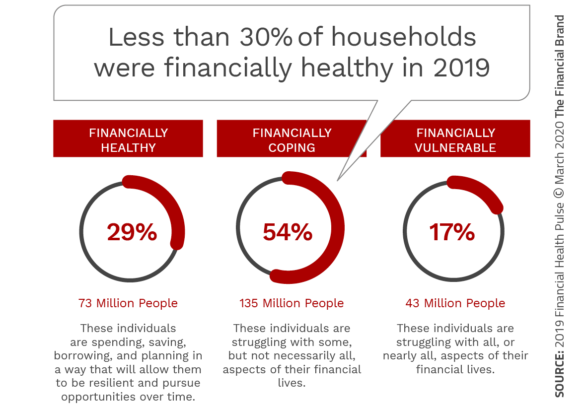

According to the 2019 U.S. Financial Health Pulse report, well before the current coronavirus crisis, less than 30% of Americans were considered financially healthy, with millions of households not having enough money in savings to get through a month. This highlighted that the majority of Americans were unprepared for short or long-term financial shock.These are the people who are the most at risk given today’s COVID-19 crisis.

What will happen to those who are impacted by a health emergency? What will happen if a third of the recent unemployed can’t find the same level of employment once this crisis subsides?

We already realize that the longer this crisis continues, the more loan payments will be missed, the more savings will be depleted, and the less money will be available for retirement. Underneath the obvious impact will be the reality that protracted and dynamic pandemic conditions will also draw out anxiety and financial stress impacting relationships and creating underlying phychosocial behaviors.

Unfortunately, things will get worse before they get better.

To get a better perspective on the impact of COVID-19, and the response required by both the banking industry and government to address the needs of households and small businesses, we interviewed Jennifer Tescher, the President & CEO of the Financial Health Network. This exclusive interview by the Banking Transformed podcast discusses the role of the Financial Health Network, Tescher’s mission to make more organizations aware of the impending crisis what needs to be done immediately and going forward to promote the financial wellness of all consumers.

Below is an abridged version of our interview with Jennifer Tescher.

Listen to the Jennifer Tescher Podcast

Can You Share a bit about the Financial Health Network?

Tescher: Our mission is to improve financial health for all. And, I emphasize the for all because financial health is relevant and important for everybody. It makes it relatable to everybody. But we are particularly concerned about the people who often get left behind, or who are most likely to have challenged financial health. So we want everyone to be able to have the opportunity to improve their financial health and ultimately live their best life.

How do you set out to accomplish your goals?

Tescher: A lot of people initially assume that we’re a direct service provider, working directly with people, but we don’t. We are about trying to get the business community to understand why it’s in their interest to invest in the financial health of their customers, their employees, and their communities. We run a membership network, with 160-plus companies that are mostly financial services companies of varying kinds and sizes.

We also run a consulting business to help design products and experiences and to evaluate whether what they’re doing is actually making a difference in people’s lives. Finally, we run an accelerator through our Financial Solutions Lab to invest in early stage fintech companies that are focused on solving critical consumer financial health challenges.

Is the government doing enough to support the financial wellness of consumers?

Tescher: The short answer is no. Even before this recent crisis, there was a need to understand that financial wellness is not just a poor person’s problem. Over the last 20 years, the story has been the middle class and just how little wage gains and growth they’ve seen, while at the same time everything in life has gotten more expensive.

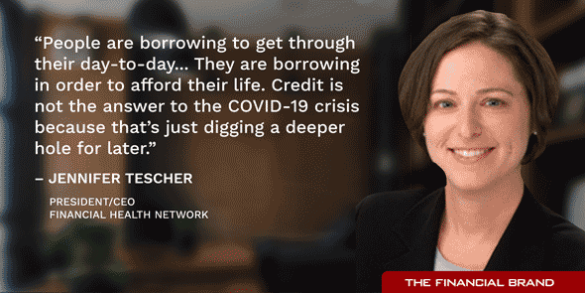

Even since the financial crisis 10 years ago, we’ve seen consumer borrowing go right back to where it was before. And that’s because people are borrowing to get through their day-to-day. They are borrowing in order to afford their life. They’re not borrowing to take a vacation or to make an investment in their future. And usually it’s NOT because they are living outside of their means.

And the one thing I can’t stress enough is credit is not the answer to the COVID-19 crisis because that’s just digging a deeper hole for later that folks aren’t going to be able to make up.

And, when you’re thinking about the broader national economy, that kind of negative downward spiral is what can drive a country into not just a little downturn, but a very severe recession and ultimately potentially a depression. So, I’m really heartened by what I’m seeing coming out of Congress. I like this idea that I’ve been hearing about small businesses being able to take a loan that can be forgiven if they keep their employees on the payroll.

How can the banking industry assist during this crisis and beyond?

Tescher: I’ve been really heartened by what I’m seeing, certainly relative to where we were 10 years ago in the financial crisis. Now this isn’t a financial crisis. This is a public health crisis and a financial health crisis for individuals. But I do think that the actions that I’m seeing banks take to give their borrowers relief – to allow them to skip some payments – I think is the right thing.

I’ve also seen the right signals from regulators giving banks the comfort they need, where taking those actions isn’t going to put them at risk from a regulatory perspective. We’ve even seen the regulators encourage banks to engage in more small-dollar lending.

And I think banks are really going to need to be willing to cash those government checks for anybody, regardless of whether they’re customers or non-customers, for free. We’ve really got to give as much access as possible to help people get this money into their hands in a spendable form as quickly as possible.

Is this a time of great opportunity for banking to improve consumer outcomes?

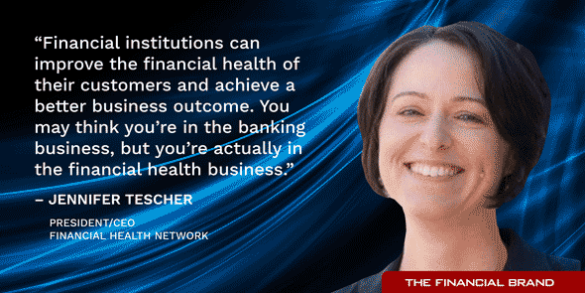

Tescher: This is a time when financial institutions can definitely improve the financial health of their customers for a better business outcome. I often say to banks, “You may think you’re in the banking business, but you’re actually in the financial health business”. That’s customers want from you – that you have their back as they’re trying to manage their lives.

Remember, people’s lives and their financial lives are one and the same, deeply interconnected. And if that’s not how you see yourself in terms of the business you’re in, then you’re not really speaking to your customer.

How do we deal with the longer-term impact on consumers?

Tescher: I think the triaging and the being able to deal with customers as individuals is going to be the most challenging part. Because so far, what institutions have done rightly is to create some broad policies. We’re waiving all fees for example.

But, as it comes to what would normally be considered collections or workouts, that’s got to be at an individual level. The last time the sector had to gear up for that was during the mortgage meltdown, and frankly they didn’t do such a good job. Banks are really going to have to gear up for the kind of customer service that they’ve been largely trying to push to digital channels and self-service help. A lot of these issues are not going to be self-service.

Is now the time banks should be going beyond credit bureau scores?

Tescher: I think that financial institutions are in a great position to be more thoughtful about how they can improve the financial health of their customers and how doing so is better for their ultimate business outcome. We have spent the last several years developing a measurement methodology around financial health. And we’re now working with dozens of firms that are using that framework and methodology to actually measure the financial health of their customers over time based on product usage, etc.

The financial crisis of 2008 demonstrated that when people’s finances went haywire, credit scores weren’t working at all to separate the good from the bad in terms of evaluating households. That’s when nontraditional credit data really took hold, because that data turned out to be much more useful in evaluating credit capability. So, non-traditional financial health data may be particularly useful as firms evaluate the impact of this crisis.

Can financial institutions do better helping consumers manage their money?

Tescher: There is a significant role for providers to play in helping people be their best financial stewards. I think there’s a lot we can do in how we structure products and experiences to help people be the best that they want to be … even if their brain is telling them to do the wrong thing.

Creating an app that crawls through your checking account and finds small amounts of money that a person would never notice being taken out and putting it into savings for instance.

With regards to gender inequity, what needs to change?

Tescher: We’re making strides, but this is a universal problem. I think it’s got to start all the way back in college and in banking education. We need to make sure that women are seeing opportunities for careers in finance and banking at the senior levels. We need to find ways to have more women in the industry so that we have equal pools of gender to begin with.

There are more than enough qualified women who can serve on corporate bank boards. We just have to have the will to actually make the changes.

I’ve seen banks start to get more comfortable with flexible work, whether that’s location, hours, etc. I think that’s actually going to be a silver lining of this crisis. The demonstration that a lot of work can be done from home or at differing hours. That should help knock down some of the barriers that keep women from continuing to rise in the ranks.

And then, I just think it’s sheer force of will. The fact that we have so few women on all corporate boards, but particularly in financial services, just needs to change … and it can, tomorrow. There are more than enough qualified women who can serve on corporate bank boards. We just have to have the will to actually make the changes.