The older portion of Generation Z — people born between 1997 and 2002 — have entered their college years and the workplace. Older and younger Gen Zers combined represent the second-largest generation in the U.S., and they already represent approximately 40% of the nation’s consumer purchasing power.

“Forget Millennials, Gen Z is the new golden child. With the oldest of this cohort entering the workforce, flexing their purchasing power and shaping strong opinions of the world around them, it’s time to take this generation seriously,” states a report by Porter Novelli/Cone.

The challenging thing about considering this generation is that the specifics of what it means to financial marketers is still solidifying.

“Generation Z has been called many things, but homogenous is not one of them,” states Raddon Research in a major survey. “This generation’s unique experience growing up amid the rapid evolution of personal technology and the resulting surge in accessible information have shaped their preferences as consumers, especially in the financial services sphere.”

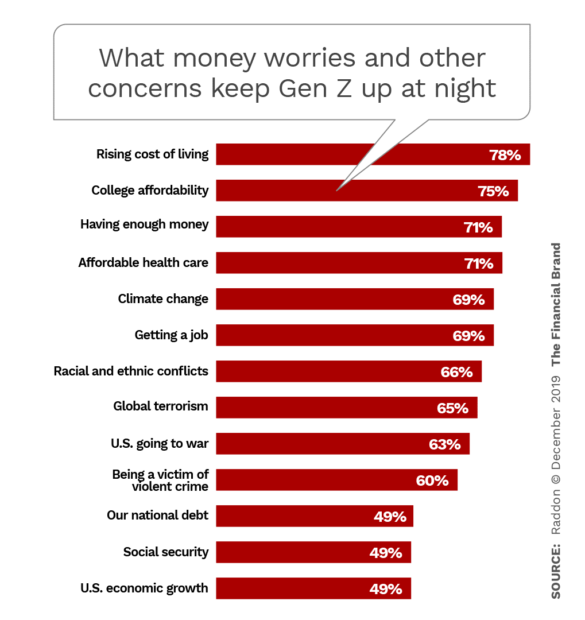

Raddon found that while the much-discussed interest among Gen Z in various issues and causes is genuine, this generation also has a strong focus on its own financial well being.

Morgan Stanley thinks the impact of younger generations on financial services is just beginning. In a commentary, the firm states that “as Gen Z ages into the key 25-to-40-year-old sweet spot for borrowing, they will combine with Generation Y (a.k.a. the Millennials, ages 22 to 37) and could reshape the financial industry in their tech-savvy, mobile-first image.”

While the older members of Generation Z know their technology, their confidence is much weaker when it comes to financial affairs. Over one in four Gen Zers (28%) see their own generation as not being financially responsible, for example, according to a study by Northwestern Mutual. Only 13% of this generation sees themselves as very responsible, financially — half the rate of the population at large. Multiple studies report that Gen Z has a deep desire to better understand money, though how it wants to learn about it may differ significantly from previous generations.

While some early commentary attempted to portray Gen Z as Millennials 2.0, this generation is rapidly turning out to be its own self, in some cases even inheriting attitudes from older generations, rather than Millennials.

1. Generation Z loves branches.

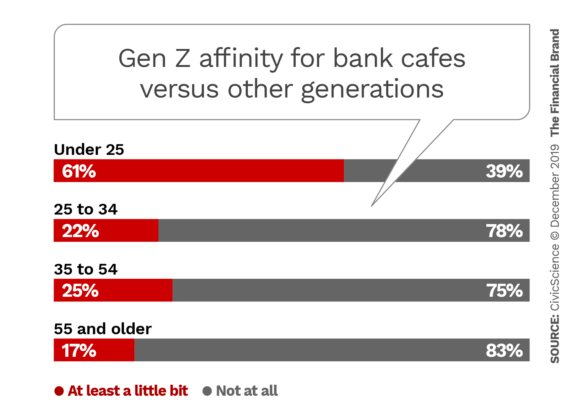

CivicScience studied consumers’ use of branches and found that Gen Zers are the heaviest users, often visiting them several times a week. This is greater than Millennials and quadruple the rate of people over 55. Why is a generation that knows smartphones, voice assistants and the Internet of Things remotely interested in going to a branch?

“Part of it may come down to the lack of zeroes they have in their bank account,” the marketing research firm concludes.

CivicScience found that there’s a strong correlation between feeling bad about one’s finances and visiting financial institution branches frequently, overall, and found that Gen Z feels least positive of all generations about their financial affairs.

But CivicScience says there’s another reason that is literally food for thought for financial marketers.

2. Start with free coffee and donuts.

The firm’s research found that 21% of consumers say they are offered something to eat or drink when they visit a branch — food, candy, or a drink. The thing of it is, CivicScience found that when it lined up frequent branch visitation with receiving free snacks, there was a strong correlation. And Generation Z consumers reported getting free eats at a much higher rate than any other generation — 32% get something to munch.

This is not just a statistical anomaly. CivicScience asked explicitly, and learned that for two out of five Gen Zers, it’s at least a little bit important to get snacks when they visit the branch.

“But it’s not just free food,” the report states. “It’s any food.”

3. Gen Z really likes café branches.

As the chart below shows, Gen Zers overwhelmingly favor the idea of branches that have cafés inside, that hold events and host other activities. The study also probed consumers for their feelings about the feeling of “community” instilled by branches, and found that while Baby Boomers and older consumers most strongly like that, the second-highest liking for the branch as community center came from Generation Z.

While consumers overall tend to stick with their financial institutions, the report notes, one in five Gen Zers would switch.

“Taking into account free food and community, perhaps a free cup of coffee and the opportunity to buy a croissant — assuming all else is equal — might be all it would take for a bank to gain a young customer for life,” CivicScience conclu

Is a generation’s loneliness playing a role here? Several other pieces of research support the importance of a feeling of community to Gen Zers. One, from Cigna and Ipsos, finds Gen Z to be the loneliest generation, with nearly half of those surveyed saying that they feel alone, isolated, left out and without anyone to talk to. Nearly 70% of Gen Zers surveyed say they feel no one knows them well — ironic given that electronically they are the most connected generation. It’s possible that the idea of a place where you can go and see other humans fills a need devices don’t. Perhaps banks and credit unions have something to build on there.

Also this: According to research by PiperJaffray, food continues to be the top spending category for male Gen Zers.

Read More: Massive Forces Impacting the Future of Bank & Credit Union Branches

4. Gen Z has a tendency towards frugality and moderation.

The Porter Novelli/Cone analysis suggests that witnessing the Great Recession’s impact on their parents when they were quite young left a mark on Gen Z.

“For this reason — and in contrast to Millennials — this generation is both pragmatic and competitive,” the firm observes. “No handouts or participation trophies for this group. They value hard work and seek to create meaningful careers, but are also marked by a sense of frugality not seen among experience-seeking Millennials. There is also research showing this tendency toward moderation extends beyond budgeting.”

One small indicator of frugality: While all generations make some use of online coupon codes, virtually every Gen Zer surveyed by Coupon Follow tries to find codes before buying. More than any other generation, they use browser add-ons to automatically seek online coupons before buying. And a Business Insider study indicates that they shop price over brand.

Yet financial awareness isn’t complete. While Gen Z has more of a tendency to save than Millennials, this generation doesn’t always have a handle on where their deposited savings stand. Three out of five (57%) of Gen Zers surveyed by Northwestern Mutual were unsure about their personal savings. The same research found that only about one in three Gen Z consumers have developed a good sense of the balance between spending now versus saving for later needs.

But they get the concept, at least. “Even at a young age,” reports Raddon, “members of Gen Z are focused on saving the money they earn … among those who already have a job, saving money was cited as the top reason for working.”

Read More: How to Grow Deposits in a Weird Rate Environment

5. Gen Z adults have respect for credit and are already using it.

Lending Point reports that the average FICO score seen among a very large sample of Near Prime loan applications was highest among Gen Zers. That generation averaged a score of 637, superior to Gen Xers’ 632 and Millennials’ 629. While Gen Z on the whole is just getting into its credit using years, multiple studies have found that they are using certain types of credit.

How Gen Z credit compares to other generations

| Generation | Avg. FICO Score | Avg. Debt-to-Income | Avg. Income | Avg. Loan Request |

|---|---|---|---|---|

| Gen Z | 637 | 9.90% | $47,825 | $8,462 |

| Millennials | 629 | 16.40% | $60,606 | $11,058 |

| Gen X | 632 | 17.50% | $71,578 | $11,918 |

| Boomers | 645 | 18.80% | $69,178 | $11,928 |

| Silent | 657 | 18.90% | $63,905 | $11,479 |

Source: Lending Point

Lending Point’s research also found that that while Gen Z is part of the resurgence of personal loans — brought on in part by the advent of online fintech lenders — the youngest adults are using this credit differently. Overwhelmingly, as the table below shows, Millennials and Gen Xers use personal loans to consolidate credit card and other debt — essentially a credit reboot. Gen Z, on the other hand, tends to use personal loans for explicit credit needs, such as a major purchase.

What Gen Z wants personal loans for

| Generation | Debt Consolidation | Major Purchase | Healthcare | Auto Needs |

|---|---|---|---|---|

| Gen Z | 58% | 25% | 3% | 5% |

| Millennial | 81% | 9% | 2% | 2% |

| Gen X | 80% | 6% | 2% | 2% |

| Boomers | 78% | 5% | 2% | 2% |

| Silent | 74% | 5% | 3% | 2% |

Source: Lending Point

6. Gen Z still has a lot to learn about using credit.

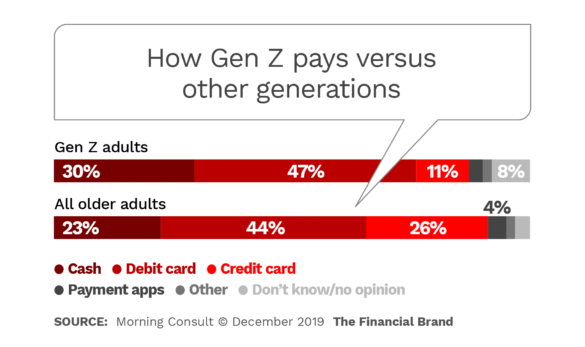

Experian surveyed a group of recent high school graduates ages 18 and 19 and found that while three in five had checking accounts, only about a third had a credit card. Gen Zers are still fairly light users of credit cards, typically still paying in cash or via debit card, according to research by Morning Consult.

The Experian study found that only 19% of the recent graduates polled felt they have a good understanding of credit generally. About two thirds said that they had not received any education on personal finance in school and even those that had taken a course had questions on finance.

Of those who had never had a class, 43% said they want to learn to save, 38% want to learn to manage their expenses, and 36% want a class that teaches them how to file their taxes.

Financial worry is widespread. Multiple studies indicate this. Logica Research reports that 47% of Gen Z has some non-mortgage debt, compared to 68% for Millennials, 70% for Gen X and 67% for Baby Boomers, and that money stress is an issue for 72% of Gen Z. One point from Experian is that about half of those surveyed say they are concerned about having enough money to do what they enjoy later in their lives.

7. Gen Z wants to be taught — but innovatively.

Clearly, research indicates that while Gen Z wants financial education, it doesn’t actually want to sit down in a classroom somewhere for a lecture in classical school style. Studies make the point that this is a generation that views more than it reads. That means that to the extent that financial marketers can reach out in some other way, the more they can be perceived as financial home base.

“As fintech and big tech players expand their payments functionality, banks will need to be invested in teen banking — or risk being left behind.”

— Morgan Stanley report

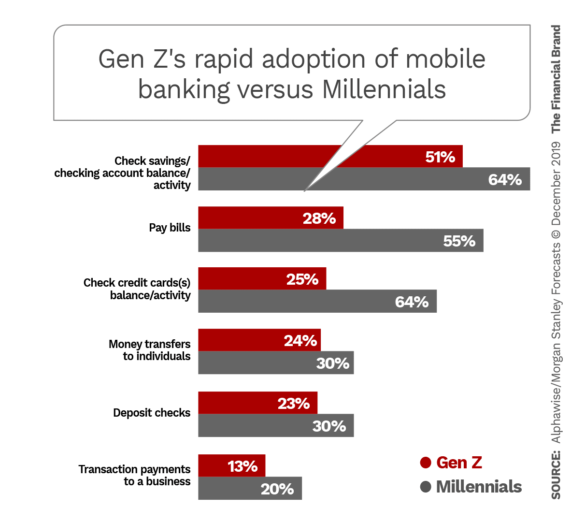

Morgan Stanley makes an important point in the blog mentioned earlier. Some Gen Zers get cell phones as early as 10 and they can have a social media account at 13. Yet typically they don’t have a bank account until they are 18. The firm suggests that with a generation that has rapidly taken up mobile banking when it comes of age, this misses a big opportunity to provide a teen mobile account for younger Z’s.

“This includes sending and receiving money and paying at the point of sale and online with their phones,” the blog states. “As fintech and big tech players expand their payments functionality, banks will need to be invested in teen banking — or risk being left behind.”

“These accounts would allow younger users to learn how to monitor their own budgets and spending, all with a parent’s permission and ability to monitor the account,” says Betsy Graseck, Global Head of Banks and Diversified Finance Research at Morgan Stanley. “While several banks offer this today, they are more the exception than the rule.”

8. Gen Z likes the idea of gig work, but not the lifestyle.

The gig economy has much appeal for Gen Z in the forms of schedule flexibility, the perception of being their own boss, and not having a supervisor or co-workers. But an international survey by Kronos indicates that the flip side — lack of stability and unpredictable pay — make Gen Zers nervous. While just over half would like to live on gig employment, less than half actually do gig work and only 10% do so exclusively. For the most part Gen Z likes the structure of traditional employment.

The leading “side hustles” for Gen Zers, per the Logica research: selling things online and being social media influencers.

Read More: The Business Case for Financial Wellness in Banking

9. YouTube is increasingly where Gen Z lives.

Enter the word “Banking” in the YouTube search function and most of what you’ll see are negative rants or news broadcasts, posts by fintech disruptors, or generic explanations of the banking system. That’s a missed opportunity for banks and credit unions because Experian’s research says that most recent high school graduates learn what they do about finances from their friends (28%), YouTube (27%) and social media in some other form (24%).

“Gen Z spends 23 hour per week on video content.”

Porter Novelli/Cone’s research reports that, in a generation whose preferences are still forming, it shouldn’t be a surprise that social media favorites change. YouTube (64% of Gen Z) edges out Instagram (63%), which in turn edges out Facebook (61%). Piper Jaffray research finds that teens spend 37% of their daily video consumption on YouTube — ahead of Netflix by two percentage points.

But there’s more to this than just those percentages. Gen Z consumers watch 68 videos daily, according to a much-quoted statistic. Another take on viewership: Research by Criteo finds that Gen Z spends 23 hour per week on video content.

A post by Visual Objects says that YouTube serves four functions for Gen Z: TV player; music player; influencer channel and learning channel.

Research by Think with Google and Ipsos found that 80% of Gen Z teens surveyed said that YouTube helped them become more knowledgeable about something. In addition, 68% said the platform taught them a skill or honed a skill they already had.

10. Facebook and YouTube where Gen Z goes to learn about and participate.

Porter Novelli/Cone’s study puts Facebook in first place at 66% and YouTube in second at 64%.

Multiple reports note how important issues and causes are to this generation and there is a temptation to get on board to build a connection with Gen Z, as well as Millennials. Best to sit this out if the financial brand isn’t wholly committed. Gen Z sniffs out inauthenticity, and will verify a brand’s record independently. “Three quarters will do research to see if a company is walking the talk when it takes a stand on an issue,” Porter Novelli/Cone reports.

11. Reaching Gen Z isn’t all about social media.

It can be tempting to think of Gen Z as a social media generation, but that’s not the only channel and not necessarily always the best channel.

For example, according to Raddon, comparatively few Gen Z consumers have ever sought out their financial service provider’s social media home page. So you can’t put all your chips on that.

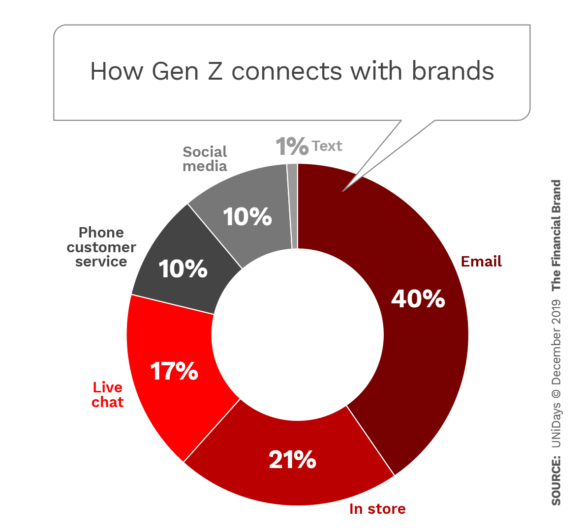

In fact, according to Gen Z research by UNiDays, when this generation wants to reach out to a specific brand, the two highest-ranking channels are decidedly old school: email, at 40%, and going to a store, at 21%. Social media? Only 10%.

This is interesting in light of the research noted early in this article about Gen Z’s interest in branches.

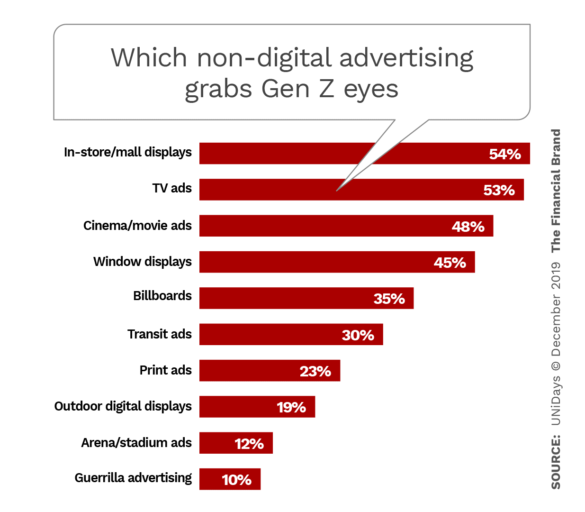

12. Gen Z isn’t just a digital generation.

While Gen Z is very comfortable with digital channels and spends almost a day a week on video, they are about more than electrons. Some traditional forms of advertising still pull well, according to UNiDay’s research.

13. Nearly half of Gen Z gets its news from social media sources.

Not only are many not relying on cable or TV news or newspapers or on their online components, what constitutes a news source to them is very different.

Morning Consult ranks Gen Z’s preferred digital-first news publications as:

- BuzzFeed News 27%

- Vice Media 14%

- Business Insider 12%

- Refinery29 9%

- Quartz 9%

- Vox Media 8%

- Thrillist 8%