Generation Z has acquired a reputation for being financially conservative, but that’s not the whole picture by any means. This generation began adding on consumer debt as soon as its members became old enough to take out loans and credit lines, and has continued to add more debt ever since, according to research from TransUnion.

“One potential factor in the rising level of Gen Z borrowing may be the greater access to credit in general.”

Gen Z consumers represent something of a moving target, much as have Millennials. Financial marketers who bog down too much in sweeping statements about a generation at any one point fail to take into account that people change as they grow older, even within the generational parameters that marketers scrutinize.

Much has been made of Gen Z’s care with a buck. Auto industry publications have discussed how dealers work to keep an inventory of used sedans on their lots because Gen Z first-time car buyers show little interest in buying the new SUVs that automakers keep cranking out. And that doesn’t even count those who feel they can get by without cars altogether thanks to ride-sharing services such as Uber and Lyft.

However, that doesn’t mean they aren’t borrowing to buy cars.

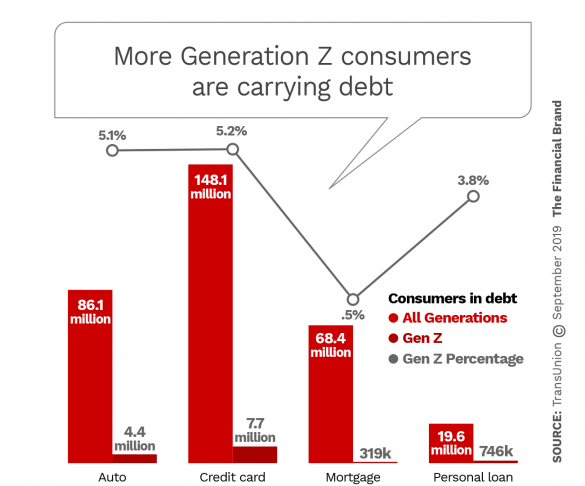

In fact, overall, TransUnion research finds that 14 million Gen Z consumers — 44% of this generation — were carrying some type of consumer credit balance as of the second quarter of 2019. That represents an increase of 27% over the second quarter of 2018. Gen Z, consisting of people born in 1995 or after, included 31.5 million consumers who were credit-eligible (over 18 years old) as of 2019’s second quarter. Another 13 million will become credit-eligible over the next three years.

One potential factor in the rising level of Gen Z borrowing may be the greater access to credit in general, suggests Paul Siegfried, Senior Vice President and Credit Card Business Leader at TransUnion. While it is early to say so definitively, he adds, Gen Z’s earlier adoption of consumer credit versus Millennials appears in part to be the result of Millennials’ coming of age in the midst of the Great Recession. As various experts have pointed out, circumstances thrust Millennials into the economic climate and poor job market. Gen Z, while influenced by what they saw happening to Gen X and Baby Boomer parents and in some cases Millennial siblings, observed those difficulties from the sidelines.

These developments come as a Merrill report, “Early Adulthood: The Pursuit of Financial Independence,” finds that a growing number of “early adult” consumers are not realizing their goal of financial independence due to debt burdens, the cost of living and additional factors. (This group, aged 18-34, includes both portions of the Gen Z and Millennial generations.)

Read More:

- 15 Things Banks & Credit Unions Must Know Before Targeting Gen Z

- Generation Z Means More Digital, Mobile & Social for Financial Marketers

Gen Z Grows Used to Idea of Life in Debt

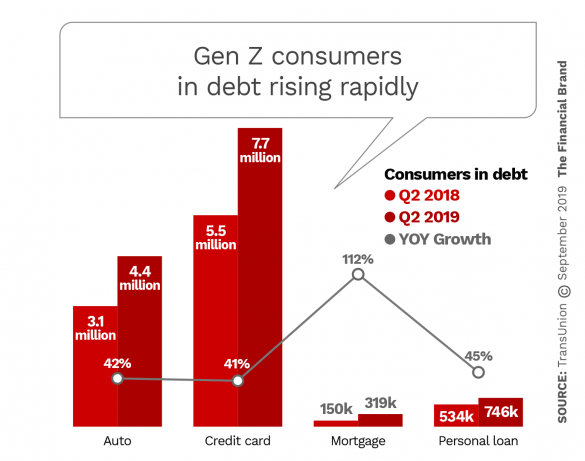

The TransUnion research finds that credit cards are the most common form of consumer credit used by Gen Z at present. Gen Z comprises about 5% of the U.S. population carrying card debt, but 55% of Gen Z cardholders have an outstanding balance.

By contrast, only a handful of Gen Zers have mortgages, which results in a very high growth rate of 112% given the small base.

Gen Z consumers represented 2% of total originations in the first quarter of 2019, according to TransUnion’s mortgage tracking. “Gen Z may soon account for a larger share of mortgage loan growth, however,” the company states, “as the median age of home buyers is 28 and the oldest individuals in this generation are currently 24.”

In auto credit, the second-largest area of Gen Z consumer debt, 1.3 million car loan borrowers from this generation came on during the second quarter of 2019. TransUnion notes that that tally exceeds the volume of additional borrowers from Millennials and Generation X combined.

In the area of personal loans, Generation Z represents the fastest-growing generation, the report states, at 45.5% growth in the second quarter over the pace of a year earlier.

Read More: Where’s the Marketing ROI on Financial Literacy Programs?

Debt Burden Delaying Gen Z’s Definition of Financial Success

The Merrill study capsulizes the situation this way: “Early adults today carry unprecedented levels of student and credit card debt. Starting salaries aren’t rising, but cost of living continues to. Many struggle to find meaningful work that pays well. Most rely on their parents for continued financial support to make ends meet and maintain their lifestyles.”

“While 19% of respondents define financial success as being rich, 60% say being debt-free would mean success to them.”

The study finds that while 19% of respondents define financial success as being rich, 60% say being debt-free would mean success to them.

An interesting wrinkle in the Merrill research concerns the all-pervasive role of personal technology in early adults’ lives. It appears to promote some smart consumer behavior — being able to look up comparative pricing while shopping for a car is an example. On the other hand, it also helps create pressures unseen by earlier generations.

Much has been made of Gen Z’s willingness to look beyond brand, but the Merrill study underscores the influence of social media on early adults.

For example, almost half of the Merrill sample feels addicted to social media. And nearly 70% admit to FOMO — fear of missing out on the lifestyle they perceive their social-media-linked friends appear to be leading. 60% of the sample say they feel pressure to buy things that they can’t afford. And one in four say they have made early withdrawals from retirement savings to pay down credit card bills.

“FOMO can shape people’s spending habits,” the report says, “and it can engender indecision. 42% say they hesitate to commit to social plans because something better might come along. The same indecision often extends to jobs, relationships and financial decisions.”

These pressures, and outstanding student debt, which takes almost a tenth of respondents’ pre-tax income, appear to be creating a situation where many early adults would like to be financially independent of their parents but they aren’t there yet. This was the top factor given — by 75% of respondents — when asked “what it takes to become an adult.”

58% of the early adults say they could not afford their current lifestyles without parental support. The support, consisting of parents paying in full or in part, ranks as follows:

- Cell phone/phone plan 46%

- Food/groceries 44%

- School or related costs 37%

- Car expenses 36%

- Vacations 36%

- Rent/mortgage payment 34%

- Student loans 30%

Where do financial institutions fit in this mix, having both the role of lenders but also the aspiration of being financial advisors? The Merrill report contains a suggestion:

“Early adults are much more likely to describe this life stage as a roller coaster (30%), a juggling act (24%) or climbing a mountain (24%) than a day at the beach (8%). Two-thirds say they feel fatigued by their new responsibilities and 72% say they wish they had more guidance and clarity about how to effectively become an adult.”