The major turning point when digital banking transactions outstripped branch-based transactions has already passed. A much bigger milestone will be the point at which more consumers use digital-only providers as their primary financial institution than use traditional banks and credit unions. That day may be closer than many think. Impossible? New data show that only a couple of hurdles may stand in the way.

“30% of Americans have considered changing banks in the past year, and three quarters of them say they would consider a digital-only bank.”

A survey of U.S. consumers by Marqeta, a digital card issuer, found that just 14% of Americans use a digital bank exclusively. A fairly modest number, considering the marketing and operational prowess of Ally Bank, Discover Bank and other online-only institutions. However, the survey also found that nearly half (43%) of Americans use a digital banking service alongside their primary bank, and that, of those, just over half (53%) prefer the service of the digital bank.

On top of that, 30% of American consumers have considered changing banks in the past year, according to Marqeta, and three quarters of them say they would consider a digital-only bank if they were to make a change.

Security a Drag on Digital-Only Bank Growth

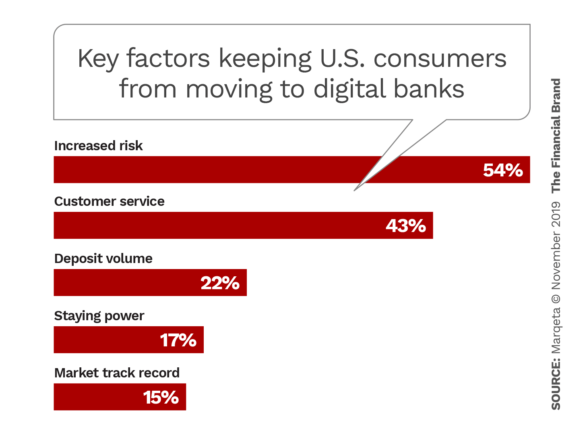

So why haven’t more consumers already shifted their primary accounts over to a digital bank? The single biggest factor uncovered by the Marqeta data is security. More than half of U.S. consumers (54%) feel a digital bank is a riskier place to put their money, and almost half (48%) say they would limit how much money they would deposit into a digital bank.

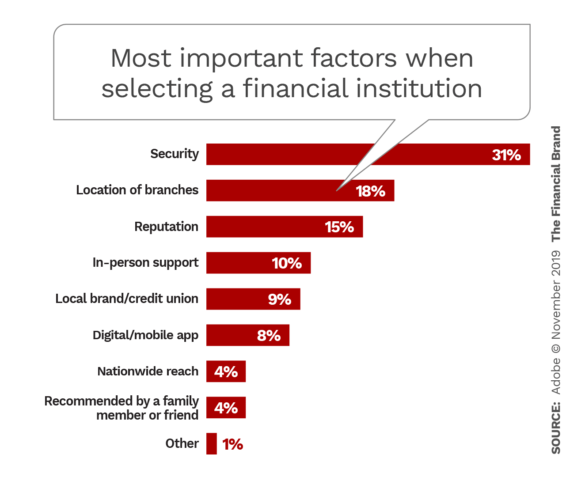

The risk factor surfaces in another consumer survey, conducted by Adobe. About a third of the approximately 1,000 respondents rank security as the most important factor when selecting a financial institution, far above reputation, digital capability and even branch location.

Security ranks even higher with consumers in connection with online-only banks, Adobe found. Exactly half agree with the statement: “With online-only banks, I worry about the safety of my finances.” For Gen Z respondents, that figures climbs to 62%.

“85% of consumers believe their traditional bank does enough to protect them from fraud and ensure their money is safe.”

Further, the Marqeta survey found that more than three quarters (78%) of all respondents (U.S. and U.K.) say they would actively consider security and reputation when deciding which account to deposit their paycheck into. And more than eight out of ten (85%) believe their traditional bank does enough to protect them from fraud and ensures their money is safe.

Clearly traditional banks and credit unions have the chops when it comes to security. And even Marqeta, a fintech company itself, notes that consumers’ perceptions about digital-bank risk could be slowing their adoption. The firm believes an economic turndown could make switching less likely. 61% of U.S. consumers say they would feel less comfortable changing to a digital bank if the state of the economy worsened. “Digital banks need to do more to win the trust and confidence of customers,” the company states.

Strong as they are, consumers’ reservations may not be an assurance that the threat to traditional institutions is diminished. For one thing, Marqeta found that only 17% of consumers say they are completely satisfied with their traditional banking provider. Lackluster digital banking capabilities is likely one of the reasons for this low number.

Read More:

- Major Storm Clouds On The Digital Banking Horizon

- Taking Mobile Banking to the Next Level with Innovation & Design

- It’s Time To Build Digital-First Banking Units

Most Consumers Label Digital Banking Ho-Hum

Nearly nine in ten consumers (89%) use their bank or credit union’s online banking option, Adobe found, and just over half of them (52%) conduct most of their banking online. In fact, the Adobe survey reports that nearly three in five consumers (59%) would not do business with a financial institution that didn’t offer digital or mobile banking services. This was particularly true of Millennial and Gen Z consumers, the firm points out.

The problem is, when Adobe probed further, it uncovered the fact that nearly two-thirds of consumers using traditional institutions’ digital banking consider it just average when compared with the digital experiences they have with other types of providers.

![]()

For most of the respondents, their digital banking activity mainly involves checking balances (67%), paying bills (36%) and making mobile check deposits (24%), according to Adobe. Fairly basic stuff compared with what is available from more advanced digital banking players. Some of the features offered by the top five financial institutions in Business Insider Intelligence’s Mobile Banking Provider Competitive Edge Study, for example, include these: financial wellness scores, card transaction dispute status, sending or requesting money, and chatting with a conversational assistant. This represents some of the best providers, of course, but is an indication of what consumers will expect from all institutions.

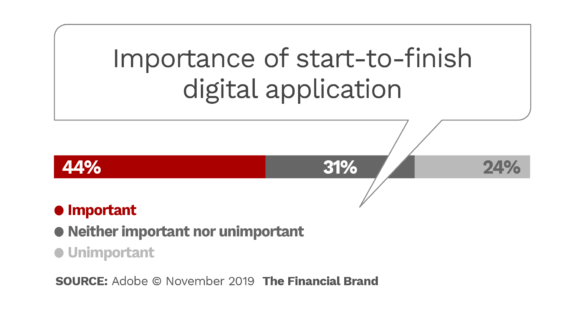

One measure of the degree of digital banking sophistication is the ability of a consumer to digitally complete an application for a loan or account from beginning to end without having to go to a branch or mail in documents. As shown below, just under half of consumers consider this feature to be important.

“Digital natives aren’t looking to just check their balances. They want to open an account without ever walking into a bank.”

— Craig Peasley, Adobe

“We’re finding that consumers are increasingly engaging with their banks online, especially for quick transactions like checking balances, but banks are just scratching the surface,” says Craig Peasley, Director of Marketing at Adobe. “The data shows that there’s still room to delight customers. Digital natives,” he continued, “aren’t looking to just check their balances and deposit checks. They’re looking for a more meaningful online experiences [including the ability to] open an account without ever walking into a bank.”

Read More:

- Chasing the Digital Dream: Can Banks Catch Up With Consumers?

- Build Your Digital Banking Strategy on a Mobile-First Foundation

Branches Still Matter, Sort of

While data from the two surveys were remarkably similar in many respects, their results diverged on the subject of in-person banking.

Adobe’s survey found that exactly three quarters of consumers believe financial institution branches still matter and that seven in ten had visited a branch at least once within the past month.

By contrast, less than a third (31%) of Marqeta’s sample of U.S. consumers say they bank primarily in person, and only 30% expect to visit a branch in the next three months.

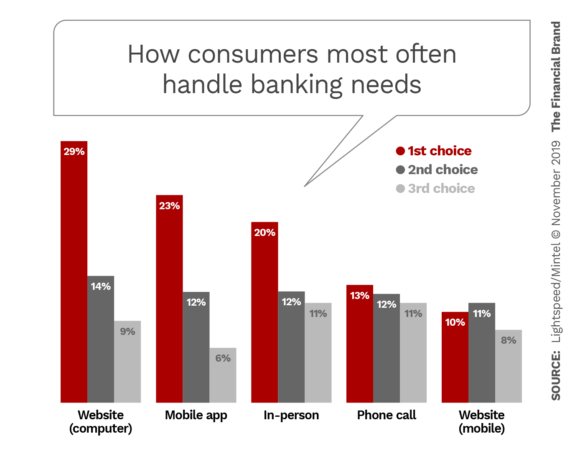

Further, when Marqeta asked consumers if they would be inconvenienced if their financial institution closed all of its physical locations, just one third said, “yes.” That may seem low, but in the chart below, from a Mintel report, an even smaller figure, 20%, selected “in-person” as their first choice for doing their banking.

The Mintel report, “Attitudes Toward Digital Trends and Fintech US, October 2019” also notes that “a third of all consumers say they would prefer not to have to go into a branch to conduct financial transactions.” However, more than three quarters (78%) agree that “there will always be a need for in-person transactions.”

“Banks need to make every touch point, both online and in person, as frictionless and helpful as possible for consumers,” says Adobe’s Peasley. “Banks need to complement the brick-and-mortar experience with innovative digital experiences in order to continue to engage and retain customers.”