How Consumers Value – and Use – Branches is Shifting in Subtle Ways

Consumer preferences about which banking activities they want to do online and which they prefer to conduct in person are bifurcating. That much many banks already understand. But institutions that focus solely on the operational issue of which services to offer where may be missing an important emotional piece of the puzzle: Even consumers who prefer online also want the security and reassurance provided by a nearby branch – even if they never use it.

By Corey Wrinn, Rivel Banking Research

Simple Subscribe

Subscribe Now!

Bank leaders have traditionally relied on building relationships with their clients through face-to-face transactions and advice in order to build trust and ultimately more business. New research finds that this is a trend that perhaps is coming to an end with a push to digital options on service, and a preference for branches, but only in certain situations.

15 Minutes Away Matters

For consumers, bank branches offer everyday convenience to do transactions, the ability to speak to a professional in-person, but importantly, provide a sense of safety even if they never visit. According to Rivel’s November 2024 National Pulse Survey, 52% of consumers have visited their primary bank’s branch between 1-4 times in the past 12 months. Baby Boomers lead this national data set with an average of 4.6 visits per year, while Gen Z is lowest at 3.6 visits.

However, Rivel’s research also reveals that 69% of consumers prefer a branch within 15 minutes of them to consider switching to a new institution. Surprisingly, this strong desire is remarkably equal across ages and income levels as well.

So, why does the branch still hold sway and what can financial institutions do to maximize their consumers’ visits?

Branch Strategy in Flux

With more than 40% of bank leaders believing their institution will purchase another this upcoming year, there will continue to be a shake-up in the banking options available for both consumers and businesses. Banks often pursue acquisitions of competitors to cut expenses on overlapping staff, services and facilities in order to drive profitability. In recent years, closing branches has often proven integral to deal-related cost-cutting.

Therefore, with potentially fewer branch options, how can smaller community banks and credit unions stand out within a changing landscape? By providing the services consumers need today and planning for tomorrow.

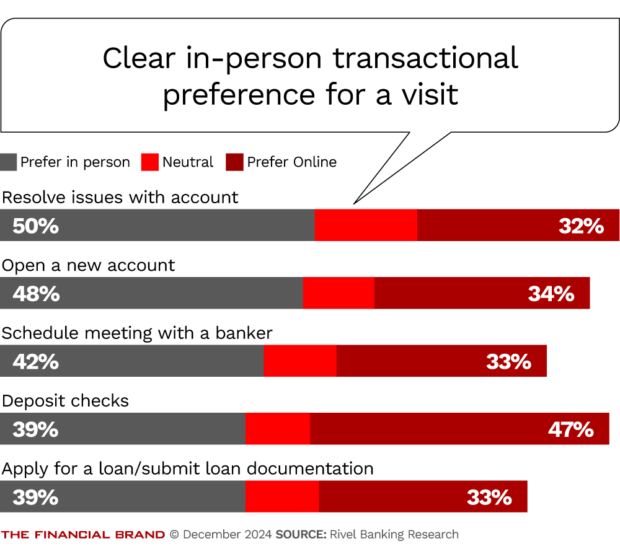

According to Rivel’s newest research on branch demand, there are four clear branch drivers (compared to online options) for those consumers looking to manage their primary banking relationships:

- Resolving an issue with their account

- Opening a new account

- Scheduling a meeting with a banker

- Applying for a loan (and submitting documentation)

In 2024, Cornerstone Bank in Massachusetts developed an online deposit account opening system to improve customer experience for younger generations, knowing that they prefer a more online-centric experience. After a planned and thoughtful launch, their new system has boosted new deposit account generation, with overwhelmingly positive customer feedback. According to Cornerstone’s CEO Todd Tallman, the bank is now expanding the system to its branch network to ensure a consistent account opening experience across online and in-person platforms. “We are very excited about this new streamlined approach because our branch network continues to be a crucial connection to our customers.”

However, more common transactions done in-person have fallen from the weekly or even daily visits of the past and now a majority of consumers are doing what they can easily online. The outlier is that traditional relationship-building, problem-solving face-to-face meeting. Certain consumers still come directly to the branch to talk through an issue, hoping for speed and a tailored experience.

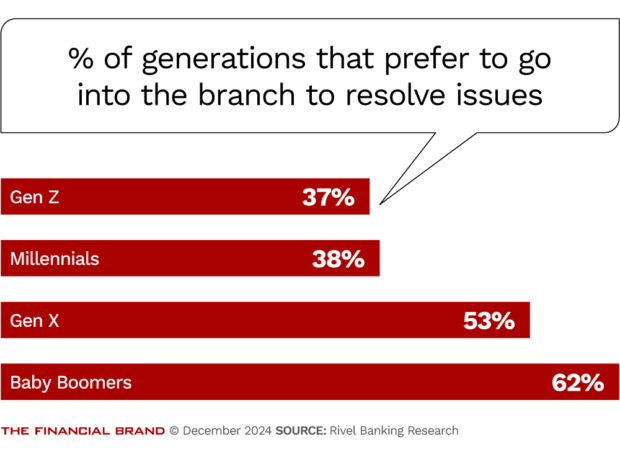

Overall, 50% of consumers prefer to visit a branch to get their problem solved, although its average score is carried by the two older generations, with Gen Z and Millennials much preferring online options. Banks should be thinking today about how they’re able to support both ends of that demand curve: face-to-face solutions at the branch as well as a variety of chat, FAQ, or email options for those that prefer it.

Problems Solved Locations

Despite “resolving issues” being the top reasons that consumers go to the branch today, it’s not their first stop on their path to begin finding a solution to their bank-related problem.

Preferred Method to Begin Solving an Issue with a Personal Bank Account Average Ranking (5 being strongest preference, 1 being least preference)

- Send email — 3.71

- Online chat — 3.15

- Visit branch — 3.03

- Check website — 2.81

- Phone call — 2.30

Sending an email is the top choice, with an average ranking of 3.71 out of 5, followed by online chat at 3.15. These methods offer convenience and efficiency, allowing customers to articulate their concerns clearly and receive timely responses.

More importantly, they can do it from home, their work, or their car without having to carve time out of their day to arrive somewhere in-person. They’re passive and allow the consumer to move on with their day while waiting for their bank or credit union to respond in time.

Visiting a branch remains important for more complex or sensitive issues, with an average ranking score of 3.03. This indicates that many customers still value personal interaction for certain tasks, and perhaps the reassuring conversation with a bank representative that can provide help in real-time.

Traditional phone calls are the least preferred method, with an average ranking of 2.30, suggesting they are seen as less efficient and more time-consuming. Checking the bank’s website, with an average ranking of 2.81, is useful but not the primary choice for most customers.

Banks should enhance their digital services while maintaining robust in-person support to meet diverse customer preferences. It’s not enough to simply wait until consumers happen to visit the branch those 4 to 5 times per year, but rather boost the digital problem-solving capabilities, which will drive loyalty and ultimately retention when a consumer knows their financial institution can find a solution quickly and easily.

What the Future Demands

The future of the branch is simply focused on ways to keep customers and members active with the institution. More frequent visits, more conversations, and deeper connections will drive long-term growth. Some pieces of the bank branch experience cannot be replicated online, and it can be seen in consumers’ response to our research on which aspects of their financial life would drive them to the branch more often:

- Notary services

- Coin counting machines

- More drive through ATMs

- Safe deposit boxes

Only after these options did consumers agree that two aspects of their experience were tied to customer service and support – the traditional assumption of branch visitations. 31% of consumers shared they would come to a branch more often if there were additional relationship managers and 30% if there were private consultation rooms.

When focusing on just those consumers 42 and under (Gen Z and Millennials), their ways into a branch are tied more to amenities than transactions. Their interest for certain experiences was much higher than Gen X and Baby Boomers on five key options:

- Multilingual services

- Financial education opportunities

- Free Wi-Fi and chargers

- Flexible layout with lounge area

- Community event offerings and workshops

Are you preparing for the next wave of branch interactions? These spaces will be more aligned to coffee shops and libraries than bank branches. Based on the research, the next iteration of face-to-face visits will be surrounded by comfort and peers, rather than transactions which can simply be done on their phone.