The banking industry realizes that it must build a new distribution model — one that reflects consumers’ desire for cross-channel experiences like those they receive when shopping, paying and even selecting music or podcasts. Just as important, the banking industry also realizes that the current branch-focused distribution model is not financially viable going forward. Unfortunately, few organizations have met the challenge of building the banking distribution model of the future.

More and more consumers are selecting their retail banking partners based on new criteria, such as ease of use, engaging design and speed. The most advanced financial services providers understand that solutions must move towards a one-touch delivery. Today, consumers can begin the mortgage application process using their phone, providing only four pieces of information. An American Express card can be applied for with only a person’s name and Social Security number. Payments between two individuals can be done in a single click.

In the future, consumers will not have a problem separating their financial relationships between multiple specialty providers – benefiting from the partnership of humans and machines – getting the ultimate in customer experiences. These experiences will be personalized to the individual consumer and will be contextual to where, when and how the consumer wants to engage. Banking is being transformed by digital technology, the abundance of data and insights available, and the application of advanced analytics.

The distribution model of the future will require a reduction of traditional human-centric contact centers, with digital platforms offering seamless user experience. Expensive branch networks will need to be reduced and optimized. The payoff for traditional financial institutions will be a vastly improved consumer experience as well as improved profits and enhanced ability to compete with non-traditional providers.

According to a Boston Consulting Group study on the future of retail banking distribution, financial institutions can use five levers to generate as much as a 25% increase in profitability:

- Implementing the intelligent routing of customer requests between digital and assisted channels (profitability increase of 5% to 15%).

- Shifting from contact centers to customer care platforms (2% to 8% increase in profits).

- Embedding ‘distribution’ on partner platform services through application programming interfaces (APIs) (2% to 8% profit improvement).

- Reducing branch networks and optimizing remaining branches (profit enhancement of 2% to 8%).

- Harnessing the creativity and passion of front-line colleagues to meet customers’ needs, providing support for the four other levers.

While many organizations have made progress on one or more of these changes, the pace of distribution transformation must increase. Profits and enhanced experiences are in the balance.

Today’s Distribution Model Mired in the Past

Consumers are constantly being educated on what is possible with digital distribution of products and services. They realize that shopping for a new car or house can be enhanced by the combination of digital and human interactions and highly personalized options.

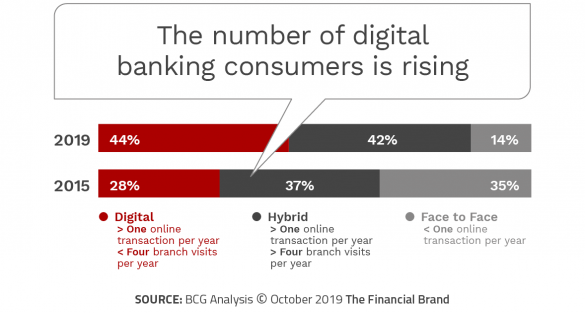

Compared with what they experience elsewhere, however, consumers are not very happy with the products, services and delivery options offered by retail banking. A BCG survey found that, in terms of customers’ willingness to advocate for banks’ services, retail banks rank ninth of ten industries. The winning industries have found ways to build consumer engagement digitally, allowing for minimal human intervention during the majority of the customer journey.

The industries where brand advocacy was the strongest were automotive, smartphones, cosmetics, and pay TV/streaming services. The only industry with lower advocacy was the utility business (gas and electricity). According to BCG, the new distribution model for retail banking will be more automated, channel agnostic, and capable of meeting individual needs across channels. The firm believes that while humans will still be involved, they will often be in a supplemental role for very high value engagements.

In effect, leading banks will be ‘ubiquitous,’ engaging with customers in close to real time, proactively offering solutions on a highly personalized basis. While this will involve the use of more consumer data, the value proposition will help negate the concern around privacy for most consumers.

Six Trends Impacting Retail Banking Distribution

According to BCG, there will be six key trends that will reshape the banking industry and which will also define winners and losers.

1. Multiple Customer Touch Points. Banks and credit unions will connect with consumers across an increasing array of channels and devices. These will include online and mobile apps, the Internet of Things, aggregator and open banking connections, internet searches, and social networks. The shift from physical to digital options will continue, with new integrations of delivery occurring, making banking more ‘invisible’.

2. Blurred Lines Between Humans and Machines. The use of more data and the application of advanced analytics and artificial intelligence (AI) will improve personalization, but blur the lines between human and machine. We are already seeing this with the application of chatbots for more simplified customer care. The use of advanced intelligence systems to make humans more effective (and efficient) will only increase with time.

3. Increased Delivery Options Across Channels. In the near future, advice and offerings will be shared and integrated across channels. This will allow the consumer to determine which channel they want to use for engagement, with no reduction in capabilities. According to BCG, banks and credit unions will increasingly communicate using text, voice (human or automated, online or in person), and video.

4. Service Model Differentiation Based on Customer Profile. As opposed to offering the same form of delivery to virtually all consumers, the future will see banks and credit unions differentiating between those consumers who receive ‘mass distribution’ and those who receive ‘enhanced delivery’ (most likely including greater use of humans).

5. Mass Personalization. According to Salesforce, nearly two-thirds of Millennials are willing to share personal data in return for more personalized service. This trend highlights the need for banking organizations to make every interaction personal and contextual, using data and analytics to offer relevant insights, products, and services. This level of personalization will increase engagement and loyalty and will improve the profits at financial institutions.

6. Wider Reach and Proactive Integration. Digital technology and open banking will allow consumers to find offerings and to engage across new touch points, including third-party offerings, ecosystems, and fintech firms. This will allow for even greater levels of product and service personalization, with proactive offerings being made before a consumer will even search for a solution.

Read More: Secret To Digital Banking Success is AI With “Human-Like” Feel

Distribution as Part of Future Digital Transformation

Despite historically low levels of churn reported by JD Powers, traditional financial institutions continue to be impacted by non-traditional offerings. From payments to lending and savings, fintech providers as well as big tech behemoths are siphoning business from consumers wanting simplified digital solutions. As a result, banks must focus on distribution models as part of their digital transformation process. Organizations must look to deliver ubiquitous, personalized solutions that make economic sense.

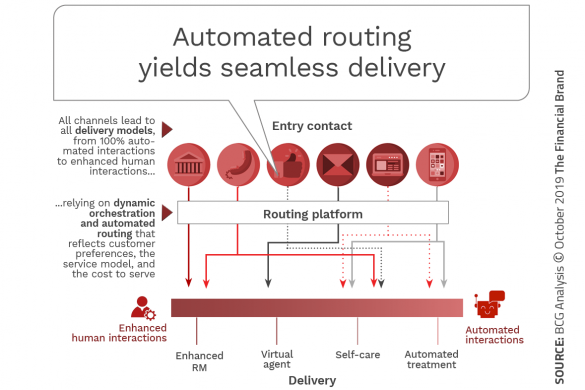

One of the strongest ways to redefine distribution of products, services and offers is through automated-routing capabilities. Through automated routing, banks can create seamless customer journeys and determine the best delivery option for each situation, product/service and consumer. The determination of correct set(s) of channels would be based on potential value and cost to serve. This new delivery model could include new channels such as virtual agents.

This form of routing becomes imperative with the integration of open banking APIs. This is because the analysis of customer insights and desires is required to determine which new set of products and services are best for each consumer. This becomes even more impactful with the integration of digital wallets and mobile dashboards, where the proactive offering of solutions can be delivered through alternative channels.

Retraining and Reskilling for the Future

One of the oft forgotten components of digital transformation, especially as we focus on new distribution models, is adjustments to the strategic mindset as it relates to human resources (and culture). One of the most important components of a redesigned distribution strategy is a revised talent strategy — with the requirement to retrain, reskill and redeploy resources for the digital age.

Much has been said about the potential loss of jobs in the banking industry, especially in the distribution and customer care (call center) areas. No place within banking will be more impacted … but few areas of banking provide a greater potential for differentiation.

With a focus on training for the integration of ‘humans powered by technology’, organizations can provide tremendous opportunities for individuals to leverage their customer-focused skills with the power of data, AI and advanced analytics. In other words, while some of the menial transactional components of jobs will be eliminated (as so many have been already), the ability to provide enhanced customer care will be valued.

The keys to the future delivery of financial services will be to place a higher focus on personalization and ease of engagement. This will require the combination of data, analytics and the delivery of solutions seamlessly across channels based on new value propositions.

According to BCG, “Banks need clever, connected, and responsive digital offerings; smart routing; new customer care platforms; inspired branch strategies; and a constructive approach to partnerships. The most effective approach to implementation will likely be based on agile principles.” As they summarize: “The prize for those that get it right is remaining competitive, serving customers better, and a significant boost to the bottom line.”