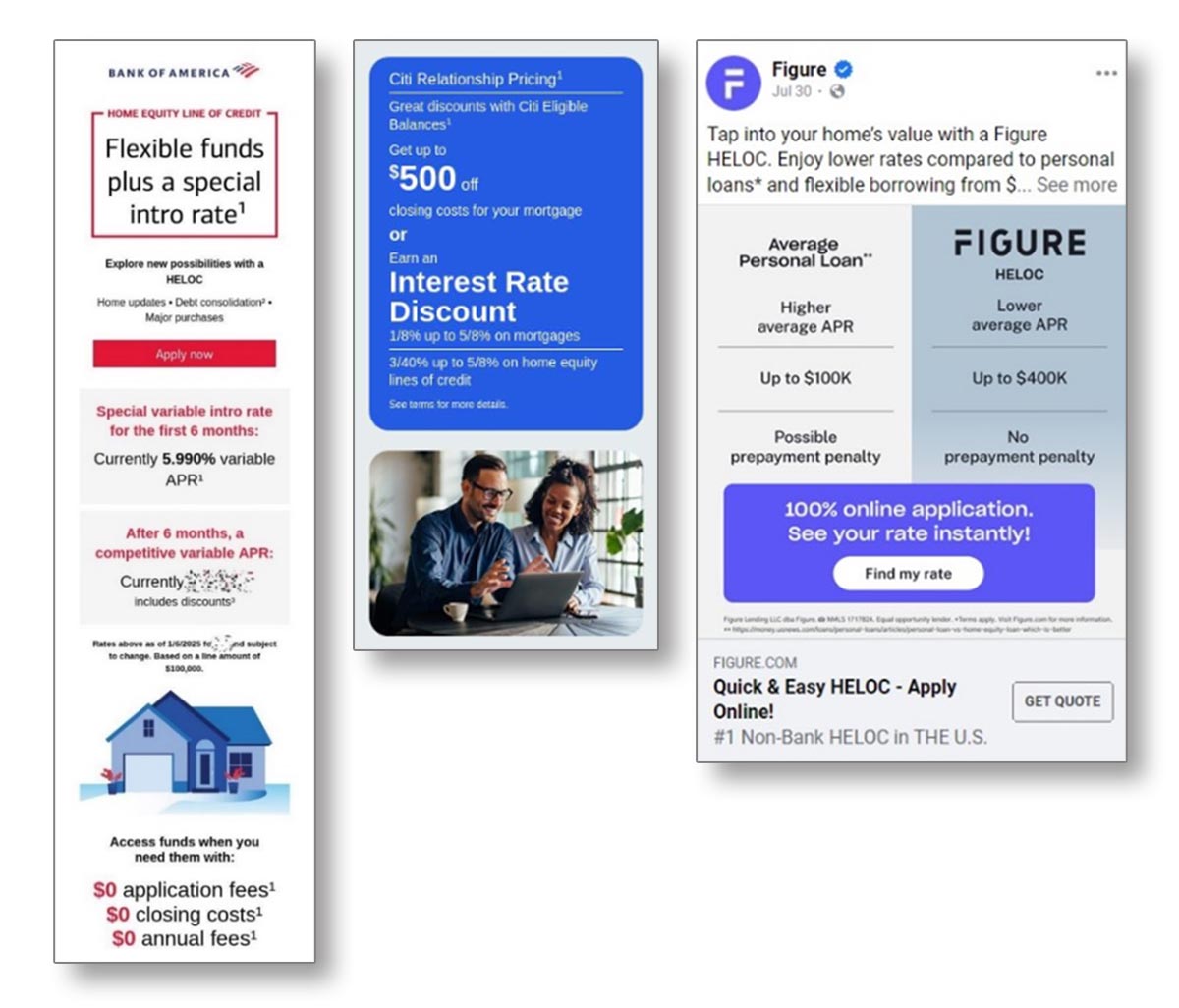

While some of this is traditional in theme, Frys says lenders have been refining their messages. They have been stressing that larger loan amounts are available and have pushed the rate advantage over both credit cards and unsecured personal loans.

“Flexibility and transparency are frequently highlighted,” says Frys, “reinforcing that borrowers can draw funds as needed — rather than commit to a lump sum.”

Promotional rates have also appeared in lenders’ arsenals. Frys noted that UW Credit Union promoted a 0% APR for the first six months of its HELOCs and PNC offered a 0.25% introductory rate. In its offers, Citibank has been promoting relationship pricing, offering discounts that increase based on other business done with the bank.