Consumers are increasingly chopping up their financial lives, distributing bits and pieces among a wide range of providers. The beneficiaries of this trend are most often the biggest financial brands that have invested in advanced digital solutions, large big tech organizations that have expanded financial service offerings, and fintech firms that have created digital solutions that appeal to well-defined (and sometimes underserved) consumer segments. Without decisive shifts in existing business models and investment in compelling digital solutions, there is no reason to believe that consumers will stop their diversification of financial service providers, putting existing revenue streams and potentially the survival of many legacy financial institutions at risk.

In a world of decreased branch visits and increased digital activity, convenience is no longer defined by geography. Convenience has been redefined based on simplicity of engagement, speed of delivery, and contextuality (personalization) of solutions. More importantly, both the depth and value of relationship are growing dependent on the number of digital engagements initiated by a customer. And the number of engagements depends on the value of these experiences. Therefore, it will be imperative that financial institutions optimize each touchpoint of a customer journey to bridge the gap between customer expectations and the current delivery of products and solutions.

Finally, it is important to note that not all consumer segments are acting the same, with segments no longer being defined solely by age and income. Segment behavior varies significantly based on digital use across all industries, with the most at-risk households being those that are the most digitally adept.

As Digital Adoption Reaches Saturation, Focus on Engagement

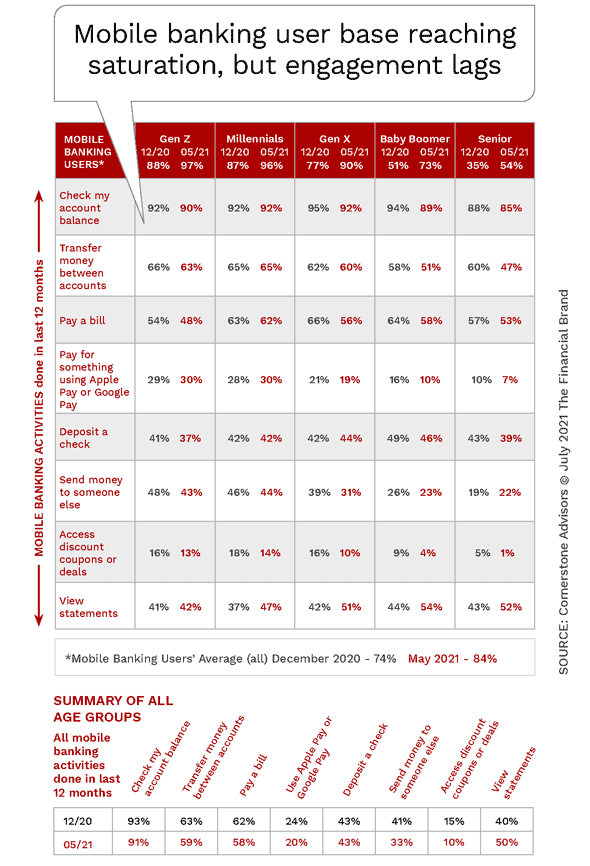

Recent analysis from Cornerstone Advisors indicates that the banking industry may be reaching saturation of digital adoption across the majority of consumer segments. Especially during the pandemic, when branches were closed, households become more comfortable using their mobile phone for balance inquiries and simple transactions. While some of the digital activity has dropped between December 2020 and May 2021, the number of users has increased.

That said, the same research shows that there is significant opportunity to grow the number and diversity of interactions beyond the basics. And, with branch activity at the lowest point ever, the need to focus on digital engagement has never been more important. This is especially true for recent adopters of digital banking. According to Ron Shevlin, Director of Research for Cornerstone Advisors, “As new users came on board in the past six months, they haven’t done many digital activities, dragging down the overall engagement numbers.”

Read More:

- Beyond Personalization: Three Reasons to Focus on Customer Journeys

- Digital Banking CX Boils Down to One Word: Speed

- Financial Institutions Benefit from AI, But Consumers Remain Skeptical

Bank of America Increases Digital Engagement to Build Loyalty

The deceleration of digital banking user growth at Bank of America illustrates how many banks may be reaching digital banking user saturation and that investment should be focused on increasing digital engagement to increase loyalty. According to bank data, the number of active users who used digital channels in the most recent 90-day period were up just over 3% YoY, representing 70% of Bank of America’s customer base.

Alternatively, the number of digital sessions (both mobile and desktop) at Bank of America grew 9.4% between Q2 2020 and Q2 2021. Part of this growth was attributed to a 31% growth in digital appointment setting by customers. More dramatic was the growth in interactions with BofA’s virtual assistant, Erica, where they increased by more than 150% YOY, to 94.2 million.

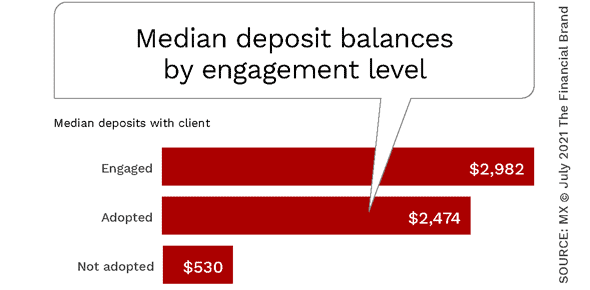

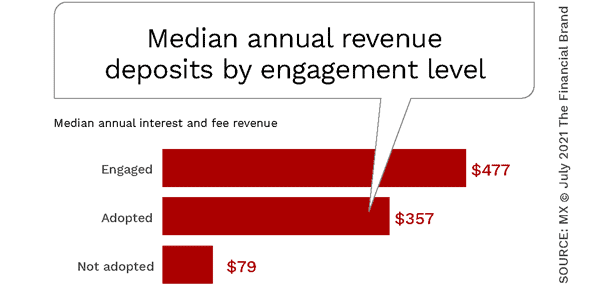

Digital Engagement Correlated to Increased Balances and Revenue

In a recent study by data-driven solution provider MX, it was found that both median balances and customer revenues increased as digital banking engagement increases. This correlation is important as financial institutions hope to retain consumers who are being lured by alternative providers.

But, digital banking activity can’t be forced… it must be earned.

Customers will increase their use of mobile and online banking if engagement is easy, fast and driven by a positive value transfer. Keeping customers engaged throughout their purchase journey develops customer loyalty and allows financial institutions to collect valuable customer information.

According to Gartner, “More customer interactions lead buyers to find your brand more valuable and provide you with customer insights. Those customer insights can inform marketing decisions such as re-targeting and content development, as well as sales processes such as messaging and outreach methods.”

Opportunities for Engagement Go Beyond Transactions

A financial institution’s engagement strategy should be based on what consumers want as they look for new financial institutions and what exiting customers want throughout their purchase journey. This analysis sets the foundation for trigger opportunities that include potential transactions, product offerings, and advice that help the consumer better manage their finances. These personalized interactions improve the customer experience and can build customer loyalty.

To build engagement, banks and credit unions must use data and customer insight proactively and meaningfully boost engagement across all channels. Communication must be relevant, timely, and illustrate to the intended consumer that your recommendation will provide value. Not only is timing and content important, so is the channel used to communicate.

Remember that content can go beyond sales messages, to include budgeting recommendations, financial wellness tips, and even local offers from neighborhood retailers. The goal is to get the customer engaged with your brand as often as possible … on their terms. Each engagement should help the customer’s progress along their financial journey, providing useful information or content that drives interaction, a positive experience and loyalty.