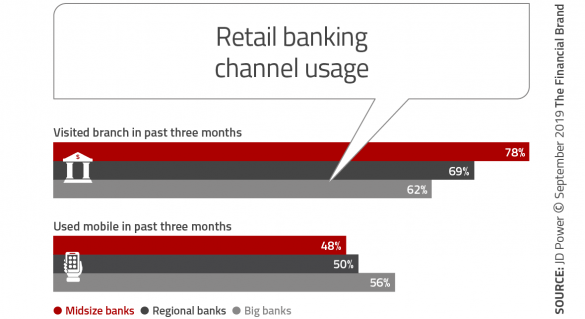

The banking industry continues to struggle with issues around reputation, trust and loyalty, failing to completely recover from pre-crisis issues that have resulted in new competitors and consumer backlash. One of the ways financial institutions have tried to change perceptions has been to build better mobile banking applications that respond to consumers’ desire to do banking on the go.

The building of improved mobile banking platforms is costly, however, with the largest banks previously having a distinct advantage when it comes to the ability to invest in the most progressive functionality. As increasing capabilities are built into mobile banking platforms, more consumers are moving transactions to digital channels, providing cost of delivery advantages to the biggest players.

Just as importantly, while midsize banks are still doing well satisfying older consumers, the largest banks are wining the battle for younger digital-centric customers. This positive satisfaction gap with younger consumers is driven by the benefits of convenience and self-service.

“Leading U.S. banks now have more than half of their customers interacting with them in a digitally centric manner,” said Bob Neuhaus, Vice President of Financial Services Intelligence at J.D. Power. “The trend is most pronounced among the largest national banks, such as Bank of America, which now counts 54% of its customers as digitally centric, meaning they do the bulk of their banking without setting foot in a branch.”

Is there a way for smaller banks and credit unions to compete in the mobile banking arms race?

Read More:

- Great Mobile Banking UX Demands More Than a Flood of Features

- How Bank of America and Chase Get Mobile Account Opening Right

- Banking Providers Struggle With Mobile Web Experience and Design

Satisfaction Becoming Correlated with Digital Delivery

According to J.D. Power, financial institutions must refine strategies to adapt to shifts in consumer behavior as more people disengage from the traditional branch. While satisfaction is lower for digital-only customers than those who access both digital and the branch delivery network, these metrics will most likely shift in favor of digital channels as more organizations improve the delivery of mobile services such as mobile account opening. In fact, J.D. Power found that consumers using digital-only banks far exceeded the satisfaction of any category of those using traditional banking institutions.

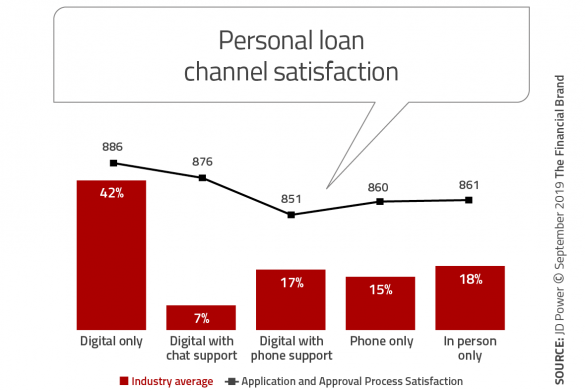

A glimpse into the future of digital banking satisfaction can already be seen with personal loan application processing. J.D. Power found that satisfaction for digital-only loan application processing far exceeded any alternative loan application. This trend has impacted the competitive balance for personal and mortgage loans, with alternative lenders receiving some of the highest satisfaction scores.

Early Mobile Banking Winners Defined by Number of Capabilities

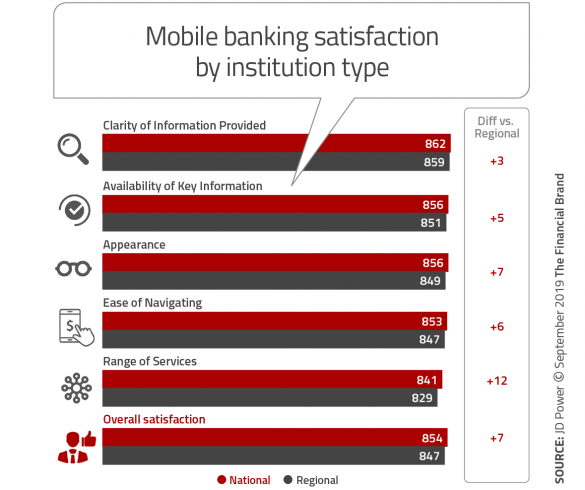

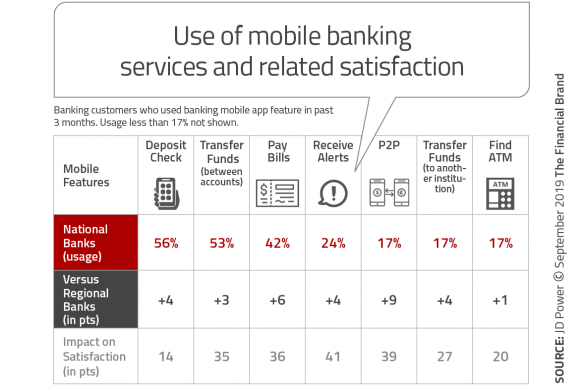

Until now, digital consumers have rewarded those organizations that have developed and deployed the greatest number of services on the mobile banking app. This has helped to position the largest banks with a significant competitive advantage vs. smaller organizations as mentioned earlier.

Adding to this advantage is that the largest banking organizations have the financial capabilities to be innovation leaders in the delivery of new services. This was evident with the introduction of mobile check deposit and deployment of mobile biometric identification. J.D. Power says that the percentage of large organizations that have deployed mobile check deposit has reached 90% (vs. 82% for regional banks), with 100% of national banks offering biometric ID (compared to 69% for regional banks).

The use of all advanced services by consumers at the largest banking organizations also exceeds the use at regional banks. This has driven higher satisfaction across all services at the largest financial institutions.

Despite these trends, smaller financial institutions have found a way to excel in mobile banking satisfaction by leveraging platform offerings to deliver narrower, high value mobile banking capabilities with well-designed mobile apps. For instance, Huntington Bank was rated the #1 mobile banking application by J.D. Power without offering chat, mobile statements, cardless ATM transactions, free credit scores or a virtual assistant.

In other words, trying to beat the largest financial institutions by offering all possible capabilities may not be the best strategy.

Read More:

- Build Your Digital Banking Strategy on a Mobile-First Foundation

- Data Can Move Mobile Banking from ‘Convenient’ to ‘Monetized’

- Poor Digital Sales Begins with Weak Content on Banking Websites

Winning the Next Phase of Mobile Banking Innovation with Advanced UI

The future mobile banking winners may not be defined by the number of mobile banking capabilities provided, but by the user experience designed into the mobile app and the level of personalized advice delivered through the mobile channel. Too many features may create an experience that’s difficult to navigate. As apps become increasingly powerful, banks and credit unions should devote more attention to user experience and navigability to help customers understand and use the app.

As was found years ago with online banking, more is not always better. Most consumers want an intuitive design that delivers what they want with clean look and feel and ease of use.

Some common sense keys to a better user experience include:

- Easy login

- Legible text

- Clean layout

- Personalized design

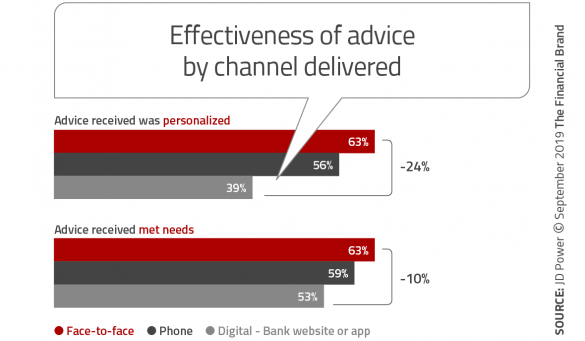

The most important capability for the future of mobile banking dominance will be the ability to deliver mobile advice and recommendations. While the effectiveness of advice delivered today still lags face-to-face delivery, the application of AI and time/place contextuality will elevate the power of mobile real-time advice.

Similar to how mobile GPS capabilities can provide time to destination insight based on future traffic conditions, the most progressive financial institutions will be able to delver proactive financial advice based on transactions that are occurring, and are most likely to occur in the future.

For instance, instead of asking the consumer to provide a “trigger” for low-balance alerts, a financial institution will notify a consumer about potential insufficient funds or overdraft on their mobile device based on deposits and withdrawals projected into the future based on past behavior. Proactive advice could also include a recommendation to transfer checking account funds to a savings or investment account if balances are higher than normal.

The future of mobile banking will be delivered in real time, driven by data and advanced analytics. This functionality is available to any sized organizations today.