If you want a good capsule description of how the COVID Recession has hit many Millennials, you can’t do better than “toxic storm.”

That phrase comes from Ana Kent, Policy Analyst at the Federal Reserve Bank of St. Louis, in a podcast. A Millennial herself and a member of the Fed bank’s Center for Household Financial Stability, Kent has made a specialty of studying the generation. She summarizes the storm this way:

“Millennials are old enough to have been negatively affected by the Great Recession. But we’re also young enough to still be early to mid-career still when the COVID-19 pandemic hit. Meaning that we’ve been doubly hit in just over 12 years… . And what this means is that we were economically vulnerable going into the pandemic … than older generations of similar ages and little to no buffer for many.”

Kent adds that the attitude that each generation should sink or swim on its own efforts “while it’s very American, often ignores the fact that the tide is stronger now and many Millennials are swimming upstream.”

The tide she describes includes income levels that started comparatively low as a result of the Great Recession, home prices that rose at a higher rate than did salaries, skyrocketing student debt — compounded in some cases by the decision to go to grad school instead of going right into the poor job market, and increasing responsibility for health care costs and retirement savings in the modern business environment.

In a blog, Kent suggests that, in the wake of COVID-19 and the economic slump, many Millennials might become part of a “lost generation” in financial terms, a group that overall has spent much of its collective life attempting but failing to reach common economic goals.

“The financial obstacles Millennials have had to deal with have not always been their fault,” agrees Anuj Nayar, Vice-President and U.S. Financial Health Officer at Lending Club. In fact, he notes, “when faced with the option of save or pay down debt, many Millennials choose to pay down debt. That’s the reality of where we are today. Financial institutions that recognize this and don’t capitalize on that debt will thrive.”

Nayar questions the thinking of lenders who still see Millennials as a vast market for plastic. “They aren’t looking for credit cards that they’ll revolve on or products that will keep them deeper in debt,” says Nayar. “Giving someone who is in debt already a credit card is like feeding sugar pills to a diabetic.”

The Financial Brand dug into statistics about the Millennial generation’s financial challenges and asked a quartet of experts how financial institutions can better serve Millennials.

Here’s why financial marketers must get this right: In July 2020, the U.S. Census confirmed that, based on mid-2019 figures, Millennials have surpassed Baby Boomers. They now rank as the largest generation of Americans. While the following generation — Gen Z — may be the customers of tomorrow, Millennials, both by number and age, are the primary customers of today. (Pew Research Center defines Millennials as people born between 1981 and 1996.)

Millennials Just Can’t Seem to Buy a Break

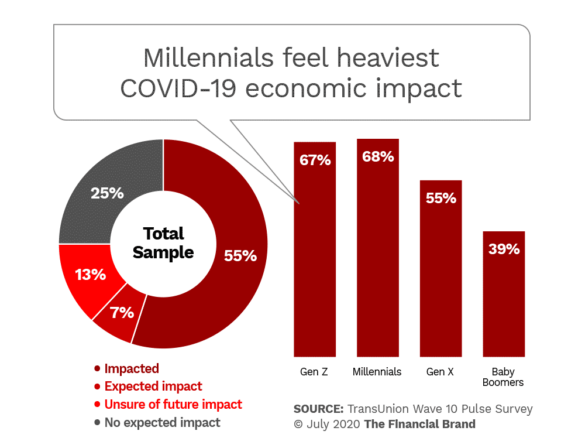

Just over half — 55% — of all Americans told TransUnion that they had been impacted by the COVID recession, but younger consumers were hit much harder. The lockdown recession has hit nearly seven out of ten Millennial, just edging out Gen Z.

86% of Millennials — much higher than any other generation — currently worry about being able to pay bills and loans, according to TransUnion. The greatest concern, among 40% of Millennials, is over paying credit card bills. TransUnion also found that Millennials have received credit relief of one kind or another more than any other generation during the COVID period.

The coronavirus recession hit Millennials when many were already just getting by, according to John Thompson, Chief Program Officer at Financial Health Network, a nonprofit organization supported by many financial services providers. Thompson says that the group’s 2019 U.S. Financial Health Pulse consumer survey — conducted prior to the pandemic and the shutdowns — classified only 24% of Millennials as “Financially Healthy.” The organization defines this as being when consumers save, spend, borrow and plan in ways that allow them to be resilient in the face of the unexpected.

By contrast, Thompson continues, 54% of Millennials were “Financially Coping” before COVID-19, that is, struggling with at least some aspects of their financial lives. And 22% were “Financially Vulnerable,” grappling with most, if not all, facets of their financial lives.

The Deloitte Global Millennial Survey 2020 found that one out of five Millennials around the world had been put out of work by early May and one out of four younger Millennials (25-30) had lost their jobs or been furloughed. Over one in four Millennials were working fewer hours. The study found that just one in three Millennials had not seen their employment or income status affected as a result of the disease.

And it’s likely the full brunt of the COVID recession hasn’t been felt yet by this generation or any other. In the U.S. the effects of the pandemic on the economy have been partially buffered through mid-summer as a result of federal stimulus payments, lower costs due to living and working at home during lockdown, bolstered federal unemployment payments through the end of July, and the Paycheck Protection Program.

Read More: Why Millennials and Gen Z Love Megabanks

COVID Makes Millennials a Moving Target

The Deloitte study indicates that many Millennials feel they are financially responsible:

- “I actively budget my money so that I know how much I can spend over the week/month.” 74%

- “I feel that I have the right level of knowledge to make informed decisions about my finances.” 72%

- “I feel confident making decisions about financial products and services. ” 69%

- “I have set myself clear financial goals for my long-term future.” 64%

- “I have set myself clear financial goals for the next five years.” 62%

This part of the study was based on polling before COVID hit, and underscores that continuing employment provides a base for the confidence reflected in the findings above. Take away steady income, however, and the best plan can blow up.

Strong pre-COVID and lockdown attitudes may be changing drastically, something no planning would have anticipated. While it is early to say for sure, key assumptions and observations about Millennials may flip in the post-COVID period. With urban unrest rising, their preference for living in cities may change, and there are already indications that this generation’s expressed disinterest in owning cars is already reversing.

While Millennials favored mass transit and ride sharing before the pandemic, health concerns may shift that. Research by Capgemini early on in the pandemic found that many people expressed a preference for private transportation out of health concerns. While 35% of all consumers surveyed in the U.S. and additional countries were considering buying cars, 45% of people under 35 were thinking about buying one.

However, Capgemini found that over half of younger people who say they are not in the market to buy a car say that it is because they can’t afford one — 57% of 18-24 year olds and 51% of 25-35 year olds.

Millennials Are Not Your Former Typical Young Adult

Financial marketers and others in banks and credit unions have been talking about Millennials for such a long time that they’ve sometimes lost track of the fact that these aren’t “kids” anymore. (Some marketers need to update their photo libraries.)

But something not fully appreciated is that for many Millennials their economic status, even pre-COVID, has held them back on some basic life steps.

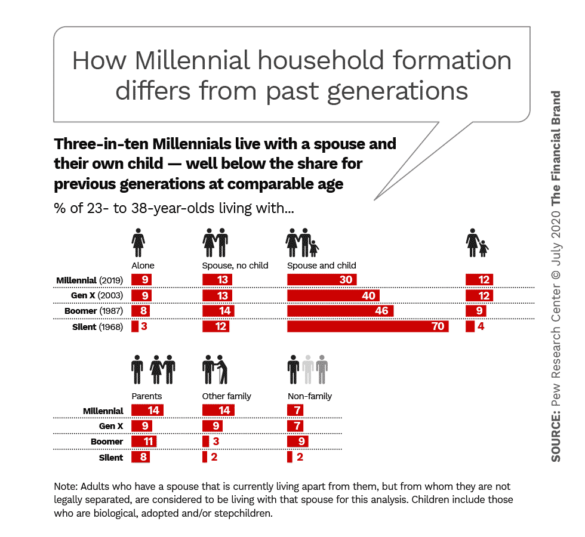

An analysis by Pew Research Center has found that Millennials’ formation of traditional households consisting of a spouse and a child or children has dwindled compared to older generations. As shown in the chart below, 70% of members of the “Silent Generation,” between the ages of 23-38, lived in traditional households. That percentage has dropped with each generation, but among Millennials, less than a third live in such households. 14% of Millennials still live with their parents, in some cases having moved back during economic stress. Another 14% live with other family members besides parents.

“A majority of Millennials are not currently married, marking a significant change from past generations,” states Pew Research in an article. “Only 44% of Millennials were married in 2019, compared with 53% of Gen Xers, 61% of Boomers, and 81% of Silents at a comparable age.” When they do marry, Millennials marry older — men around 30, women around 28, according to Pew. The data indicates that 12% of Millennials were living with an unmarried partner.

Read More: Why Financial Institutions Must Overhaul Their Retail Banking Strategies

What Can Banks and Credit Unions Do to Help Millennials?

Financial Health Network’s John Thompson says it’s critical for banks and credit unions to understand that they can’t solve Millennials difficulties by themselves.

“Financial health is a complex and interconnected state,” says Thompson. “Access to a quality job and stable income, access to benefits, healthcare, education — all of these and more have a role to play.” Financial institutions can make an effort to engage with other companies to influence those other areas, for example, he adds.

There is also a danger, in setting out to help this generation, to put too much reliance on the grouping itself as a basis of trying to help. Several experts contacted by The Financial Brand noted that Millennials are not a single, uniform mass.

“Millennials are an ever-elusive generation — there is really no one-size-fits-all definition,” says Jesse Mecham, CEO and Founder of You Need a Budget (YNAB). “Therefore, there isn’t one solution.” Mecham, a Millennial himself, developed budgeting software that he and his wife used to stay solvent while in college. It became the basis of his company.

“Companies need to think in terms of micro-demographics,” Mecham states “They need to understand the Millennial generation’s diversity and speak to the unique pockets within it. ”

Just a few of the slices of this market, according to Meacham:

- Millennials who graduated at the height of the Great Recession.

- Established professionals who are now beginning to take responsibility for the care of their parents.

- Millennials that are getting married, buying a house or starting a family.

Institutions that discern the differences “are the ones that will make lasting connections,” says Mecham.

Achieving that understanding requires more than an intensive round of research. Even though the oldest Millennials are nearing 40, many banking institutions still operate from a Boomer/Gen X mindset.

Lending Club’s Nayar thinks the product lineup and marketing of many traditional institutions needs a good shaking up. “Traditional financial institutions today function more like warehouses for your money,” says Nayar. “What consumers, especially Millennials, want is greater flexibility in their offerings.”

“Banks would be smart to make a point of promoting Millennials into key roles and assigning them to projects about the future of the institution and its technology,” says Jo Ann Barefoot, a consultant and fintech founder. She’s also mother to two Millennials.

Building the Right Kind of Content Will Build Bridges with Millennials

Barefoot says the knowledge of how to handle money isn’t there, for many Millennials.

“My kids wish they had been taught it in school,” says Barefoot, “and they weren’t. They have said that they wouldn’t have even known to pay off credit card bills every month if I hadn’t taught them so.”

But today a classroom isn’t the place to do the teaching — the mobile phone is. Specifically, Barefoot thinks money management apps can help show Millennials how to handle their finances in real time and how to search for the best products while avoiding scams.

“Millennials do their research. They want transparency, access and authenticity,” says YNAB’s Mecham. “They want recommendations from trustworthy sources. So what can a financial institution do to reach Millennials? They need to build trust. They can do that by being genuine and providing valuable educational content for free.”

“Millennials are facing a very real financial health crisis and banks, credit unions and fintechs have an opportunity now to not pay lip service to it, but instead to take meaningful action to help Millennials save, borrow responsibility and plan for their futures,” says Anuj Nayar of Lending Club.

The more institutions can personalize their approach to Millennial consumers, the better they’ll do, he adds. Personalizing assistance to offer hardship plans, payment deferral plans, “and products that can help consumers smooth their income and save more” will be on target, he adds.

‘It’s About Products, Not About Content’

Not everyone contacted sees content as a major assistance to Millennials.

“Content is an asset, but it is certainly not the answer,” says Financial Health Network’s John Thompson. “While useful as a component of services, the financial health of Millennials won’t be materially advanced by more financial education.”

Thompson believes that the answer to helping Millennials best lies in product design. He points to pre-COVID research by his organization that found that only 14% of Millennials felt strongly that their primary financial institution helped them to improve their financial health. He thinks it will take more than interesting content to change that impression.

“Financial institutions can no longer afford to simply offer products and hope that prospective customers are ‘financially literate’ to know they need a solution, find the right one, use it the right way and achieve their goals,” says Thompson. “Rather, financial institutions must design with an explicit mission to improve outcomes.”

Cultural issues must also be considered. Thompson says that financial health continues to be divided across racial and ethnic lines, the result of “decades of discriminatory policies that have made it far harder for non-white Americans to build and transfer wealth to future generations.”

Read More: Banking Must Take A Stand On Tough Social Issues

Stop Thinking Like a Boomer and Step into Millennials’ Shoes

Experts suggest that partnerships with fintechs will help, but it’s not always just about the tech. It can be as much about perceptions and ways of thinking.

“Millennials appreciate humor,” says Jo Ann Barefoot. “It’s a witty generation, enabled by the high volume of humorous material they exchange online. Fintechs are often funny and entertaining. Banks rarely are. In fact, to Millennials they seem boring. Boring can be good when the focus is on security, but it doesn’t attract people for their day-to-day needs.”

YNAB’s Mecham says banks and credit unions run by Boomers and Gen Xers have to realize that Millennials aren’t willing to put up with pain points that they were.

“Millennials expect that complicated things can — and should be — made simpler,” says Mecham. “As a bank, whatever can be done to simplify their financial lives goes a long way.”