As any executive at a financial services firm knows, organic growth is hard to come by. The underlying fundamentals in most developed markets just aren’t favorable.

Growth in population and household incomes in most markets is low. Millennials are taking their banking, borrowing and investing needs to digital alternatives, and investment firms are seeing the end of the Baby Boomers’ asset accumulation years. Outcomes tell the story – The top four U.S. banks’ consumer businesses grew revenue by 0.2% in 2015 and 0.7% in 2016.

Every year, financial services firms invest billions of dollars in marketing and customer experience improvements that do not produce significant results. Products and services are commoditized and innovations are short-lived. Cross-sell ratios are stagnant, and aggressive sales tactics and quotas are no longer a viable strategy. Institutions have no choice but to attract more customers and serve more of their needs. But how?

The key to differential growth is connecting with clients at an emotional level. Appealing to customers’ deepest emotions is far from a new idea – but big data and technology now allow what was once marketing art to become business science. To do so, customers’ emotions must be objectively defined, measured and modeled to predict the most profitable behaviors.

Emotional connections can drive increases in customer lifetime value of as much as 800% for financial services firms. An emotional connection occurs when customers connect their deepest motivations, values and aspirations to a brand.

When customers feel a financial institution helps them realize such personal values as achieving social acceptance, attaining freedom and independence in life or simplifying life in a complex world, they have an emotional connection to the institution. These types of unspoken emotional needs – typically not captured in traditional market and consumer insight research – are the strongest drivers of customer value in the industry.

Read More: Banking Needs a Customer Experience Wake-Up Call

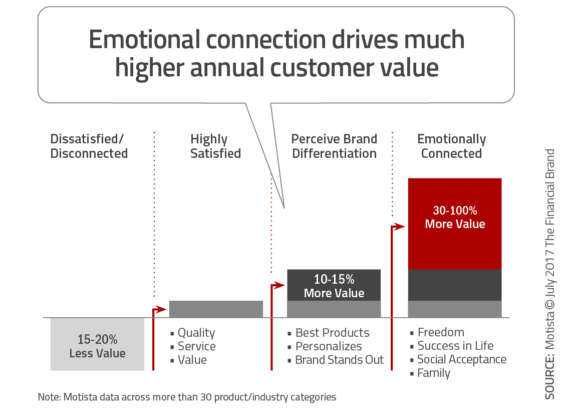

How Emotional Connection Drives Customer Value

We’ve seen that emotional connections follow a predictable pathway that falls into four main customer categories, each of which delivers significantly different value.

The above chart shows ranges of annual customer value, with “highly satisfied” as the baseline. Emotionally connected customers are anywhere from 30%–100% more valuable annually depending on the industry or category. This difference is especially high in financial services, where differences in year-to-year retention drive orders of magnitude multiples in customer lifetime value.

If all you measure is customer satisfaction, the above chart would only have two columns – satisfied and dissatisfied. This view often leads banks to focus marketing spend on their dissatisfied or low Net Promoter Score customers. While some customers are dissatisfied with a particular bank, most are actually disaffected with the category at large.

In either case, the investment required to move ta consumer up to ‘satisfied’ has a much lower return than focusing on customers who are already emotionally connected (to consolidate their business with you) or highly satisfied (if they show a propensity to become emotionally connected).

Across all categories of consumer financial services – retail banking, credit cards, home lending, personal lending, and brokerage and wealth management – emotional connection leads to significantly higher customer value and greater ROI on customer-facing investments.

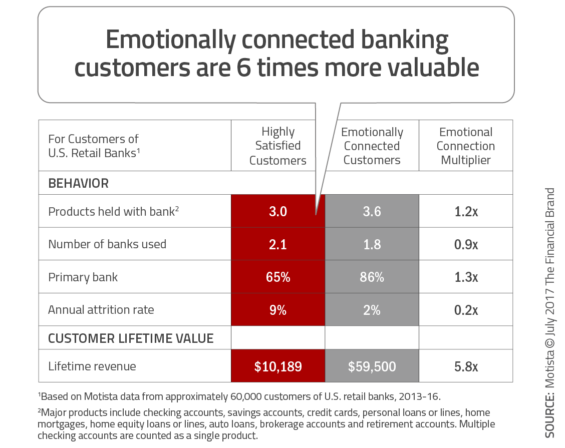

RETAIL BANKING

Emotionally connected retail banking customers hold more products, concentrate more of their balances and remain customers much longer when compared to customers who are [only] highly satisfied.

As the above multiples show, what all of this adds up to is that emotionally connected customers generate lifetime revenue nearly six times that of highly satisfied customers.

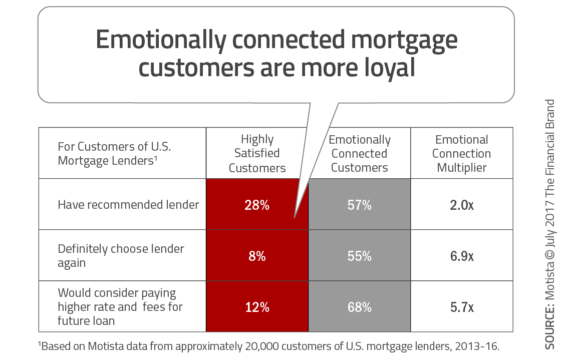

MORTGAGE LENDING

Emotionally connected mortgage customers recommend their lender twice as often as highly satisfied customers, and are six times more likely to choose their lender again even if it means paying a higher rate or fees than a competitive offer.

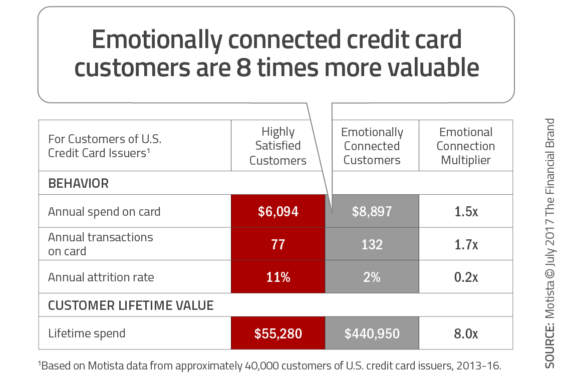

CREDIT CARDS

Emotionally connected credit card customers spend 46% more annually than those who are ‘just’ highly satisfied, carrying fewer cards and having an attrition rate that is significantly lower. As a result, their lifetime value is eight times higher.

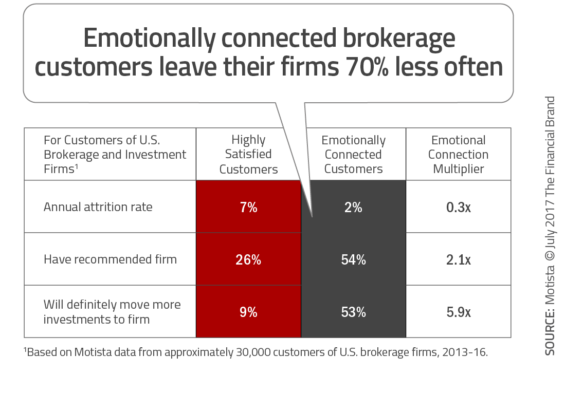

BROKERAGE

For brokerage firms – both full-service and self-directed – emotional connection drives retention, asset concentration and advocacy. Among emotionally connected customers, attrition is 70% lower, and intent to consolidate assets is six times higher.

Activating the Emotional Connection Opportunity

Given the value of emotionally connected customers, there is opportunity for almost any firm to drive growth if they can move customers into this preferred zone. The starting points for different institutions can be quite varied.

A growing number of financial institutions are now tracking their emotional connection. They know, to paraphrase the old management adage, “what gets measured gets managed.” Leaders of these firms know that managing their emotional connection yields customer value and profitable growth.

Case Studies

Here’s how a few case studies on how emotional connection can drive growth and competitive advantage.

NATIONAL BANK: USING EMOTION TO DRIVE CROSS-SELL

One bank’s ‘Emotional Connection Score’ was benchmarked at 28%, meaning 28% of its customers were emotionally connected. A “size-of-prize” model estimated a $300M–$475M annual revenue opportunity associated with monetizing existing emotionally connected customers and growing their population.

With a focus on cross-sell as a path to growth, the bank deployed predictive analytics to identify a particularly valuable segment of customers whose emotional motivations and aspirations made them predisposed to connect with the bank.

The bank’s current messaging emphasized security, product breadth, service and convenience, common advertising claims for the bank and its competitors, but not actual predictors of cross-sell success. Instead, to increase the purchase of additional products, customers needed to connect different emotions to the bank, such as:

- Reflects My Lifestyle: When customers feel their lifestyles – their aspirations, challenges and complexities – are understood and reflected by the bank.

- Belonging: When customers feel a sense of belonging with other customers of the bank.

- Admire Me: When customers feel they are more respected and ultimately more admired by their families and friends through their financial decisions.

Armed with these insights, the bank set about tailoring the experience to these key customers’ emotional needs. When these high-potential customers were researching, comparing and then applying for home mortgages, personal loans and brokerage accounts, live advice and consultation boosted the emotional connection and conversion. As a result, the questions asked by branch and call center teams, and the pacing with which reps communicated product information, were all designed and tested to deliver on these emotions.

The bank’s team also used emotion-based analytics to prioritize high-impact marketing touch points, learning that specific social media content represented the most valuable opportunity to connect emotionally with the high-potential segment.

Positive cross-sell results began to appear six months into implementation. Within two years:

- Average products held by the target segment increased from 4.3 to 5.4.

- Average annual revenue per customer improved from $1,290 to $1,730, reflecting both product and balance concentrations.

- Average tenure for these customers rose to 6.8 years from 6.1 years.

The bank has grown its annual revenue associated with the 900,000 customers in this segment by 35% – from approximately $1.2B to $1.6B, – in line with the initial projection. The segment’s lifetime revenue has grown by 49% – from approximately $7.1B to $10.6B – reflecting the significant benefits of both higher annual revenue and longer tenure.

CREDIT CARD ISSUER: PROFITABLY GROWING REVENUE WITH MILLENNIALS

A leading card issuer was struggling to grow revenue with its increasingly important Millennial customers. Entertaining advertising, targeted digital and social media marketing, an overhaul of the rewards program, aggressive teaser rates and major upgrades to the website and mobile app had not resulted in expected growth.

The issuer discovered that Millennial customers who felt an emotional connection to the card issuer transacted with their cards 52% more often, used their cards as their “primary card” 26% more often and closed their accounts with the brand 80% less often.

Big data analytics revealed that two emotions had a particularly powerful impact for the brand with Millennials

- Improving the Environment: When Millennials feel a particular brand – including a credit card brand – helps them do so, they become heavy and loyal users.

- Fitting In: Brands that help Millennials fit in with friends and colleagues become the beneficiaries of profitable behaviors.

Based on these key emotions, the product managers designed and launched one of the industry’s first credit cards centered on environmental causes. Cardholders would accrue rewards that could be converted into contributions to environmental charities or purchases of environmentally friendly merchandise and experiences, enabling Millennials to give back to the environment just by swiping their cards and enhancing their sense of fitting in with their environmentally conscious social circles.

A microsite about the card, direct mail and digital advertising were developed and tested to deliver the key emotions. Video content on social media sites featured early customers of this new card testifying as to how using the card in their everyday lives helped them fulfill their personal goal of improving the environment.

This card for Millennials remains one of the most successful product launches for this issuer. One year after in-market implementation, transactions were up 30% among Millennials versus the pre-launch baseline, rising to 70% by the end of year two. Primary card usage among Millennial customers increased 65% over two years. These significant increases in usage (the result of growing emotional connection) translated into impressive gains in lifetime customer value.

Additionally, the strategy ignited growth in new Millennial customer acquisition. New account growth among Millennials expanded 26% in one year, hitting 40% at the end of year two (again versus the pre-launch baseline). These Millennials churned at slower rates after three, six and twelve months, while ramping their card transactions at a faster rate than historical averages.

BROKERAGE FIRM: DRIVING RETENTION AND ASSET CONSOLIDATION WITH AFFLUENT CLIENTS

A market-leading brokerage firm sought to grow the portfolios of customers holding at least $250,000 of assets with the firm. The marketing and customer experience leadership teams learned that emotionally connected clients left the firm 55% less often than highly satisfied clients, while recommending the brand twice as often. Moreover, 49% of emotionally connected clients indicated a strong intent to increase assets with the firm, as opposed to just 8% of highly satisfied customers.

For one high-potential segment – affluent baby boomers with high investing IQs who were prone to combining advisor and self-service channels – analytics focused the team on three critical emotions that had the biggest impact on asset consolidation and customer retention:

- Helps Me Stand Out: The desire to look smart and enhance their friends’, colleagues’ and family members’ perceptions of them.

- Makes Me a More Interesting Person: Seeking to use their knowledge of and experience with investing and markets to become more interesting people.

- Brings order and Structure to Life. The desire to simplify lives that are complicated by juggling the demands of professional careers, teen or college-aged children and aging parents.

The firm assessed nearly 100 customer touch points for their impact on the key emotions. Specific content touch points emerged as opportunities.

Podcasts and videos prepared by the firm on specific investing topics of interest to the client led to deeper emotional connection. The same was true for invitations for clients to attend both in-person and online seminars. These touch points aligned to these clients’ desire to ‘stand out’ and ‘be more interesting’ through investing knowledge and experience – even though they were not the touch points clients reported as most important.

The next set of touch points focused on the advisor-client relationship. The analytics showed that unsolicited, empathetic check-ins from the advisor – through email, texting and social media – grew emotional connection.

Video conferencing with an advisor, especially at night or on the weekend, also deepened connection, especially driving the ‘order and structure’ emotion. While the firm’s advisors had been cautious in pushing insurance to clients, analytics determined that unsolicited inquiries about life, long-term care and personal disability insurance – when empathetically delivered – elevated the emotional connection score with these clients.

The marketing team used these insights to:

- Inform the creation and testing of new digital content to deliver on the key emotions, including Podcasts, social videos and videos on the firm’s site and mobile app.

- Evolve and test the “skin” of the firm’s websites and mobile app, including the usability, imagery and messaging.

- Stimulate conversations likely to grow Emotional Connection through social media properties, such as Twitter and Facebook.

The firm has accelerated its growth rate among affluent clients from 3.1% to 3.9% over two years. The number of affluent clients leaving the firm fell 12% during the period, further increasing profitability and lifetime value. The team continues to set new growth goals and to measure and manage emotional connection as the path to achieve these goals.

Leverage Your Emotional Connection Asset

Financial institutions must generate organic growth to drive long-term shareholder value. Competitive pressures are intense, marketing dollars are precious and customer experience investments need to show returns.

Customers are waiting to bring more of their business to the institution that doesn’t just satisfy their product and service needs, but resonates with and fulfills their underlying motivations and desires.

Every institution’s emotional connection asset already exists, but few are being leveraged for growth. The most successful institutions are looking beyond traditional competitive tactics and customer satisfaction metrics to emotion-based strategies to drive their future success.